Potrebbero piacerti anche

- What Is The Case Study Method ? How Can You Use It To Write Case Solution For The WORKS Gourmet Burger Bistro Case Study?Documento9 pagineWhat Is The Case Study Method ? How Can You Use It To Write Case Solution For The WORKS Gourmet Burger Bistro Case Study?Divya RaghuvanshiNessuna valutazione finora

- 03.McAfee. Mastering The Three Worlds of Information TechnologyDocumento10 pagine03.McAfee. Mastering The Three Worlds of Information Technology5oscilantesNessuna valutazione finora

- Acquisition of Tetley by TataDocumento3 pagineAcquisition of Tetley by TataANUSHRI MAYEKARNessuna valutazione finora

- Beach Nut Nutrition Corporation (A1)Documento3 pagineBeach Nut Nutrition Corporation (A1)Nav EedNessuna valutazione finora

- IB SummaryDocumento7 pagineIB SummaryrronakrjainNessuna valutazione finora

- Assignment 1 IbsDocumento11 pagineAssignment 1 IbsSash ChatterjeeNessuna valutazione finora

- AOL.com (Review and Analysis of Swisher's Book)Da EverandAOL.com (Review and Analysis of Swisher's Book)Nessuna valutazione finora

- Hostile TakeoverDocumento3 pagineHostile TakeoverAlexandru Cristian PoenaruNessuna valutazione finora

- OracleDocumento2 pagineOracleaj4u7Nessuna valutazione finora

- Statue of Unity in Shortlist For Best Engineered Structures PDFDocumento2 pagineStatue of Unity in Shortlist For Best Engineered Structures PDFIndra Nath MishraNessuna valutazione finora

- Analysis On Combating Hostile TakeoversDocumento14 pagineAnalysis On Combating Hostile TakeoversLAW MANTRANessuna valutazione finora

- Explain Apple's Success Over The Last Decade. Think About Which Industries It Has Disrupted and How. Also Look at Apple's Main CompetitorsDocumento5 pagineExplain Apple's Success Over The Last Decade. Think About Which Industries It Has Disrupted and How. Also Look at Apple's Main CompetitorsPui YanNessuna valutazione finora

- Presentation On Tata Nano, The Peoples CarDocumento18 paginePresentation On Tata Nano, The Peoples CarShashank IssarNessuna valutazione finora

- TATA Tea's M&A With TetleyDocumento16 pagineTATA Tea's M&A With TetleyChandrakant Hingankar100% (1)

- Moderating Effect of The Relationship Between Private Label Share and Store Loyalty PDFDocumento15 pagineModerating Effect of The Relationship Between Private Label Share and Store Loyalty PDFKhushbooNessuna valutazione finora

- ITC E ChoupalDocumento23 pagineITC E Choupalgag90Nessuna valutazione finora

- INFOSYS LTD CGDocumento6 pagineINFOSYS LTD CGAshish ChdNessuna valutazione finora

- Case Reinventing Tata Steel (Part A) .01.12.05Documento16 pagineCase Reinventing Tata Steel (Part A) .01.12.05Tushar JadhavNessuna valutazione finora

- Group1 - Section A - Aravind Eye CareDocumento6 pagineGroup1 - Section A - Aravind Eye CareGopichand AthukuriNessuna valutazione finora

- BL QP EPGP End-Term 2022Documento4 pagineBL QP EPGP End-Term 2022Abhay AgarwalNessuna valutazione finora

- 13 - Chapter 4 PDFDocumento43 pagine13 - Chapter 4 PDFSan DeepNessuna valutazione finora

- Trend Analysis of Ultratech Cement - Aditya Birla Group.Documento9 pagineTrend Analysis of Ultratech Cement - Aditya Birla Group.Kanhay VishariaNessuna valutazione finora

- MTI Project Presentation Ideo Product Development PDFDocumento22 pagineMTI Project Presentation Ideo Product Development PDFDamian DeoNessuna valutazione finora

- FreeMove Alliance Group5Documento10 pagineFreeMove Alliance Group5Annisa MoeslimNessuna valutazione finora

- Submission1 - P&G Acquisition of GilletteDocumento9 pagineSubmission1 - P&G Acquisition of GilletteAryan AnandNessuna valutazione finora

- Honda Case Study Full Mike Jett InterviewDocumento8 pagineHonda Case Study Full Mike Jett InterviewSalwa ParachaNessuna valutazione finora

- Ib - Case - 2 TSMC - ModDocumento6 pagineIb - Case - 2 TSMC - ModYoungHoon WonNessuna valutazione finora

- Group 3 FM Project IT IndustryDocumento13 pagineGroup 3 FM Project IT IndustryPS KannanNessuna valutazione finora

- GOO Is Dell's Center For Consolidating Its Global Manufacturing, Procurement and Supply ChainDocumento3 pagineGOO Is Dell's Center For Consolidating Its Global Manufacturing, Procurement and Supply ChainSirsanath BanerjeeNessuna valutazione finora

