Potrebbero piacerti anche

- Global Governance of Financial SystemsDocumento328 pagineGlobal Governance of Financial SystemsNugroho PurwonoNessuna valutazione finora

- Group 135 GreeceDocumento18 pagineGroup 135 GreeceAndrei SpqNessuna valutazione finora

- Sovereign Wealth Funds: Legitimacy, Governance, and Global PowerDa EverandSovereign Wealth Funds: Legitimacy, Governance, and Global PowerValutazione: 4 su 5 stelle4/5 (2)

- Financial Market SupervisionDocumento28 pagineFinancial Market SupervisionsoufianvipNessuna valutazione finora

- Structural Causes of The Global Financial Crisis A Critical Assessment of The New Financial ArchitectureDocumento18 pagineStructural Causes of The Global Financial Crisis A Critical Assessment of The New Financial ArchitectureremivictorinNessuna valutazione finora

- Business Resilience in the Pandemic and Beyond: Adaptation, innovation, financing and climate action from Eastern Europe to Central AsiaDa EverandBusiness Resilience in the Pandemic and Beyond: Adaptation, innovation, financing and climate action from Eastern Europe to Central AsiaNessuna valutazione finora

- Conclusions and Recommendations: FindingsDocumento8 pagineConclusions and Recommendations: FindingsBruno PaulNessuna valutazione finora

- Globalisation of Financial MarketDocumento17 pagineGlobalisation of Financial MarketPiya SharmaNessuna valutazione finora

- Multi 0 PageDocumento57 pagineMulti 0 PageKatrina ReyesNessuna valutazione finora

- Understanding Financial Consolidation: KeynoteaddressDocumento5 pagineUnderstanding Financial Consolidation: KeynoteaddressmeetsvkNessuna valutazione finora

- LSE - The Future of FinanceDocumento294 pagineLSE - The Future of FinancethirdeyepNessuna valutazione finora

- Introduction To Finance Markets Investments and Financial Management 15Th Edition Melicher Solutions Manual Full Chapter PDFDocumento36 pagineIntroduction To Finance Markets Investments and Financial Management 15Th Edition Melicher Solutions Manual Full Chapter PDFmargaret.clark112100% (12)

- Introduction To Finance Markets Investments and Financial Management 15th Edition Melicher Solutions Manual 1Documento13 pagineIntroduction To Finance Markets Investments and Financial Management 15th Edition Melicher Solutions Manual 1samanthahortoncbdsetjaxr100% (25)

- Notes On Finance Capital and Imperialism Today: The MarxistDocumento15 pagineNotes On Finance Capital and Imperialism Today: The MarxistNachiket KulkarniNessuna valutazione finora

- Financial System Resilience Lessons From A Real Stress Speech by Jon CunliffeDocumento12 pagineFinancial System Resilience Lessons From A Real Stress Speech by Jon CunliffeHao WangNessuna valutazione finora

- Documentos de Política Económica: Banco Central de ChileDocumento29 pagineDocumentos de Política Económica: Banco Central de Chileroberticounico1974Nessuna valutazione finora

- Indonesia - A Tale of Three Crises - Iwan AzizDocumento50 pagineIndonesia - A Tale of Three Crises - Iwan AzizAlisa Syakila MaharaniNessuna valutazione finora

- Effects of Global Financial CrisisDocumento10 pagineEffects of Global Financial CrisisHusseinNessuna valutazione finora

- Qef 141Documento44 pagineQef 141werner71Nessuna valutazione finora

- Economic and Financial Situation in Asia: Latest DevelopmentsDocumento7 pagineEconomic and Financial Situation in Asia: Latest DevelopmentsLizette MacatangayNessuna valutazione finora

- Crises Managed 30-11-11Documento24 pagineCrises Managed 30-11-11Lubomir ChristoffNessuna valutazione finora

- Summer in The City - Banking Failures of 1974 and The Development of International Banking SupervisionDocumento28 pagineSummer in The City - Banking Failures of 1974 and The Development of International Banking SupervisionImran HussainNessuna valutazione finora

- The Changing Role of Financial Intermediation in Europe: April 1998Documento20 pagineThe Changing Role of Financial Intermediation in Europe: April 1998hitesh gayakwadNessuna valutazione finora

- MergerDocumento17 pagineMergerSuresh Kumar manoharanNessuna valutazione finora

- Policy Insight 68Documento13 paginePolicy Insight 68unicycle1234Nessuna valutazione finora

