Potrebbero piacerti anche

- Research Methodology of Portfolio ManagementDocumento6 pagineResearch Methodology of Portfolio ManagementZalak Shah100% (1)

- Zeus Asset Management Case Week 5Documento8 pagineZeus Asset Management Case Week 5Johanlee1992Nessuna valutazione finora

- Reading 24 - Equity Valuation - Applications and ProcessesDocumento5 pagineReading 24 - Equity Valuation - Applications and ProcessesJuan MatiasNessuna valutazione finora

- RELATIVE VALUATION Theory PDFDocumento5 pagineRELATIVE VALUATION Theory PDFPrateek SidharNessuna valutazione finora

- CDMDocumento2 pagineCDMi am tadaeiNessuna valutazione finora

- 25 SAP CRM Interview Questions and AnswersDocumento5 pagine25 SAP CRM Interview Questions and AnswersHunny BhatiaNessuna valutazione finora

- Financial Reporting and AnalysisDocumento34 pagineFinancial Reporting and AnalysisNatasha AzzariennaNessuna valutazione finora

- Cfa Prepare Part 4Documento12 pagineCfa Prepare Part 4Роберт МкртчянNessuna valutazione finora

- Chapter 6Documento24 pagineChapter 6sdfklmjsdlklskfjd100% (2)

- Investment Valuatio1Documento9 pagineInvestment Valuatio1Nguyen Thi HangNessuna valutazione finora

- Task 1Documento5 pagineTask 1my youtube advisorNessuna valutazione finora

- FM QP KeyDocumento19 pagineFM QP KeyporseenaNessuna valutazione finora

- CH 16Documento9 pagineCH 16NMBGolfer100% (1)

- Company Analysis & Stock Val.Documento7 pagineCompany Analysis & Stock Val.Ezyquel QuintoNessuna valutazione finora

- Securities Analysis & Portfolio Management IntroDocumento50 pagineSecurities Analysis & Portfolio Management IntrogirishNessuna valutazione finora

- Synopsis On A Comparative Study of Equity Linked Savings Schemes Floated by Domestic Mutual Fund PlayersDocumento8 pagineSynopsis On A Comparative Study of Equity Linked Savings Schemes Floated by Domestic Mutual Fund PlayersPraveen Sehgal100% (1)

- Stock and Stock Valuation Garcia Cheska Kate HDocumento4 pagineStock and Stock Valuation Garcia Cheska Kate HJosua PranataNessuna valutazione finora

- Unit - Iv Valuation of Shares and Goodwill What Is Share Valuation?Documento56 pagineUnit - Iv Valuation of Shares and Goodwill What Is Share Valuation?Rizwan AkhtarNessuna valutazione finora

- Corporate ValuationDocumento23 pagineCorporate ValuationRakesh GuptaNessuna valutazione finora

- Uk Cmsa - Nur Eka Ayu Dana - 20180420159 - Ipacc 2018Documento3 pagineUk Cmsa - Nur Eka Ayu Dana - 20180420159 - Ipacc 2018nur eka ayu danaNessuna valutazione finora

- Acca F9 Business ValuationsDocumento6 pagineAcca F9 Business ValuationsHaseeb SethyNessuna valutazione finora

- 8524 UniqueDocumento20 pagine8524 UniqueMs AimaNessuna valutazione finora

- Unconfirmed 205358.crdownloadDocumento13 pagineUnconfirmed 205358.crdownloadKavita PawarNessuna valutazione finora

- DocumentDocumento24 pagineDocumentKavita PawarNessuna valutazione finora

- Equity AnalysisDocumento6 pagineEquity AnalysisVarsha Sukhramani100% (1)

- Stock Market Efficiency & Stock ValuationDocumento23 pagineStock Market Efficiency & Stock ValuationKaila SalemNessuna valutazione finora

- Moduel 4Documento4 pagineModuel 4sarojkumardasbsetNessuna valutazione finora

- Fsa 12NDocumento4 pagineFsa 12Npriyanshu.goel1710Nessuna valutazione finora

- FIN 404 Final AssessmentDocumento16 pagineFIN 404 Final AssessmentHOSSAIN MOHAMMAD YEASINNessuna valutazione finora

- Lesson 1 - OVERVIEW OF VALUATION CONCEPTS AND METHODSDocumento14 pagineLesson 1 - OVERVIEW OF VALUATION CONCEPTS AND METHODSGevilyn M. GomezNessuna valutazione finora

- CAPMDocumento8 pagineCAPMshadehdavNessuna valutazione finora

- SHARPE SINGLE INDEX MODEL - HarryDocumento12 pagineSHARPE SINGLE INDEX MODEL - HarryEguanuku Harry EfeNessuna valutazione finora

- Project Report: "A Study On The Stock Performance of Higher Dividend Yielding Companies "Documento20 pagineProject Report: "A Study On The Stock Performance of Higher Dividend Yielding Companies "Arun OusephNessuna valutazione finora

- Risk and Return: Week 3 - Financial MarketDocumento25 pagineRisk and Return: Week 3 - Financial MarketToni MarquezNessuna valutazione finora