- Beach NutDocumento4 pagineBeach Nutzain1234567Nessuna valutazione finora

- Program: MBA-Master in Business Administration: Student: Mislav MatijevićDocumento4 pagineProgram: MBA-Master in Business Administration: Student: Mislav MatijevićMislav MatijevićNessuna valutazione finora

- The Case On Tata Nano - The People's CarDocumento4 pagineThe Case On Tata Nano - The People's CarAsm TowheedNessuna valutazione finora

- Hul - GSK Acquisition: A Brief About The EventDocumento2 pagineHul - GSK Acquisition: A Brief About The EventTestNessuna valutazione finora

- Mergers and AmalgmationsDocumento38 pagineMergers and AmalgmationsShweta SawantNessuna valutazione finora

- Kudremukh Iron Ore Co. LTD - The Death Knell and Beyond - Vikalpa - Pages-133-143-Diagnoses-36-2Documento11 pagineKudremukh Iron Ore Co. LTD - The Death Knell and Beyond - Vikalpa - Pages-133-143-Diagnoses-36-2acb562Nessuna valutazione finora

- Final Version of Goodyear Tire CaseDocumento7 pagineFinal Version of Goodyear Tire Casekfrench91100% (1)

- Le Petit Chef Case MemoDocumento7 pagineLe Petit Chef Case MemoashuNessuna valutazione finora

- Operations StartegyDocumento27 pagineOperations StartegySaloni BishnoiNessuna valutazione finora

- Arcelor Mittal+ReportDocumento13 pagineArcelor Mittal+ReportSrikanth DL0% (1)

- Project of Strategic Management Topic: Porters National Competetiveness Model (Single Diamond Model)Documento4 pagineProject of Strategic Management Topic: Porters National Competetiveness Model (Single Diamond Model)shubhamsethi0% (1)

- Timeshare Resorts and Exchanges, Inc.: BUAD 311 Operation Management Case Analysis 1Documento8 pagineTimeshare Resorts and Exchanges, Inc.: BUAD 311 Operation Management Case Analysis 1Anima SharmaNessuna valutazione finora

- SVCM - Group 4 - Case 3Documento2 pagineSVCM - Group 4 - Case 3NehaTaneja0% (1)

- BRL Hardy: Globalizing An Australian Wine CompanyDocumento6 pagineBRL Hardy: Globalizing An Australian Wine CompanyTusharNessuna valutazione finora

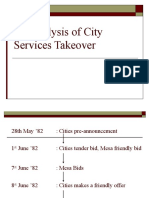

- CitiesService Takeover CaseDocumento20 pagineCitiesService Takeover CasesushilkhannaNessuna valutazione finora

- M&a Project Group-2Documento21 pagineM&a Project Group-2mounicaNessuna valutazione finora

- DMRC Case Analysis PDFDocumento6 pagineDMRC Case Analysis PDFAbhiramyNessuna valutazione finora

- Case Analysis IPremierDocumento18 pagineCase Analysis IPremieravigupta91Nessuna valutazione finora

- Case Report: BRL Hardy: Globalizing An Australian Wine CompanyDocumento5 pagineCase Report: BRL Hardy: Globalizing An Australian Wine CompanyShruti SankarNessuna valutazione finora

- HULDocumento10 pagineHULSALONI GOYALNessuna valutazione finora

- Tata Tea and TetleyDocumento28 pagineTata Tea and Tetleyfakeprofile74100% (2)

- Mi CaseDocumento3 pagineMi CaseVaibhav DograNessuna valutazione finora

- Case Memo #3Documento3 pagineCase Memo #3Iris WangNessuna valutazione finora

- Le PetitDocumento3 pagineLe PetitHarish Chandra JoshiNessuna valutazione finora

- GlobeDocumento10 pagineGlobeAnimesh KumarNessuna valutazione finora

- Presented by - Abilash D Reddy Ravindar .R Sandarsh SureshDocumento15 paginePresented by - Abilash D Reddy Ravindar .R Sandarsh SureshSandarsh SureshNessuna valutazione finora

- EkohealthDocumento3 pagineEkohealthSARATH RAM P PGP 2019-21 BatchNessuna valutazione finora

- HRM - Labour UnrestDocumento20 pagineHRM - Labour Unrestvishal shivkar100% (2)

- M&a - Case DetailsDocumento5 pagineM&a - Case DetailsBinoti PutchuNessuna valutazione finora

- Mergers and AcquisationsDocumento33 pagineMergers and AcquisationsAnku SharmaNessuna valutazione finora

- Merger, Acqusitions, EtcDocumento9 pagineMerger, Acqusitions, EtcSubin Suresh KumarNessuna valutazione finora

- Rider Isbm 2016Documento12 pagineRider Isbm 2016AyushJainNessuna valutazione finora

- Hostile Takeover CaseDocumento11 pagineHostile Takeover CaseAyushJainNessuna valutazione finora

