Potrebbero piacerti anche

- Deegan5e SM Ch32Documento15 pagineDeegan5e SM Ch32Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch37Documento17 pagineDeegan5e SM Ch37Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch34Documento6 pagineDeegan5e SM Ch34Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch35Documento31 pagineDeegan5e SM Ch35Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch33Documento15 pagineDeegan5e SM Ch33Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch36Documento5 pagineDeegan5e SM Ch36Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch25Documento11 pagineDeegan5e SM Ch25Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch29Documento20 pagineDeegan5e SM Ch29Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch31Documento24 pagineDeegan5e SM Ch31Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch27Documento16 pagineDeegan5e SM Ch27Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch28Documento20 pagineDeegan5e SM Ch28Rachel Tanner100% (2)

- Deegan5e SM Ch13Documento9 pagineDeegan5e SM Ch13Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch30Documento27 pagineDeegan5e SM Ch30Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch26Documento8 pagineDeegan5e SM Ch26Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch16Documento13 pagineDeegan5e SM Ch16Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch23Documento13 pagineDeegan5e SM Ch23Rachel Tanner100% (1)

- Deegan5e SM Ch24Documento6 pagineDeegan5e SM Ch24Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch18Documento12 pagineDeegan5e SM Ch18Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch19Documento12 pagineDeegan5e SM Ch19Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch20Documento23 pagineDeegan5e SM Ch20Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch15Documento19 pagineDeegan5e SM Ch15Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch14Documento10 pagineDeegan5e SM Ch14Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch17Documento9 pagineDeegan5e SM Ch17Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch21Documento15 pagineDeegan5e SM Ch21Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch12Documento3 pagineDeegan5e SM Ch12Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch11Documento22 pagineDeegan5e SM Ch11Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch10Documento13 pagineDeegan5e SM Ch10Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch08Documento18 pagineDeegan5e SM Ch08Rachel TannerNessuna valutazione finora

- Deegan5e SM Ch09Documento7 pagineDeegan5e SM Ch09Rachel TannerNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (120)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Internal Sales Representative As of SAP ERP EhP5 (New)Documento32 pagineInternal Sales Representative As of SAP ERP EhP5 (New)Khalid SayeedNessuna valutazione finora

- Defining Social InnovationDocumento15 pagineDefining Social InnovationFasyaAfifNessuna valutazione finora

- 1st Mid Term Exam Fall 2014 AuditingDocumento6 pagine1st Mid Term Exam Fall 2014 AuditingSarahZeidat100% (1)

- Indian Law Solved Case StudiesDocumento14 pagineIndian Law Solved Case StudiesJay PatelNessuna valutazione finora

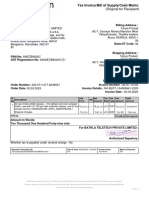

- InvoiceDocumento1 paginaInvoicetanya.prasadNessuna valutazione finora

- A Study On Consumer Behavior Regarding Investment On Financial Instruments at Karvy Stock Broking LTDDocumento88 pagineA Study On Consumer Behavior Regarding Investment On Financial Instruments at Karvy Stock Broking LTDBimal Kumar Dash100% (1)

- Governance, Risk and Dataveillance in The War On TerrorDocumento25 pagineGovernance, Risk and Dataveillance in The War On Terroreliasox123Nessuna valutazione finora

- Permission To MortgageDocumento14 paginePermission To MortgageAabad BrandNessuna valutazione finora

- Keeney v. Larkin, 4th Cir. (2004)Documento4 pagineKeeney v. Larkin, 4th Cir. (2004)Scribd Government DocsNessuna valutazione finora

- Online Shopping and Its ImpactDocumento33 pagineOnline Shopping and Its ImpactAkhil MohananNessuna valutazione finora

- World Airports Freighters: FreighDocumento16 pagineWorld Airports Freighters: FreighBobbie KhunthongchanNessuna valutazione finora

- 4b18 PDFDocumento5 pagine4b18 PDFAnonymous lN5DHnehwNessuna valutazione finora

- Entry Modes AnalysisDocumento24 pagineEntry Modes AnalysisShona JainNessuna valutazione finora

- Royal Laundry ServicesDocumento34 pagineRoyal Laundry ServicesRian Atienza EclarNessuna valutazione finora

- Letter of Intent To Buy: Insert Company Letter HeadDocumento3 pagineLetter of Intent To Buy: Insert Company Letter HeadVelasco JerwenNessuna valutazione finora

- TCI Letter To Safran Chairman 2017-02-14Documento4 pagineTCI Letter To Safran Chairman 2017-02-14marketfolly.comNessuna valutazione finora

- Kabushi Kaisha Isetan Vs IacDocumento2 pagineKabushi Kaisha Isetan Vs IacJudee Anne100% (2)

- The Need For Time Management Training Is Universal: Evidence From TurkeyDocumento8 pagineThe Need For Time Management Training Is Universal: Evidence From TurkeyAnil AkhterNessuna valutazione finora

- Freehold and LeaseholdDocumento3 pagineFreehold and LeaseholdDayah AyoebNessuna valutazione finora

- Nestle CSRDocumento309 pagineNestle CSRMaha AbbasiNessuna valutazione finora

- Caf 6 PT EsDocumento58 pagineCaf 6 PT EsSyeda ItratNessuna valutazione finora

- Example of RFP For Credit ScoringDocumento4 pagineExample of RFP For Credit ScoringadaquilaNessuna valutazione finora

- Preface and AcknowlegementDocumento5 paginePreface and Acknowlegementpraisy christianNessuna valutazione finora

- Chapter 1 Global ServiceDocumento23 pagineChapter 1 Global ServiceRandeep SinghNessuna valutazione finora

- Mission Statement: SBI Articulates Nine Core ValuesDocumento6 pagineMission Statement: SBI Articulates Nine Core ValuesPaneer MomosNessuna valutazione finora

- CR 2015Documento13 pagineCR 2015Agr AcabdiaNessuna valutazione finora

- Start A New Challenge - FXIFYDocumento1 paginaStart A New Challenge - FXIFYSähïl GäjëräNessuna valutazione finora

- Tender Document Heliport ShimlaDocumento128 pagineTender Document Heliport ShimlaAdarsh Kumar ManwalNessuna valutazione finora

- River Eye Fashion CompanyDocumento11 pagineRiver Eye Fashion Companyriver eyeNessuna valutazione finora

- Paying Quantities Key & Charest - CLE - Oil and Gas Disputes 2019Documento22 paginePaying Quantities Key & Charest - CLE - Oil and Gas Disputes 2019Daniel CharestNessuna valutazione finora