Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- State Health CoverageDocumento26 pagineState Health CoveragejspectorNessuna valutazione finora

- Cornell ComplaintDocumento41 pagineCornell Complaintjspector100% (1)

- Pennies For Charity 2018Documento12 paginePennies For Charity 2018ZacharyEJWilliamsNessuna valutazione finora

- IG LetterDocumento3 pagineIG Letterjspector100% (1)

- Federal Budget Fiscal Year 2017 Web VersionDocumento36 pagineFederal Budget Fiscal Year 2017 Web VersionjspectorNessuna valutazione finora

- Joseph Ruggiero Employment AgreementDocumento6 pagineJoseph Ruggiero Employment AgreementjspectorNessuna valutazione finora

- Teacher Shortage Report 05232017 PDFDocumento16 pagineTeacher Shortage Report 05232017 PDFjspectorNessuna valutazione finora

- NYSCrimeReport2016 PrelimDocumento14 pagineNYSCrimeReport2016 PrelimjspectorNessuna valutazione finora

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocumento8 pagineFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorNessuna valutazione finora

- Abo 2017 Annual ReportDocumento65 pagineAbo 2017 Annual ReportrkarlinNessuna valutazione finora

- Inflation AllowablegrowthfactorsDocumento1 paginaInflation AllowablegrowthfactorsjspectorNessuna valutazione finora

- Darweesh Cities AmicusDocumento32 pagineDarweesh Cities AmicusjspectorNessuna valutazione finora

- 2017 08 18 Constitution OrderDocumento27 pagine2017 08 18 Constitution OrderjspectorNessuna valutazione finora

- SNY0517 Crosstabs 052417Documento4 pagineSNY0517 Crosstabs 052417Nick ReismanNessuna valutazione finora

- Oag Sed Letter Ice 2-27-17Documento3 pagineOag Sed Letter Ice 2-27-17BethanyNessuna valutazione finora

- Class of 2022Documento1 paginaClass of 2022jspectorNessuna valutazione finora

- Opiods 2017-04-20-By Numbers Brief No8Documento17 pagineOpiods 2017-04-20-By Numbers Brief No8rkarlinNessuna valutazione finora

- 2017 School Bfast Report Online Version 3-7-17 0Documento29 pagine2017 School Bfast Report Online Version 3-7-17 0jspectorNessuna valutazione finora

- Youth Cigarette and E-Cigs UseDocumento1 paginaYouth Cigarette and E-Cigs UsejspectorNessuna valutazione finora

- Hiffa Settlement Agreement ExecutedDocumento5 pagineHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- Schneiderman Voter Fraud Letter 022217Documento2 pagineSchneiderman Voter Fraud Letter 022217Matthew HamiltonNessuna valutazione finora

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Documento4 pagineActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorNessuna valutazione finora

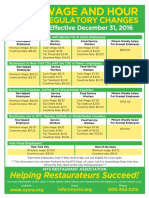

- Wage and Hour Regulatory Changes 2016Documento2 pagineWage and Hour Regulatory Changes 2016jspectorNessuna valutazione finora

- Siena Poll March 27, 2017Documento7 pagineSiena Poll March 27, 2017jspectorNessuna valutazione finora

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocumento55 pagine16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorNessuna valutazione finora

- Review of Executive Budget 2017Documento102 pagineReview of Executive Budget 2017Nick ReismanNessuna valutazione finora

- p12 Budget Testimony 2-14-17Documento31 paginep12 Budget Testimony 2-14-17jspectorNessuna valutazione finora

- Pub Auth Num 2017Documento54 paginePub Auth Num 2017jspectorNessuna valutazione finora

- 2016 Local Sales Tax CollectionsDocumento4 pagine2016 Local Sales Tax CollectionsjspectorNessuna valutazione finora

- Voting Report CardDocumento1 paginaVoting Report CardjspectorNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (120)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Entrepreneurial ProcessDocumento13 pagineThe Entrepreneurial ProcessNgoni Mukuku100% (1)

