Potrebbero piacerti anche

- ACCT 434 Final Exam (Updated)Documento12 pagineACCT 434 Final Exam (Updated)DeVryHelpNessuna valutazione finora

- DeVry ACCT 434 Final Exam 100% Correct AnswerDocumento9 pagineDeVry ACCT 434 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- Advanced Cost Management MidtermDocumento9 pagineAdvanced Cost Management MidtermAnkit BajajNessuna valutazione finora

- 2011-01-20 235608 Debra J Macchioni mt425 01 Unit 10 FinalDocumento17 pagine2011-01-20 235608 Debra J Macchioni mt425 01 Unit 10 FinalAnonymous dPyHoLNessuna valutazione finora

- ACCT 434 Midterm Exam (Updated)Documento4 pagineACCT 434 Midterm Exam (Updated)DeVryHelpNessuna valutazione finora

- MA2 CGA Sept'12 ExamDocumento19 pagineMA2 CGA Sept'12 Examumgilkin0% (1)

- ACCT 346 Final ExamDocumento7 pagineACCT 346 Final ExamDeVryHelpNessuna valutazione finora

- ADMS 2510 Final Exam W 2005 SolutionsDocumento8 pagineADMS 2510 Final Exam W 2005 SolutionsGrace 'Queen' IfeyiNessuna valutazione finora

- CUACM 413 Tutorial QuestionsDocumento31 pagineCUACM 413 Tutorial Questionstmash3017Nessuna valutazione finora

- Student Sol10 4eDocumento38 pagineStudent Sol10 4eprasad_kcp50% (2)

- F5 RevDocumento69 pagineF5 Revpercy mapetereNessuna valutazione finora

- PM Sunway Test July-Sept 2023 PTDocumento11 paginePM Sunway Test July-Sept 2023 PTFarahAin FainNessuna valutazione finora

- DeVry BUSN 278 Final Exam 100% Correct AnswerDocumento8 pagineDeVry BUSN 278 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- Module Code: PMC Module Name: Performance Measurement & Control Programme: MSC FinanceDocumento9 pagineModule Code: PMC Module Name: Performance Measurement & Control Programme: MSC FinanceRenato WilsonNessuna valutazione finora

- Revision 2Documento37 pagineRevision 2percy mapetereNessuna valutazione finora

- Lsbf.p4 Mock QuesDocumento21 pagineLsbf.p4 Mock Quesjunaid-chandio-458Nessuna valutazione finora

- t4 2008 Dec QDocumento8 paginet4 2008 Dec QShimera RamoutarNessuna valutazione finora

- Tutorial 4Documento6 pagineTutorial 4FEI FEINessuna valutazione finora

- Cga-Canada Management Accounting Fundamentals (Ma1) Examination March 2014 Marks Time: 3 HoursDocumento18 pagineCga-Canada Management Accounting Fundamentals (Ma1) Examination March 2014 Marks Time: 3 HoursasNessuna valutazione finora

- Ac102 ch11Documento19 pagineAc102 ch11Yenny Torro100% (1)

- GNB14 e CH 12 ExamDocumento6 pagineGNB14 e CH 12 Exama_elsaied0% (1)

- Low Cost and Experience CurvesDocumento31 pagineLow Cost and Experience CurvesJuhi ShahNessuna valutazione finora

- Differential Analysis: The Key To Decision MakingDocumento25 pagineDifferential Analysis: The Key To Decision MakingJhinglee Sacupayo Gocela100% (1)

- Model Test Paper Problem1 (A)Documento15 pagineModel Test Paper Problem1 (A)HibibiNessuna valutazione finora

- F5 CKT Mock1Documento8 pagineF5 CKT Mock1OMID_JJNessuna valutazione finora

- Garrison (Asian Edition) Practice Exam - Chapter 14Documento5 pagineGarrison (Asian Edition) Practice Exam - Chapter 14mariko1234Nessuna valutazione finora

- Pricing and Short Term Decision Making (Edited)Documento58 paginePricing and Short Term Decision Making (Edited)Vaibhav SuchdevaNessuna valutazione finora

- Solutions - Chapter 5Documento12 pagineSolutions - Chapter 5Parul AbrolNessuna valutazione finora

- MGT and Cost ActgDocumento14 pagineMGT and Cost Actgdanjay2792Nessuna valutazione finora

