Potrebbero piacerti anche

- Place of Provision of Services Rules, 2012Documento7 paginePlace of Provision of Services Rules, 2012Suppy PNessuna valutazione finora

- Service Tax - Pop RulesDocumento5 pagineService Tax - Pop RulesSuman ParialNessuna valutazione finora

- Place of Provision of Services RulesDocumento4 paginePlace of Provision of Services RulesParth UpadhyayNessuna valutazione finora

- Section 13 of The Integrated Goods and Services ActDocumento3 pagineSection 13 of The Integrated Goods and Services ActNikita BaliNessuna valutazione finora

- Article Draft IGST Part IDocumento7 pagineArticle Draft IGST Part IAshok SharmaNessuna valutazione finora

- Brief Facts of The Case: 2.1Documento11 pagineBrief Facts of The Case: 2.1Gaurav SinghNessuna valutazione finora

- (A) Date of Introduction: (B) Definition and Scope of ServiceDocumento6 pagine(A) Date of Introduction: (B) Definition and Scope of ServicePradeep JainNessuna valutazione finora

- Place of SupplyDocumento6 paginePlace of SupplyMadhuram SharmaNessuna valutazione finora

- Chapter-I Preliminary: NotificationDocumento46 pagineChapter-I Preliminary: NotificationBasitGillaniNessuna valutazione finora

- 30688revised-Sm Finalnew Idtl Service cp2Documento20 pagine30688revised-Sm Finalnew Idtl Service cp2Saurav KakkarNessuna valutazione finora

- Service Tax Rules, 1994Documento75 pagineService Tax Rules, 1994Gens GeorgeNessuna valutazione finora

- Government of India notifies taxable services under Service TaxDocumento2 pagineGovernment of India notifies taxable services under Service TaxAMIT GUPTANessuna valutazione finora

- Chapter 10 Place of Supply Under GSTDocumento15 pagineChapter 10 Place of Supply Under GSTDR. PREETI JINDALNessuna valutazione finora

- Notification No 15/2012Documento2 pagineNotification No 15/2012Ankit GuptaNessuna valutazione finora

- Service Tax RulesDocumento4 pagineService Tax RulesSURYA SNessuna valutazione finora

- Site Info ClearanceDocumento9 pagineSite Info ClearanceAnuppur Amlai RangeNessuna valutazione finora

- Stock Exchange Service (A) Date of IntroductionDocumento7 pagineStock Exchange Service (A) Date of Introductionarshad89057Nessuna valutazione finora

- GST ImportDocumento28 pagineGST ImportTripathi OjNessuna valutazione finora

- TPT RoadDocumento13 pagineTPT RoadLakhan PatidarNessuna valutazione finora

- Export of Services and Intermediary ServicesDocumento43 pagineExport of Services and Intermediary ServicesPhani BhaskarNessuna valutazione finora

- Import and Export Under GSTDocumento50 pagineImport and Export Under GSTSONICK THUKKANINessuna valutazione finora

- Works Contract ServicesDocumento13 pagineWorks Contract ServicesSreedhar EtrouthuNessuna valutazione finora

- WWW - Livelaw.In: Explanation.-For The Purposes of This Clause, "Governmental Authority" Means AnDocumento16 pagineWWW - Livelaw.In: Explanation.-For The Purposes of This Clause, "Governmental Authority" Means Anc3849666Nessuna valutazione finora

- Integrated Goods and Services Tax ActDocumento14 pagineIntegrated Goods and Services Tax ActsanjitaNessuna valutazione finora

- Kerala Tax on Luxuries Acts GuideDocumento32 pagineKerala Tax on Luxuries Acts GuideShafna AshrafNessuna valutazione finora

- Carriage by Road Act, 2007Documento11 pagineCarriage by Road Act, 2007Shayan GhoshNessuna valutazione finora

- Supply Under GST: Concept of Supply (Section 7 of CGST Act)Documento13 pagineSupply Under GST: Concept of Supply (Section 7 of CGST Act)Qamran moin khanNessuna valutazione finora

- Notification No. 30/2012-Service TaxDocumento4 pagineNotification No. 30/2012-Service TaxReview UdaipurNessuna valutazione finora

- ST Determtn Value Rules PDFDocumento4 pagineST Determtn Value Rules PDFKumarvNessuna valutazione finora

- Sindh Sales Tax On Services Rules 2011 (Amendede Upto 30 Nov 2012) PDFDocumento64 pagineSindh Sales Tax On Services Rules 2011 (Amendede Upto 30 Nov 2012) PDFrohail51Nessuna valutazione finora