- Show Cgi PDFDocumento55 pagineShow Cgi PDFEugenio MartinezNessuna valutazione finora

- BSA12M1-Globustra: Global FinanceDocumento168 pagineBSA12M1-Globustra: Global FinanceErica Claire VidalNessuna valutazione finora

- Show CgiDocumento56 pagineShow CgiDNYANESHWAR SHINDENessuna valutazione finora

- Current Affairs: CLASS NOTES: 23 Apr - 29 Apr, 2013Documento12 pagineCurrent Affairs: CLASS NOTES: 23 Apr - 29 Apr, 2013Mohan KumarNessuna valutazione finora

- Commission On Growth and Development. Reproduced With Permission. All Rights ReservedDocumento86 pagineCommission On Growth and Development. Reproduced With Permission. All Rights ReservedjotritelNessuna valutazione finora

- Research Paper Economic CrisisDocumento5 pagineResearch Paper Economic Crisisafmcqeqeq100% (1)

- Introduction 201Documento5 pagineIntroduction 201Flaviub23Nessuna valutazione finora

- The Global Financial Crisis - Causes and Solutions.Documento5 pagineThe Global Financial Crisis - Causes and Solutions.Sherlene GarciaNessuna valutazione finora

- Group 135 GreeceDocumento18 pagineGroup 135 GreeceRobert TanaseNessuna valutazione finora

- 002 PDFDocumento42 pagine002 PDFumang24Nessuna valutazione finora

- Financial Market and EconomyDocumento12 pagineFinancial Market and EconomyPraise Cabalum BuenaflorNessuna valutazione finora

- Financial Liberalization and Investments in Nigeria - A Firm Level AnalysisDocumento248 pagineFinancial Liberalization and Investments in Nigeria - A Firm Level Analysischukwu solomonNessuna valutazione finora

- Finance and GrowthDocumento8 pagineFinance and GrowthHabib UllahNessuna valutazione finora

- Hamilton Jenkinson PenalverDocumento25 pagineHamilton Jenkinson Penalverashu9026Nessuna valutazione finora

- All Real and FinancialDocumento16 pagineAll Real and FinancialOgwoGPNessuna valutazione finora

- Accounting Forum: Prem SikkaDocumento18 pagineAccounting Forum: Prem SikkaHendra PoltakNessuna valutazione finora

- Groupwork Assignment Submission 3 M7Documento9 pagineGroupwork Assignment Submission 3 M7Abdullah AbdullahNessuna valutazione finora

- Crisis and 2008 Financial Crisis, Is Considered by Many Economists To Be The WorstDocumento54 pagineCrisis and 2008 Financial Crisis, Is Considered by Many Economists To Be The Worstdineshpatil186Nessuna valutazione finora

- Financialization - What It Is - Why It MattersDocumento31 pagineFinancialization - What It Is - Why It MattersStefan ErdoglijaNessuna valutazione finora

- Global ImbalancesDocumento16 pagineGlobal ImbalancesmetaregardNessuna valutazione finora

- Credit and Growth-Reconsidering Italian Indutrial Policy During The Golden AgeDocumento21 pagineCredit and Growth-Reconsidering Italian Indutrial Policy During The Golden AgeliartofficialNessuna valutazione finora

- New Financial Products and Their Impacts On The Asian Financial Markets Executive SummaryDocumento6 pagineNew Financial Products and Their Impacts On The Asian Financial Markets Executive Summarylalit2roamNessuna valutazione finora

- Bulletin Mar 30Documento15 pagineBulletin Mar 30Finanzas y ComercioNessuna valutazione finora

- Securitization, Shadow Banking, and FinancializationDocumento54 pagineSecuritization, Shadow Banking, and FinancializationjoebloggsscribdNessuna valutazione finora

- Research On Money and Finance: Discussion Paper No 16Documento34 pagineResearch On Money and Finance: Discussion Paper No 16Brian O O'SNessuna valutazione finora

- 1456892183BSE P5 M34 E-Text PDFDocumento9 pagine1456892183BSE P5 M34 E-Text PDFsahil sharmaNessuna valutazione finora

- Treasury Department Financial Regulatory Reform Blueprint 2008Documento212 pagineTreasury Department Financial Regulatory Reform Blueprint 2008joebloggsscribdNessuna valutazione finora