- Saa P5Documento12 pagineSaa P5smartguy0Nessuna valutazione finora

- Managerial AccountingDocumento8 pagineManagerial AccountingPaula Cxerna Gacis100% (1)

- Acct1003 Midsemester Exam08-09 SOLUTIONSDocumento7 pagineAcct1003 Midsemester Exam08-09 SOLUTIONSKimberly KangalooNessuna valutazione finora

- 2009-02-05 171631 Lynn 1Documento13 pagine2009-02-05 171631 Lynn 1Ashish BhallaNessuna valutazione finora

- Section C Part 2 MCQDocumento344 pagineSection C Part 2 MCQSaiswetha BethiNessuna valutazione finora

- F5 Mapit Workbook Questions PDFDocumento88 pagineF5 Mapit Workbook Questions PDFBeryl Maliakkal0% (1)

- ACCT 505 Week 6 Quiz Segment Reporting and Relevant Costs For DecisionsDocumento7 pagineACCT 505 Week 6 Quiz Segment Reporting and Relevant Costs For DecisionsNatasha DeclanNessuna valutazione finora

- SA Syl12 Jun2014 P10 PDFDocumento21 pagineSA Syl12 Jun2014 P10 PDFpatil_viny1760Nessuna valutazione finora

- SolutionDocumento5 pagineSolutionNur Aina Safwani ZainoddinNessuna valutazione finora

- Paper T7 Planning Control and Performance Management: Sample Multiple Choice Questions - June 2009Documento152 paginePaper T7 Planning Control and Performance Management: Sample Multiple Choice Questions - June 2009GT Boss AvyLara50% (4)

- ACC102-Chapter10new 000Documento28 pagineACC102-Chapter10new 000Mikee FactoresNessuna valutazione finora

- Chapters 8 - 13 - 14 - 15 QuestionsDocumento5 pagineChapters 8 - 13 - 14 - 15 QuestionsJamie N Clint BrendleNessuna valutazione finora

- ABC CostingDocumento5 pagineABC CostingMike RobmonNessuna valutazione finora

- 8508 Managerial AccountingDocumento10 pagine8508 Managerial AccountingHassan Malik100% (1)

- Class Note - Chpt12 Decision MakingDocumento19 pagineClass Note - Chpt12 Decision MakingNicole LinNessuna valutazione finora

- Decsion Analysis Printing Hock ExamsuccessDocumento92 pagineDecsion Analysis Printing Hock ExamsuccessJane Michelle EmanNessuna valutazione finora

- Session 08: Tactical Decision MakingDocumento18 pagineSession 08: Tactical Decision MakingFrancisco Pedro SantosNessuna valutazione finora

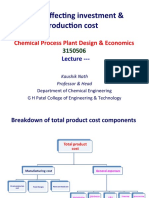

- Lecture 17 - Factors Affecting Investment and Production CostDocumento17 pagineLecture 17 - Factors Affecting Investment and Production CostGoa TripNessuna valutazione finora

- CH 11 and 11A - CLASS NOTES - MOS 3370 - KINGS - FALL 2023-1Documento55 pagineCH 11 and 11A - CLASS NOTES - MOS 3370 - KINGS - FALL 2023-1niweisheng28Nessuna valutazione finora

- Costs of Production 1Documento23 pagineCosts of Production 1Daksh AnejaNessuna valutazione finora

- PM MJ21 Examiner's ReportDocumento21 paginePM MJ21 Examiner's ReportleylaNessuna valutazione finora

- Quiz Week 2 NewDocumento4 pagineQuiz Week 2 NewMuhammad M BhattiNessuna valutazione finora

- F5-Test1 (Costing)Documento7 pagineF5-Test1 (Costing)Amna HussainNessuna valutazione finora

- Manufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesDa EverandManufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesValutazione: 4.5 su 5 stelle4.5/5 (3)

- Practice Questions for UiPath Certified RPA Associate Case BasedDa EverandPractice Questions for UiPath Certified RPA Associate Case BasedNessuna valutazione finora

- Creating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowDa EverandCreating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowValutazione: 4 su 5 stelle4/5 (1)

- Cost & Managerial Accounting II EssentialsDa EverandCost & Managerial Accounting II EssentialsValutazione: 4 su 5 stelle4/5 (1)

- Computer Modeling for Injection Molding: Simulation, Optimization, and ControlDa EverandComputer Modeling for Injection Molding: Simulation, Optimization, and ControlHuamin ZhouNessuna valutazione finora