- ST Determtn Value Rules 1Documento4 pagineST Determtn Value Rules 1Poonam GuptaNessuna valutazione finora

- GST Module 2 - Collection and LevyDocumento19 pagineGST Module 2 - Collection and LevyPooja D AcharyaNessuna valutazione finora

- Luxurytax As On 2008Documento31 pagineLuxurytax As On 2008syriluitNessuna valutazione finora

- Insurance Auxiliary Services GuideDocumento9 pagineInsurance Auxiliary Services GuidePunit GuptaNessuna valutazione finora

- Chapter Eleven Cross-Border Trade in ServicesDocumento17 pagineChapter Eleven Cross-Border Trade in ServicesEstudiantes por DerechoNessuna valutazione finora

- Service Tax Credit RulesDocumento4 pagineService Tax Credit Rulesgauravbarthwal123Nessuna valutazione finora

- Place of SupplyDocumento7 paginePlace of SupplyAkash SharmaNessuna valutazione finora

- Integrated Goods and Services Tax ActDocumento17 pagineIntegrated Goods and Services Tax Actdkgupta28Nessuna valutazione finora

- Taxation of Financial Services Sybbi FinalDocumento24 pagineTaxation of Financial Services Sybbi Finalsheenu152005Nessuna valutazione finora

- Abatement in Service Tax 2010Documento3 pagineAbatement in Service Tax 2010Pankaj MaggoNessuna valutazione finora

- Meaning and Scope of Supply Under GSTDocumento5 pagineMeaning and Scope of Supply Under GSTGirish kNessuna valutazione finora

- Kerala Tax on Luxuries ActDocumento33 pagineKerala Tax on Luxuries ActdinuindiaNessuna valutazione finora

- Bimal Jain BGM Service Tax 051014Documento67 pagineBimal Jain BGM Service Tax 051014Aayushi AroraNessuna valutazione finora

- Service Tax on Air TravelDocumento15 pagineService Tax on Air TravelvijaykoratNessuna valutazione finora

- Carriage by Road Act, 2007Documento9 pagineCarriage by Road Act, 2007KLE CBALCNessuna valutazione finora

- Cable TVDocumento15 pagineCable TVYeluripati VR SubrahmanyamNessuna valutazione finora

- TH TH: Explanation.-For The Purposes of This ClauseDocumento4 pagineTH TH: Explanation.-For The Purposes of This ClauseAks SomvanshiNessuna valutazione finora

- The Cable Television Networks (Regulation) Act, 1995Documento9 pagineThe Cable Television Networks (Regulation) Act, 1995AnkitTiwariNessuna valutazione finora

- IGST Act Updated 01.10.2021Documento28 pagineIGST Act Updated 01.10.2021Amit K. SinghNessuna valutazione finora

- Variant 3 REVISED Jan13 LDocumento96 pagineVariant 3 REVISED Jan13 LGopakumar PNessuna valutazione finora

- The Punjab Place of Provision of Services Rules, 2023Documento6 pagineThe Punjab Place of Provision of Services Rules, 2023Rameel ShafqatNessuna valutazione finora

- Rules 1Documento6 pagineRules 1afaqNessuna valutazione finora

- TRAVEL TAX TITLEDocumento9 pagineTRAVEL TAX TITLEAPI SupportNessuna valutazione finora

- Payment of Service TaxDocumento12 paginePayment of Service TaxPrasanth KumarNessuna valutazione finora

- Secret Trade in Services Agreement (TISA) 2014Documento7 pagineSecret Trade in Services Agreement (TISA) 2014clonazzyoNessuna valutazione finora

- Payment of Wages Act SummaryDocumento10 paginePayment of Wages Act SummaryhappyNessuna valutazione finora

- Introduction to Negotiable Instruments: As per Indian LawsDa EverandIntroduction to Negotiable Instruments: As per Indian LawsValutazione: 5 su 5 stelle5/5 (1)

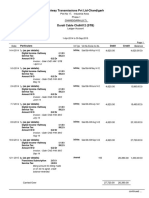

- Friends Cable NW - CHDH016 (STB)Documento2 pagineFriends Cable NW - CHDH016 (STB)Kanishk YadavNessuna valutazione finora

- New Gill Cable - 22275 - CommDocumento3 pagineNew Gill Cable - 22275 - CommKanishk YadavNessuna valutazione finora

- Friends Cable Network-Jassi CHDH015Documento11 pagineFriends Cable Network-Jassi CHDH015Kanishk YadavNessuna valutazione finora

- Friends CBL Jaspal Ph-1-22281Documento8 pagineFriends CBL Jaspal Ph-1-22281Kanishk YadavNessuna valutazione finora

