Potrebbero piacerti anche

- Freedom to Operate EssentialsDocumento24 pagineFreedom to Operate Essentialssandeep patialNessuna valutazione finora

- Bio Similar SDocumento5 pagineBio Similar Ssandeep patialNessuna valutazione finora

- Joint Venture FinalDocumento29 pagineJoint Venture Finalsandeep patialNessuna valutazione finora

- Pharma CMOs Pursue Success Strategies Focusing on Operational ExcellenceDocumento22 paginePharma CMOs Pursue Success Strategies Focusing on Operational Excellencesandeep patialNessuna valutazione finora

- ElnDocumento9 pagineElnsandeep patialNessuna valutazione finora

- Case AnalysispaperDocumento15 pagineCase Analysispapersandeep patialNessuna valutazione finora

- Ethics in R & D ManagementDocumento32 pagineEthics in R & D Managementsandeep patialNessuna valutazione finora

- Selecting Foreign Investors Using the EPRG FrameworkDocumento8 pagineSelecting Foreign Investors Using the EPRG Frameworksandeep patialNessuna valutazione finora

- Department of Scientific and Industrial Research (India)Documento2 pagineDepartment of Scientific and Industrial Research (India)sandeep patialNessuna valutazione finora

- TIPS For Writing Case Studies: Provided by The Abstracts CommitteeDocumento9 pagineTIPS For Writing Case Studies: Provided by The Abstracts Committeesandeep patialNessuna valutazione finora

- Forms Fees and Patent SearchingDocumento138 pagineForms Fees and Patent Searchingsandeep patialNessuna valutazione finora

- End-to-end IT modernization critical for digital business successDocumento79 pagineEnd-to-end IT modernization critical for digital business successsandeep patialNessuna valutazione finora

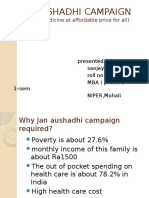

- Jan Aushadhi Campiagn by Sanjay NakumDocumento30 pagineJan Aushadhi Campiagn by Sanjay Nakumsandeep patialNessuna valutazione finora

- Project Portfolio MatrixDocumento1 paginaProject Portfolio Matrixsandeep patialNessuna valutazione finora

- 006 Id 101Documento10 pagine006 Id 101lavate amol bhimraoNessuna valutazione finora

- Study Note: This Module Should Take AroundDocumento27 pagineStudy Note: This Module Should Take Aroundlavate amol bhimraoNessuna valutazione finora

- Economy of India: Fdi in Indian Pharma SectorDocumento38 pagineEconomy of India: Fdi in Indian Pharma Sectorsandeep patialNessuna valutazione finora

- Here Are The 19 Plans Modi Has For Start-Ups: 1. Self CertificationDocumento6 pagineHere Are The 19 Plans Modi Has For Start-Ups: 1. Self Certificationsandeep patialNessuna valutazione finora

- The Indian Pharmaceutical Industry Is One of The Most Attractive Investment Destinations in The WorldDocumento7 pagineThe Indian Pharmaceutical Industry Is One of The Most Attractive Investment Destinations in The Worldsandeep patialNessuna valutazione finora

- Digital India - WordDocumento2 pagineDigital India - Wordsandeep patialNessuna valutazione finora

- Ethical Issues in Health Care Sector in IndiaDocumento34 pagineEthical Issues in Health Care Sector in Indiasandeep patialNessuna valutazione finora

- M A in Pharama SectorDocumento35 pagineM A in Pharama Sectorsandeep patialNessuna valutazione finora

- Orphan Drug Development TrendsDocumento31 pagineOrphan Drug Development Trendssandeep patialNessuna valutazione finora

- OutsourcingDocumento6 pagineOutsourcingsandeep patialNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)