- DeVry SBE 430 Final Exam 100% Correct AnswerDocumento9 pagineDeVry SBE 430 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- HRM 582 Final ExamDocumento8 pagineHRM 582 Final ExamDeVryHelpNessuna valutazione finora

- GSCM 209 Final ExamDocumento4 pagineGSCM 209 Final ExamDeVryHelpNessuna valutazione finora

- GSCM 326 Final Exam (Updated)Documento6 pagineGSCM 326 Final Exam (Updated)DeVryHelpNessuna valutazione finora

- FIN 515 Final ExamDocumento3 pagineFIN 515 Final ExamDeVryHelpNessuna valutazione finora

- HRM 430 Final ExamDocumento5 pagineHRM 430 Final ExamDeVryHelpNessuna valutazione finora

- GSCM 520 Final Exam (UPDATED)Documento10 pagineGSCM 520 Final Exam (UPDATED)DevryFinalExamscomNessuna valutazione finora

- DeVry HUMN 303 Final Exam 100% Correct AnswerDocumento5 pagineDeVry HUMN 303 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry MGMT 520 Final Exam 100% Correct AnswerDocumento3 pagineDeVry MGMT 520 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry HRM 587 Final Exam 100% Correct AnswerDocumento9 pagineDeVry HRM 587 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry HRM 598 Final Exam 100% Correct AnswerDocumento3 pagineDeVry HRM 598 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry BIS 245 Final Exam 100% Correct AnswerDocumento7 pagineDeVry BIS 245 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry MATH 533 Final Exam 100% Correct AnswerDocumento6 pagineDeVry MATH 533 Final Exam 100% Correct AnswerDeVryHelp100% (1)

- HOSP 420 Final Exam (Updated)Documento4 pagineHOSP 420 Final Exam (Updated)DevryFinalExamscomNessuna valutazione finora

- DeVry BUSN 278 Final Exam 100% Correct AnswerDocumento8 pagineDeVry BUSN 278 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- GSCM 326 Final Exam 1 (UPDATED)Documento5 pagineGSCM 326 Final Exam 1 (UPDATED)DevryFinalExamscomNessuna valutazione finora

- GSCM 326 Final Exam (UPDATED)Documento5 pagineGSCM 326 Final Exam (UPDATED)DevryFinalExamscomNessuna valutazione finora

- DeVry BUSN 379 Final Exam 100% Correct AnswerDocumento17 pagineDeVry BUSN 379 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry BUSN 427 Final Exam 100% Correct AnswerDocumento10 pagineDeVry BUSN 427 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry ECOM 210 Final Exam 100% Correct AnswerDocumento5 pagineDeVry ECOM 210 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry BSOP 588 Final Exam 100% Correct AnswerDocumento4 pagineDeVry BSOP 588 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry BSOP 334 Final Exam 100% Correct AnswerDocumento6 pagineDeVry BSOP 334 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry BSOP 326 Final Exam 100% Correct AnswerDocumento10 pagineDeVry BSOP 326 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry ENGL 216 Final Exam 100% Correct AnswerDocumento7 pagineDeVry ENGL 216 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry BUSN 319 Final Exam 100% Correct AnswerDocumento10 pagineDeVry BUSN 319 Final Exam 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry ACCT 505 Final Exam 1 100% Correct AnswerDocumento4 pagineDeVry ACCT 505 Final Exam 1 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry ACCT 505 Final Exam 2 100% Correct AnswerDocumento12 pagineDeVry ACCT 505 Final Exam 2 100% Correct AnswerDeVryHelpNessuna valutazione finora

- DeVry ACCT 504 Final Exam 1 100% Correct AnswerDocumento7 pagineDeVry ACCT 504 Final Exam 1 100% Correct AnswerDeVryHelpNessuna valutazione finora

- Community-Based Monitoring System (CBMS) : An Overview: Celia M. ReyesDocumento28 pagineCommunity-Based Monitoring System (CBMS) : An Overview: Celia M. ReyesDiane Rose LacenaNessuna valutazione finora

- Attachment BinaryDocumento5 pagineAttachment BinaryMonali PawarNessuna valutazione finora

- Mcqs in Wills and SuccessionDocumento14 pagineMcqs in Wills and Successionjudy andrade100% (1)