- Business 2 2023Documento10 pagineBusiness 2 2023group0840Nessuna valutazione finora

- Merger & Acquisition: Defences Against Unwelcome TakeoversDocumento22 pagineMerger & Acquisition: Defences Against Unwelcome TakeoversViraj GawandeNessuna valutazione finora

- Equity Securities MarketDocumento40 pagineEquity Securities MarketBea Bianca MadlaNessuna valutazione finora

- INV (8 Questions)Documento2 pagineINV (8 Questions)leizelNessuna valutazione finora

- Project On Impact of Dividends Policy 1Documento43 pagineProject On Impact of Dividends Policy 1Soma BanikNessuna valutazione finora

- Chapter 7Documento11 pagineChapter 7Seid KassawNessuna valutazione finora

- Task 3 - Investment AppraisalDocumento12 pagineTask 3 - Investment AppraisalYashmi BhanderiNessuna valutazione finora

- Part 1 & 2Documento12 paginePart 1 & 2Monoarul Islam JawadNessuna valutazione finora

- Is Your Stock Worth Its Market PriceDocumento14 pagineIs Your Stock Worth Its Market PriceHuicai MaiNessuna valutazione finora

- Securities Analysis & Portfolio ManagementDocumento52 pagineSecurities Analysis & Portfolio ManagementruchisinghnovNessuna valutazione finora

- F9 Note (Business Valuation 1)Documento12 pagineF9 Note (Business Valuation 1)CHIAMAKA EGBUKOLENessuna valutazione finora

- Differentiate Profit Maximization From Wealth MaximizationDocumento8 pagineDifferentiate Profit Maximization From Wealth MaximizationRobi MatiNessuna valutazione finora

- Factors Affecting Valuation of SharesDocumento6 pagineFactors Affecting Valuation of SharesSneha ChavanNessuna valutazione finora

- Portfolio Management NotesDocumento25 paginePortfolio Management NotesRigved DarekarNessuna valutazione finora

- Equity Shares 3Documento4 pagineEquity Shares 3Sci UpscNessuna valutazione finora

- Equity HY NotesDocumento30 pagineEquity HY NotesshalinNessuna valutazione finora

- Security Analysis and Portfolio Management (SAPM) E-Lecture Notes (For MBA) IMS, MGKVP, Session 2020Documento17 pagineSecurity Analysis and Portfolio Management (SAPM) E-Lecture Notes (For MBA) IMS, MGKVP, Session 2020Sukanya ShridharNessuna valutazione finora

- Topic 2 - Equity 1 AnsDocumento6 pagineTopic 2 - Equity 1 AnsGaba RieleNessuna valutazione finora

- UNit 4 Introduction of Portfolio MGT - SDocumento43 pagineUNit 4 Introduction of Portfolio MGT - SKeyur KevadiyaNessuna valutazione finora

- Definition of 'Dividend Discount Model - DDM'Documento2 pagineDefinition of 'Dividend Discount Model - DDM'Siddhesh PatwaNessuna valutazione finora

- Module Iv Capital Structure÷nd DecisionsDocumento37 pagineModule Iv Capital Structure÷nd DecisionsMidhun George VargheseNessuna valutazione finora

- FMF T8 DoneDocumento10 pagineFMF T8 DoneThongkit ThoNessuna valutazione finora

- Research Proposal For Portfolio Management in Banking, IT and Pharmaceutical SectorDocumento6 pagineResearch Proposal For Portfolio Management in Banking, IT and Pharmaceutical Sectorzalaks67% (3)

- Equity Portfolio Management Strategies and Evaluation of Portfolio PerformanceDocumento10 pagineEquity Portfolio Management Strategies and Evaluation of Portfolio PerformanceChinmayee ChoudhuryNessuna valutazione finora

- Investment & Risk ManagementDocumento5 pagineInvestment & Risk ManagementE-sabat RizviNessuna valutazione finora

- SIM - ACC 212 - Week 8-9 - ULOb CAPMDocumento16 pagineSIM - ACC 212 - Week 8-9 - ULOb CAPMDaisy GuiralNessuna valutazione finora

- TOPIC 7 & 8 - Portfolio MGTDocumento15 pagineTOPIC 7 & 8 - Portfolio MGTDaniel DakaNessuna valutazione finora

- Chapter 1Documento23 pagineChapter 1Pablo EkskobaNessuna valutazione finora

- MAF 680 Chapter 7 - Futures Derivatives (New)Documento89 pagineMAF 680 Chapter 7 - Futures Derivatives (New)Pablo EkskobaNessuna valutazione finora

- Maf 630 Chapter 11Documento6 pagineMaf 630 Chapter 11Pablo EkskobaNessuna valutazione finora

- Maf 630 Chapter 6Documento5 pagineMaf 630 Chapter 6Pablo EkskobaNessuna valutazione finora

- Maf 630 CHAPTER 7Documento3 pagineMaf 630 CHAPTER 7Pablo EkskobaNessuna valutazione finora

- Maf 630 Chapter 4Documento2 pagineMaf 630 Chapter 4Pablo EkskobaNessuna valutazione finora