- Friends Cable Jaswinder-24539Documento8 pagineFriends Cable Jaswinder-24539Kanishk YadavNessuna valutazione finora

- Freinds Cable Jaspal 22281 STBDocumento1 paginaFreinds Cable Jaspal 22281 STBKanishk YadavNessuna valutazione finora

- Friends Cable Network CHDH016 CommDocumento4 pagineFriends Cable Network CHDH016 CommKanishk YadavNessuna valutazione finora

- Friends Cable Network-Jassi CHDH015Documento11 pagineFriends Cable Network-Jassi CHDH015Kanishk YadavNessuna valutazione finora

- Friends Cable NW - CHDH016 (STB)Documento2 pagineFriends Cable NW - CHDH016 (STB)Kanishk YadavNessuna valutazione finora

- Friends Cable Nw-CHDH015 (STB)Documento1 paginaFriends Cable Nw-CHDH015 (STB)Kanishk YadavNessuna valutazione finora

- Friends Cable Network 24539 COMMDocumento3 pagineFriends Cable Network 24539 COMMKanishk YadavNessuna valutazione finora

- B&W EntDocumento8 pagineB&W EntKanishk YadavNessuna valutazione finora

- Durali Cable Durali SA C 0019 09Documento4 pagineDurali Cable Durali SA C 0019 09Kanishk YadavNessuna valutazione finora

- Durali Cable SA C 0029 10Documento2 pagineDurali Cable SA C 0029 10Kanishk YadavNessuna valutazione finora

- Chandigarh cable company ledger shows STB sales & rentalsDocumento2 pagineChandigarh cable company ledger shows STB sales & rentalsKanishk YadavNessuna valutazione finora

- Friends Cable Network-Jaswinder CHDH016Documento11 pagineFriends Cable Network-Jaswinder CHDH016Kanishk YadavNessuna valutazione finora

- 20150430175941ISTC Information Brochure - 2015 PDFDocumento28 pagine20150430175941ISTC Information Brochure - 2015 PDFKanishk YadavNessuna valutazione finora

- Durali Cable Chdh012Documento3 pagineDurali Cable Chdh012Kanishk YadavNessuna valutazione finora

- 20150430175941ISTC Information Brochure - 2015 PDFDocumento28 pagine20150430175941ISTC Information Brochure - 2015 PDFKanishk YadavNessuna valutazione finora

- DSCN-Arora Cable (Half Year)Documento15 pagineDSCN-Arora Cable (Half Year)Kanishk YadavNessuna valutazione finora

- New Microsoft Office Word DocumentDocumento8 pagineNew Microsoft Office Word DocumentKanishk YadavNessuna valutazione finora

- Landran Cable NetworkDocumento6 pagineLandran Cable NetworkKanishk YadavNessuna valutazione finora

- B&W EntDocumento8 pagineB&W EntKanishk YadavNessuna valutazione finora

- 12th ExemplerDocumento359 pagine12th Exemplergiophilip100% (1)

- B&W SCN Rs. 67 LacDocumento6 pagineB&W SCN Rs. 67 LacKanishk YadavNessuna valutazione finora

- DSCN Lco DraftDocumento6 pagineDSCN Lco DraftKanishk YadavNessuna valutazione finora

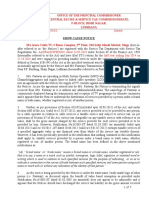

- Cable Operator Service Tax NoticeDocumento6 pagineCable Operator Service Tax NoticeKanishk YadavNessuna valutazione finora

- DSCN Lco DraftDocumento6 pagineDSCN Lco DraftKanishk YadavNessuna valutazione finora

- Request transfer to Chandigarh audit circle due to family issuesDocumento3 pagineRequest transfer to Chandigarh audit circle due to family issuesKanishk YadavNessuna valutazione finora

- IAS 38:-Intangible Assets: 11.1 Acca Syllabus Guide Outcome 1Documento242 pagineIAS 38:-Intangible Assets: 11.1 Acca Syllabus Guide Outcome 1Şâh ŠůmiťNessuna valutazione finora

- Textile Policy 2009-14Documento40 pagineTextile Policy 2009-14Arif Haq67% (3)

- Tan Vs Phil Banking (G.R. No. 137739)Documento9 pagineTan Vs Phil Banking (G.R. No. 137739)Rose MadrigalNessuna valutazione finora

- Accounting and Finance Management SystemDocumento3 pagineAccounting and Finance Management SystemAkash KumarNessuna valutazione finora

- VP Finance Risk Management in San Francisco CA Resume Michelle JamesDocumento2 pagineVP Finance Risk Management in San Francisco CA Resume Michelle JamesMichelleJamesNessuna valutazione finora