- Freehold and LeaseholdDocumento3 pagineFreehold and LeaseholdDayah AyoebNessuna valutazione finora

- Problem Set 2Documento2 pagineProblem Set 2Rubab MirzaNessuna valutazione finora

- Strategic Management ModelsDocumento24 pagineStrategic Management ModelsAnubhav DubeyNessuna valutazione finora

- Jafza Rules 6th Edition 2016Documento58 pagineJafza Rules 6th Edition 2016Binoy PsNessuna valutazione finora

- Aug 2020 Builders Line Tamil MonthlyDocumento48 pagineAug 2020 Builders Line Tamil MonthlyBuildersLineMonthlyNessuna valutazione finora

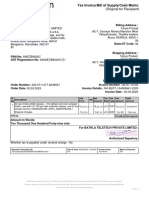

- InvoiceDocumento1 paginaInvoicetanya.prasadNessuna valutazione finora

- Kotak Mahindra GroupDocumento6 pagineKotak Mahindra GroupNitesh AswalNessuna valutazione finora

- GRC Expert - User Access Reviews1Documento11 pagineGRC Expert - User Access Reviews1Rohit KumarNessuna valutazione finora

- Kabushi Kaisha Isetan Vs IacDocumento2 pagineKabushi Kaisha Isetan Vs IacJudee Anne100% (2)

- Lazaro Vs SSSDocumento2 pagineLazaro Vs SSSFatima Briones100% (1)

- The Need For Time Management Training Is Universal: Evidence From TurkeyDocumento8 pagineThe Need For Time Management Training Is Universal: Evidence From TurkeyAnil AkhterNessuna valutazione finora

- World Airports Freighters: FreighDocumento16 pagineWorld Airports Freighters: FreighBobbie KhunthongchanNessuna valutazione finora

- CR 2015Documento13 pagineCR 2015Agr AcabdiaNessuna valutazione finora

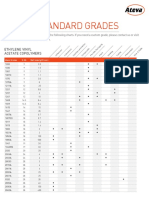

- !!!EVA 019 AtevaOverviewGradesSheet TS EN 0416 PDFDocumento2 pagine!!!EVA 019 AtevaOverviewGradesSheet TS EN 0416 PDFSlava75Nessuna valutazione finora

- NAFTA Verification and Audit ManualDocumento316 pagineNAFTA Verification and Audit Manualbiharris22Nessuna valutazione finora

- TRDocumento18 pagineTRharshal49Nessuna valutazione finora

- Bpo Management SystemDocumento12 pagineBpo Management SystembaskarbalachandranNessuna valutazione finora

- What Are Key Performance IndicatorsDocumento13 pagineWhat Are Key Performance IndicatorsKharieh Comb's100% (1)

- EXPORTDocumento99 pagineEXPORTdhruv81275Nessuna valutazione finora

- CommoditiesDocumento122 pagineCommoditiesAnil TiwariNessuna valutazione finora

- Announcement Invitation For Psychotest (October)Documento17 pagineAnnouncement Invitation For Psychotest (October)bgbfbvmnmNessuna valutazione finora

- Bus Boy ServicingDocumento17 pagineBus Boy ServicingChryz SantosNessuna valutazione finora

- Chapter 1Documento4 pagineChapter 1Micaela BakerNessuna valutazione finora

- Keeney v. Larkin, 4th Cir. (2004)Documento4 pagineKeeney v. Larkin, 4th Cir. (2004)Scribd Government DocsNessuna valutazione finora

- Governance, Risk and Dataveillance in The War On TerrorDocumento25 pagineGovernance, Risk and Dataveillance in The War On Terroreliasox123Nessuna valutazione finora

- RAD Project PlanDocumento9 pagineRAD Project PlannasoonyNessuna valutazione finora

- Indian Law Solved Case StudiesDocumento14 pagineIndian Law Solved Case StudiesJay PatelNessuna valutazione finora

- DP World Internship ReportDocumento40 pagineDP World Internship ReportSaurabh100% (1)

- El 1204 HHDocumento6 pagineEl 1204 HHLuis Marcelo HinojosaNessuna valutazione finora