- Maf 630 Chapter 8Documento4 pagineMaf 630 Chapter 8Pablo EkskobaNessuna valutazione finora

- Chapter 5: Malaysian Bond MarketDocumento4 pagineChapter 5: Malaysian Bond MarketPablo EkskobaNessuna valutazione finora

- Maf 630 Chapter 1Documento3 pagineMaf 630 Chapter 1Pablo EkskobaNessuna valutazione finora

- Solution Far450 - Jun 2014Documento7 pagineSolution Far450 - Jun 2014Pablo EkskobaNessuna valutazione finora

- Far450 A April 2011Documento8 pagineFar450 A April 2011Pablo EkskobaNessuna valutazione finora

- Far450 A April 2011Documento8 pagineFar450 A April 2011Pablo EkskobaNessuna valutazione finora

- Suggested Solution FAR450 - JUNE 2012 Solution 1ADocumento8 pagineSuggested Solution FAR450 - JUNE 2012 Solution 1APablo EkskobaNessuna valutazione finora

- Share BuybackDocumento3 pagineShare Buybackurcrazy_mateNessuna valutazione finora

- NCA Held For Sale and Disc Operation-DiscussionDocumento3 pagineNCA Held For Sale and Disc Operation-DiscussionJennifer ArcadioNessuna valutazione finora

- Professional Development Portfolio GuidanceDocumento10 pagineProfessional Development Portfolio GuidancehoheinheimNessuna valutazione finora

- Lean - Total Productive MaintenanceDocumento9 pagineLean - Total Productive MaintenanceBalaji SNessuna valutazione finora

- GeM Bidding 4885013Documento4 pagineGeM Bidding 4885013MaheshNessuna valutazione finora

- Cost and Benefit Analysis of Outsourcing From The Perspective of Datapath LTDDocumento59 pagineCost and Benefit Analysis of Outsourcing From The Perspective of Datapath LTDranzlorenzoo100% (1)

- Ef1c HDT Sharemarket PCB3Documento37 pagineEf1c HDT Sharemarket PCB3PRATIK PRAKASHNessuna valutazione finora

- Government ProcurementDocumento4 pagineGovernment ProcurementPauline Vistan GarciaNessuna valutazione finora

- Algorithmic Trading Directory 2010Documento100 pagineAlgorithmic Trading Directory 201017524100% (4)

- Operations Management-Chapter FiveDocumento64 pagineOperations Management-Chapter FiveAGNessuna valutazione finora

- Enron ScandalDocumento9 pagineEnron ScandalRohith MohanNessuna valutazione finora

- EU Transition Timeline Whitepaper PDFDocumento10 pagineEU Transition Timeline Whitepaper PDFWFreeNessuna valutazione finora

- Applying Value Stream Mapping Technique in Apparel IndustryDocumento9 pagineApplying Value Stream Mapping Technique in Apparel IndustryAbhinav Ashish100% (1)

- Work Life Balance TechniquesDocumento2 pagineWork Life Balance TechniquestusharNessuna valutazione finora

- International Banking and Future of Banking and FinancialDocumento12 pagineInternational Banking and Future of Banking and FinancialAmit Mishra0% (1)

- The Importance of Independence.: Q:-Who Is Subject To Independence Restrictions?Documento5 pagineThe Importance of Independence.: Q:-Who Is Subject To Independence Restrictions?anon-583391Nessuna valutazione finora

- Innovation: Innovated by Professor Vijay Govindarajan, Tuck School of Business, Dartmouth CollegeDocumento13 pagineInnovation: Innovated by Professor Vijay Govindarajan, Tuck School of Business, Dartmouth CollegeManikandan SuriyanarayananNessuna valutazione finora

- CFMB AS CS3 v3Documento6 pagineCFMB AS CS3 v3lawless.d90Nessuna valutazione finora

- 1844 RulesDocumento20 pagine1844 RulestobymaoNessuna valutazione finora

- Chapter 8 Entry Strategies in Global BusinessDocumento3 pagineChapter 8 Entry Strategies in Global BusinessMariah Dion GalizaNessuna valutazione finora

- 2020 Walmart Annual ReportDocumento88 pagine2020 Walmart Annual ReportPruthviraj DhinganiNessuna valutazione finora

- Centre For Innovation, Incubation and Entrepreneurship (CIIE)Documento13 pagineCentre For Innovation, Incubation and Entrepreneurship (CIIE)Manish Singh RathorNessuna valutazione finora

- Comparative Analysis of Mutual Funds With Special Reference To Bajaj CapitalDocumento13 pagineComparative Analysis of Mutual Funds With Special Reference To Bajaj Capitalpankajbhatt1993Nessuna valutazione finora

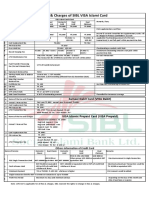

- Fees and Charges of SIBL Islami CardDocumento1 paginaFees and Charges of SIBL Islami CardMd YusufNessuna valutazione finora

- PDF 2Documento8 paginePDF 2ronnelNessuna valutazione finora

- BFIN300 Full Hands OutDocumento46 pagineBFIN300 Full Hands OutGauray LionNessuna valutazione finora