- SKF LGMT-2 Data SheetDocumento2 pagineSKF LGMT-2 Data SheetRahul SharmaNessuna valutazione finora

- I.V. FluidDocumento4 pagineI.V. FluidOdunlamiNessuna valutazione finora

- Spare Parts ManagementDocumento21 pagineSpare Parts Managementdajit1100% (1)

- The April Fair in Seville: Word FormationDocumento2 pagineThe April Fair in Seville: Word FormationДархан МакыжанNessuna valutazione finora

- 1 075 Syn4e PDFDocumento2 pagine1 075 Syn4e PDFSalvador FayssalNessuna valutazione finora

- COVID Immunization Record Correction RequestDocumento2 pagineCOVID Immunization Record Correction RequestNBC 10 WJARNessuna valutazione finora

- BS As On 23-09-2023Documento28 pagineBS As On 23-09-2023Farooq MaqboolNessuna valutazione finora

- Pediatric Skills For OT Assistants 3rd Ed.Documento645 paginePediatric Skills For OT Assistants 3rd Ed.Patrice Escobar100% (1)

- Colibri - DEMSU P01 PDFDocumento15 pagineColibri - DEMSU P01 PDFRahul Solanki100% (4)

- Sikkim Manipal MBA 1 SEM MB0038-Management Process and Organization Behavior-MQPDocumento15 pagineSikkim Manipal MBA 1 SEM MB0038-Management Process and Organization Behavior-MQPHemant MeenaNessuna valutazione finora

- SPIE Oil & Gas Services: Pressure VesselsDocumento56 pagineSPIE Oil & Gas Services: Pressure VesselsSadashiw PatilNessuna valutazione finora

- PRELEC 1 Updates in Managerial Accounting Notes PDFDocumento6 paginePRELEC 1 Updates in Managerial Accounting Notes PDFRaichele FranciscoNessuna valutazione finora

- Enumerator ResumeDocumento1 paginaEnumerator Resumesaid mohamudNessuna valutazione finora

- CoP - 6.0 - Emergency Management RequirementsDocumento25 pagineCoP - 6.0 - Emergency Management RequirementsAnonymous y1pIqcNessuna valutazione finora

- Incoterms 2010 PresentationDocumento47 pagineIncoterms 2010 PresentationBiswajit DuttaNessuna valutazione finora

- Stainless Steel 1.4404 316lDocumento3 pagineStainless Steel 1.4404 316lDilipSinghNessuna valutazione finora

- La Bugal-b'Laan Tribal Association Et - Al Vs Ramos Et - AlDocumento6 pagineLa Bugal-b'Laan Tribal Association Et - Al Vs Ramos Et - AlMarlouis U. PlanasNessuna valutazione finora

- ACC403 Week 10 Assignment Rebecca MillerDocumento7 pagineACC403 Week 10 Assignment Rebecca MillerRebecca Miller HorneNessuna valutazione finora

- Appleyard ResúmenDocumento3 pagineAppleyard ResúmenTomás J DCNessuna valutazione finora

- BS en 118-2013-11Documento22 pagineBS en 118-2013-11Abey VettoorNessuna valutazione finora

- Cara Membuat Motivation LetterDocumento5 pagineCara Membuat Motivation LetterBayu Ade Krisna0% (1)

- Common OPCRF Contents For 2021 2022 FINALE 2Documento21 pagineCommon OPCRF Contents For 2021 2022 FINALE 2JENNIFER FONTANILLA100% (30)

- CEC Proposed Additional Canopy at Guard House (RFA-2021!09!134) (Signed 23sep21)Documento3 pagineCEC Proposed Additional Canopy at Guard House (RFA-2021!09!134) (Signed 23sep21)MichaelNessuna valutazione finora

- MDC PT ChartDocumento2 pagineMDC PT ChartKailas NimbalkarNessuna valutazione finora

- A.2 de - La - Victoria - v. - Commission - On - Elections20210424-12-18iwrdDocumento6 pagineA.2 de - La - Victoria - v. - Commission - On - Elections20210424-12-18iwrdCharisse SarateNessuna valutazione finora

- จัดตารางสอบกลางภาคภาคต้น53Documento332 pagineจัดตารางสอบกลางภาคภาคต้น53Yuwarath SuktrakoonNessuna valutazione finora

- Dbms UPDATED MANUAL EWITDocumento75 pagineDbms UPDATED MANUAL EWITMadhukesh .kNessuna valutazione finora