- Financial Accounting II: 2 Year ExaminationDocumento32 pagineFinancial Accounting II: 2 Year ExaminationGeneGrace Zolina TasicNessuna valutazione finora

- CH 12Documento63 pagineCH 12Grace VersoniNessuna valutazione finora

- Report On Financial Analysis of ICI Pakistan Limited 2008Documento9 pagineReport On Financial Analysis of ICI Pakistan Limited 2008helperforeuNessuna valutazione finora

- United Breweries Holdings LimitedDocumento7 pagineUnited Breweries Holdings Limitedsalini sasiNessuna valutazione finora

- Official Form 206sum: Summary of Assets and Liabilities For Non-IndividualsDocumento1 paginaOfficial Form 206sum: Summary of Assets and Liabilities For Non-IndividualsReading_EagleNessuna valutazione finora

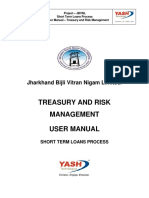

- SAP TRM Short Term Loans ProcessDocumento18 pagineSAP TRM Short Term Loans ProcessSantiago VelezNessuna valutazione finora

- Business - Valuation - Modeling - Assessment FileDocumento6 pagineBusiness - Valuation - Modeling - Assessment FileGowtham VananNessuna valutazione finora

- Lecture Notes in Taxation - TariffDocumento3 pagineLecture Notes in Taxation - TariffbubblingbrookNessuna valutazione finora

- Financial Strategy ALL MergedDocumento379 pagineFinancial Strategy ALL MergedSushil PrajapatNessuna valutazione finora

- Grand Strategy For Burma - VIIIDocumento186 pagineGrand Strategy For Burma - VIIIthangzadal100% (1)

- Direct Method or Cost of Goods Sold MethodDocumento2 pagineDirect Method or Cost of Goods Sold MethodNa Dem DolotallasNessuna valutazione finora

- Chapter-1: Working CapitalDocumento47 pagineChapter-1: Working Capitalchhita mani sorenNessuna valutazione finora

- Final Rule NoticeDocumento79 pagineFinal Rule NoticedechtersNessuna valutazione finora

- CHapter 4 COnsolidated After Date of AcquisitionDocumento53 pagineCHapter 4 COnsolidated After Date of AcquisitionAchmad RizalNessuna valutazione finora

- LVHM & Warnaco: Strategy & Financial Statement AnalysisDocumento5 pagineLVHM & Warnaco: Strategy & Financial Statement AnalysisVanshika SinghNessuna valutazione finora

- Ae 18 Financial MarketsDocumento6 pagineAe 18 Financial Marketsnglc srzNessuna valutazione finora

- TTM 10 Time Value of Money - LanjutanDocumento58 pagineTTM 10 Time Value of Money - LanjutanDede KurniatiNessuna valutazione finora

- ICPAC Presentation - Common Deficiencies On ISQC 1 and ISA Compliance Nov 13Documento18 pagineICPAC Presentation - Common Deficiencies On ISQC 1 and ISA Compliance Nov 13DruzmaNessuna valutazione finora

- Articles of Incorporation OF Blue Cart Holding, Inc.: FIRST: That The Name of The Said Corporation Shall BeDocumento7 pagineArticles of Incorporation OF Blue Cart Holding, Inc.: FIRST: That The Name of The Said Corporation Shall BeEurich EstradaNessuna valutazione finora

- Module 07 - Introduction To Regular Income TaxDocumento25 pagineModule 07 - Introduction To Regular Income TaxJANELLE NUEZNessuna valutazione finora

- Modern Challenges Faced by Banking Sector of Pakistan Evidence From: The First Micro Finance Bank, Js Bank and Bankislami PakistanDocumento3 pagineModern Challenges Faced by Banking Sector of Pakistan Evidence From: The First Micro Finance Bank, Js Bank and Bankislami PakistanNaveed AhmadNessuna valutazione finora

- Automatic Appropriation for Debt Service UpheldDocumento2 pagineAutomatic Appropriation for Debt Service UpheldBeatrice AbanNessuna valutazione finora

- Ch16 09Documento5 pagineCh16 09Umer Shaikh50% (2)

- Johnson & Johnson JNJ Stock-Sample Analysis Report Intrinsic ValueDocumento12 pagineJohnson & Johnson JNJ Stock-Sample Analysis Report Intrinsic ValueOld School Value100% (2)

- APY Details of The SchemeDocumento5 pagineAPY Details of The SchemeDipesh NagpalNessuna valutazione finora