- CG ProjectDocumento11 pagineCG ProjectAyushJainNessuna valutazione finora

- Ajays BankDocumento18 pagineAjays BankAyushJainNessuna valutazione finora

- Fixed Deposit: Milan Das Shweta Tindwani Abhishek Kumar Singh Rishu Nandeshwar Ayush JainDocumento10 pagineFixed Deposit: Milan Das Shweta Tindwani Abhishek Kumar Singh Rishu Nandeshwar Ayush JainAyushJainNessuna valutazione finora

- Risk and Return: Portfolio Theory and Asset Pricing ModelsDocumento44 pagineRisk and Return: Portfolio Theory and Asset Pricing ModelsryaniskakNessuna valutazione finora

- Presented By-AYUSH JAIN - 15005 Prashant Kumar-15017 Pushpender Singh-15021 Presented To - DR AbhilashaDocumento16 paginePresented By-AYUSH JAIN - 15005 Prashant Kumar-15017 Pushpender Singh-15021 Presented To - DR AbhilashaAyushJainNessuna valutazione finora

- Cosmic Handbook PreviewDocumento9 pagineCosmic Handbook PreviewnkjkjkjNessuna valutazione finora

- Electromagnetism WorksheetDocumento3 pagineElectromagnetism WorksheetGuan Jie KhooNessuna valutazione finora

- Generator ControllerDocumento21 pagineGenerator ControllerBrianHazeNessuna valutazione finora

- Cocaine in Blood of Coca ChewersDocumento10 pagineCocaine in Blood of Coca ChewersKarl-GeorgNessuna valutazione finora

- Model Answer Winter 2015Documento38 pagineModel Answer Winter 2015Vivek MalwadeNessuna valutazione finora

- Community Resource MobilizationDocumento17 pagineCommunity Resource Mobilizationerikka june forosueloNessuna valutazione finora

- VerificationManual en PDFDocumento621 pagineVerificationManual en PDFurdanetanpNessuna valutazione finora

- New Microsoft Office Word DocumentDocumento5 pagineNew Microsoft Office Word DocumentSukanya SinghNessuna valutazione finora

- The Serious Student of HistoryDocumento5 pagineThe Serious Student of HistoryCrisanto King CortezNessuna valutazione finora

- Cpar ReviewerDocumento6 pagineCpar ReviewerHana YeppeodaNessuna valutazione finora

- PNGRB - Electrical Safety Audit ChecklistDocumento4 paginePNGRB - Electrical Safety Audit ChecklistKritarth SrivastavNessuna valutazione finora

- The History of Music in Portugal - Owen ReesDocumento4 pagineThe History of Music in Portugal - Owen ReeseugenioamorimNessuna valutazione finora

- MPT EnglishDocumento5 pagineMPT Englishkhadijaamir435Nessuna valutazione finora

- 6 Uec ProgramDocumento21 pagine6 Uec Programsubramanyam62Nessuna valutazione finora

- Assembly InstructionsDocumento4 pagineAssembly InstructionsAghzuiNessuna valutazione finora

- Module 2Documento7 pagineModule 2karthik karti100% (1)

- SXV RXV ChassisDocumento239 pagineSXV RXV Chassischili_s16Nessuna valutazione finora

- VLSI Implementation of Floating Point AdderDocumento46 pagineVLSI Implementation of Floating Point AdderParamesh Waran100% (1)

- Compact 1.8" Height Standardized Installation 9 Months To Flight Powerful and LightweightDocumento2 pagineCompact 1.8" Height Standardized Installation 9 Months To Flight Powerful and LightweightStanley Ochieng' OumaNessuna valutazione finora

- ASHRAE Elearning Course List - Order FormDocumento4 pagineASHRAE Elearning Course List - Order Formsaquib715Nessuna valutazione finora

- University Fees Structure (Himalayan Garhwal University) - UttarakhandDocumento1 paginaUniversity Fees Structure (Himalayan Garhwal University) - UttarakhandabhaybaranwalNessuna valutazione finora

- Beautiful SpotsDocumento2 pagineBeautiful SpotsLouise Yongco100% (1)

- Atlascopco XAHS 175 DD ASL Parts ListDocumento141 pagineAtlascopco XAHS 175 DD ASL Parts ListMoataz SamiNessuna valutazione finora

- SKF Shaft Alignment Tool TKSA 41Documento2 pagineSKF Shaft Alignment Tool TKSA 41Dwiki RamadhaniNessuna valutazione finora

- JCIPDocumento5 pagineJCIPdinesh.nayak.bbsrNessuna valutazione finora

- Beer Pilkhani DistilleryDocumento44 pagineBeer Pilkhani DistillerySunil Vicky VohraNessuna valutazione finora

- For ClosureDocumento18 pagineFor Closuremau_cajipeNessuna valutazione finora

- Exam First Grading 2nd Semester - ReadingDocumento3 pagineExam First Grading 2nd Semester - ReadingArleneRamosNessuna valutazione finora

- Slides - SARSDocumento191 pagineSlides - SARSCedric PoolNessuna valutazione finora

- Icici PrudentialDocumento52 pagineIcici PrudentialDeepak DevaniNessuna valutazione finora