- Financialisation and The New Capitalism?: Giuseppe Fontana, Christos Pitelis and Jochen RundeDocumento6 pagineFinancialisation and The New Capitalism?: Giuseppe Fontana, Christos Pitelis and Jochen RundeeconstudentNessuna valutazione finora

- SpasDocumento7 pagineSpasmilosarNessuna valutazione finora

- The International Monetary and Financial Environment Learning ObjectivesDocumento4 pagineThe International Monetary and Financial Environment Learning ObjectivesAna KatulićNessuna valutazione finora

- Corbo and FischerDocumento105 pagineCorbo and FischerSumit ShekharNessuna valutazione finora

- Article: Southeast Asian Stock Market Linkages: Evidence From Pre-And Post-October 1997Documento7 pagineArticle: Southeast Asian Stock Market Linkages: Evidence From Pre-And Post-October 1997Rocking RidzNessuna valutazione finora

- Ma2451 Engineering Economics and Cost AnalysisDocumento5 pagineMa2451 Engineering Economics and Cost AnalysisRamaswamy SubbiahNessuna valutazione finora

- Case Study AssignmentDocumento7 pagineCase Study AssignmentAyu DitaNessuna valutazione finora

- TOS IA SchemeDocumento4 pagineTOS IA SchemePradeep BiradarNessuna valutazione finora

- Case Hardhat - Rashik, PoorviDocumento6 pagineCase Hardhat - Rashik, PoorviRashik Gupta100% (1)

- Rochmah Sucita Anggraini: Personal ProfileDocumento1 paginaRochmah Sucita Anggraini: Personal ProfileTia Yustika EnchancersNessuna valutazione finora

- CompetitionDocumento4 pagineCompetitionDianaLaura acNessuna valutazione finora

- Comparing Merchandising and Manufakturing CompanyDocumento3 pagineComparing Merchandising and Manufakturing CompanyHermanNessuna valutazione finora

- Amazon PPC ManagementDocumento14 pagineAmazon PPC ManagementDavid Peter100% (1)

- Uniqlo: SWOT AnalysisDocumento3 pagineUniqlo: SWOT AnalysisOpa Evilsiam0% (1)

- Price Effect: Dr. Aruna Kumar Dash IBS HyderabadDocumento16 paginePrice Effect: Dr. Aruna Kumar Dash IBS HyderabadNidhi SinghNessuna valutazione finora

- Dicidend Policy in NepalDocumento42 pagineDicidend Policy in NepalMadhurendra Singh88% (8)

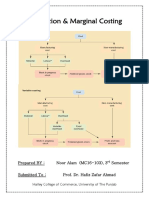

- Absorption & Marginal Costing - Noor Alam (MC16-103)Documento24 pagineAbsorption & Marginal Costing - Noor Alam (MC16-103)Ahmed Ali Khan100% (2)

- Finance 1 Case Study Sample 2013Documento7 pagineFinance 1 Case Study Sample 2013giorgiaNessuna valutazione finora

- Midterm Exam in Aacp - PupDocumento10 pagineMidterm Exam in Aacp - PupmahilomferNessuna valutazione finora

- Instant Download Ebook PDF Fundamental Accounting Principles Volume 1 16th Canadian Edition PDF ScribdDocumento42 pagineInstant Download Ebook PDF Fundamental Accounting Principles Volume 1 16th Canadian Edition PDF Scribdjudi.hawkins744100% (40)

- Notes of MGL EconomicsDocumento45 pagineNotes of MGL Economicsmohanraokp2279100% (1)

- MELI MercadoLibre Inc (Stock Report)Documento24 pagineMELI MercadoLibre Inc (Stock Report)nieuwe68Nessuna valutazione finora

- Continental Tire Success Story SCLDocumento2 pagineContinental Tire Success Story SCLBhanu NimraniNessuna valutazione finora

- (Bank of America) Understanding Mortgage Dollar RollsDocumento18 pagine(Bank of America) Understanding Mortgage Dollar RollsJay Kab100% (2)

- ABC and VariancesDocumento4 pagineABC and VariancesJosehbNessuna valutazione finora

- Restaurant Social Media Marketing Proposal TemplateDocumento1 paginaRestaurant Social Media Marketing Proposal Templatereventhk465Nessuna valutazione finora

- MKT 233 - Mother MurphysDocumento12 pagineMKT 233 - Mother Murphysapi-302016339Nessuna valutazione finora

- Test Questions Chapter 11 DRS IBEO 12Documento20 pagineTest Questions Chapter 11 DRS IBEO 12mrscrouge100% (2)

- MA, CH 05Documento16 pagineMA, CH 05Nahom AberaNessuna valutazione finora

- Reading 37 - Measures of LeverageDocumento2 pagineReading 37 - Measures of LeverageRach3chNessuna valutazione finora

- Corporate Finance 10th Edition Ross Test Bank 1Documento70 pagineCorporate Finance 10th Edition Ross Test Bank 1james100% (39)

- Midterm convertedMEEDocumento6 pagineMidterm convertedMEEMozaan MouzzaNessuna valutazione finora

- Cereal Partners WorldwideDocumento13 pagineCereal Partners WorldwideBeamlakNessuna valutazione finora

- First Interview SummaryDocumento2 pagineFirst Interview Summaryapi-537611054Nessuna valutazione finora

- Continental Mini CaseDocumento8 pagineContinental Mini CaseZane BarryNessuna valutazione finora

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorDa EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorValutazione: 4.5 su 5 stelle4.5/5 (132)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingDa EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingValutazione: 4.5 su 5 stelle4.5/5 (97)

- Business Law: a QuickStudy Digital Reference GuideDa EverandBusiness Law: a QuickStudy Digital Reference GuideNessuna valutazione finora

- The SHRM Essential Guide to Employment Law, Second Edition: A Handbook for HR Professionals, Managers, Businesses, and OrganizationsDa EverandThe SHRM Essential Guide to Employment Law, Second Edition: A Handbook for HR Professionals, Managers, Businesses, and OrganizationsNessuna valutazione finora

- Ben & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooDa EverandBen & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooValutazione: 5 su 5 stelle5/5 (2)

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsDa EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsValutazione: 5 su 5 stelle5/5 (24)

- Introduction to Negotiable Instruments: As per Indian LawsDa EverandIntroduction to Negotiable Instruments: As per Indian LawsValutazione: 5 su 5 stelle5/5 (1)

- Public Finance: Legal Aspects: Collective monographDa EverandPublic Finance: Legal Aspects: Collective monographNessuna valutazione finora

- AI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersDa EverandAI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersNessuna valutazione finora

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorDa EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorValutazione: 4.5 su 5 stelle4.5/5 (63)

- International Business Law: Cases and MaterialsDa EverandInternational Business Law: Cases and MaterialsValutazione: 5 su 5 stelle5/5 (1)

- LLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessDa EverandLLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessValutazione: 5 su 5 stelle5/5 (1)

- Contract Law in America: A Social and Economic Case StudyDa EverandContract Law in America: A Social and Economic Case StudyNessuna valutazione finora

- A Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsDa EverandA Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsNessuna valutazione finora

- The Streetwise Guide to Going Broke without Losing your ShirtDa EverandThe Streetwise Guide to Going Broke without Losing your ShirtNessuna valutazione finora

- Side Hustles for Dummies: The Key to Unlocking Extra Income and Entrepreneurial Success through Side HustlesDa EverandSide Hustles for Dummies: The Key to Unlocking Extra Income and Entrepreneurial Success through Side HustlesNessuna valutazione finora

- How to Win a Merchant Dispute or Fraudulent Chargeback CaseDa EverandHow to Win a Merchant Dispute or Fraudulent Chargeback CaseNessuna valutazione finora

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistDa EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistValutazione: 4 su 5 stelle4/5 (34)

- The Financial Planning Puzzle: Fitting Your Pieces Together to Create Financial FreedomDa EverandThe Financial Planning Puzzle: Fitting Your Pieces Together to Create Financial FreedomValutazione: 4.5 su 5 stelle4.5/5 (2)

- Indian Polity with Indian Constitution & Parliamentary AffairsDa EverandIndian Polity with Indian Constitution & Parliamentary AffairsNessuna valutazione finora

- Secrecy World: Inside the Panama Papers Investigation of Illicit Money Networks and the Global EliteDa EverandSecrecy World: Inside the Panama Papers Investigation of Illicit Money Networks and the Global EliteValutazione: 4.5 su 5 stelle4.5/5 (6)

- The Startup Visa: U.S. Immigration Visa Guide for Startups and FoundersDa EverandThe Startup Visa: U.S. Immigration Visa Guide for Startups and FoundersNessuna valutazione finora

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementDa EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementValutazione: 4.5 su 5 stelle4.5/5 (20)