Potrebbero piacerti anche

- Corporate Financial Analysis with Microsoft ExcelDa EverandCorporate Financial Analysis with Microsoft ExcelValutazione: 5 su 5 stelle5/5 (1)

- Capital Structure PDFDocumento3 pagineCapital Structure PDFnikitaNessuna valutazione finora

- Receivable Management KanchanDocumento12 pagineReceivable Management KanchanSanchita NaikNessuna valutazione finora

- Cost of Capital: Concept, Components, Importance, Example, Formula and SignificanceDocumento72 pagineCost of Capital: Concept, Components, Importance, Example, Formula and SignificanceRamya GowdaNessuna valutazione finora

- Numericals On Cost of Capital and Capital StructureDocumento2 pagineNumericals On Cost of Capital and Capital StructurePatrick AnthonyNessuna valutazione finora

- Problems On Cash Management Baumol ModelsDocumento1 paginaProblems On Cash Management Baumol ModelsDeepak100% (1)

- New Venture Finance Startup Funding For Entrepreneurs PDFDocumento26 pagineNew Venture Finance Startup Funding For Entrepreneurs PDFBhagavan BangaloreNessuna valutazione finora

- Financial Management 2: UCP-001BDocumento3 pagineFinancial Management 2: UCP-001BRobert RamirezNessuna valutazione finora

- FM - Dividend Policy and Dividend Decision Models (Cir 18.3.2020)Documento129 pagineFM - Dividend Policy and Dividend Decision Models (Cir 18.3.2020)Rohit PanpatilNessuna valutazione finora

- Working Capital MGTDocumento14 pagineWorking Capital MGTrupaliNessuna valutazione finora

- Financial Evaluation of LEASINGDocumento7 pagineFinancial Evaluation of LEASINGmba departmentNessuna valutazione finora

- Notes Toredemption of Preference SharesDocumento40 pagineNotes Toredemption of Preference Sharesaparna bingiNessuna valutazione finora

- SFM - Forex - QuestionsDocumento23 pagineSFM - Forex - QuestionsVishal SutarNessuna valutazione finora

- Dividend Policy - Sample Problems - ICAIDocumento2 pagineDividend Policy - Sample Problems - ICAIgfahsgdahNessuna valutazione finora

- Chapter 4Documento24 pagineChapter 4FăÍż SăįYąðNessuna valutazione finora

- Fa IiiDocumento76 pagineFa Iiirishav agarwalNessuna valutazione finora

- Parte 2 Segundo ParcialDocumento23 pagineParte 2 Segundo ParcialJose Luis Rasilla GonzalezNessuna valutazione finora

- Assignment Cost Sheet SumsDocumento3 pagineAssignment Cost Sheet SumsMamta PrajapatiNessuna valutazione finora

- 5.calculation of EPSDocumento6 pagine5.calculation of EPSVinitgaNessuna valutazione finora

- Banking CompaniesDocumento68 pagineBanking CompaniesKiran100% (2)

- 4 FM AssignmentDocumento3 pagine4 FM AssignmentGorav BhallaNessuna valutazione finora

- 18415compsuggans PCC FM Chapter7Documento13 pagine18415compsuggans PCC FM Chapter7Mukunthan RBNessuna valutazione finora

- FM - 30 MCQDocumento8 pagineFM - 30 MCQsiva sankarNessuna valutazione finora

- Animal HealthDocumento3 pagineAnimal Healthkritigupta.may1999Nessuna valutazione finora

- 4 - Estimating The Hurdle RateDocumento61 pagine4 - Estimating The Hurdle RateDharmesh Goyal100% (1)

- Capital Rationing: Reporter: Celestial C. AndradaDocumento13 pagineCapital Rationing: Reporter: Celestial C. AndradaCelestial Manikan Cangayda-AndradaNessuna valutazione finora

- SFM May 2015Documento25 pagineSFM May 2015Prasanna SharmaNessuna valutazione finora

- Under CapitalizationDocumento10 pagineUnder CapitalizationNMRaycNessuna valutazione finora

- Chapter 10 - Dividend PolicyDocumento37 pagineChapter 10 - Dividend PolicyShubhra Srivastava100% (1)

- Several Discussion Meetings Have Provided The Following Information About OneDocumento1 paginaSeveral Discussion Meetings Have Provided The Following Information About OneMuhammad Shahid100% (1)

- Abubaker Muhammad Haroon 55127Documento4 pagineAbubaker Muhammad Haroon 55127Abubaker NathaniNessuna valutazione finora

- Topic 8 - AS 20Documento10 pagineTopic 8 - AS 20love chawlaNessuna valutazione finora

- CASE STUDY Trends in International BankingDocumento9 pagineCASE STUDY Trends in International BankingbilalbalushiNessuna valutazione finora

- Finance Chapter No 2Documento20 pagineFinance Chapter No 2UzairNessuna valutazione finora

- Balance Sheet Presentation of Liabilities: Problem 10.2ADocumento4 pagineBalance Sheet Presentation of Liabilities: Problem 10.2AMuhammad Haris100% (1)

- Fundamental of FinanceDocumento195 pagineFundamental of FinanceMillad MusaniNessuna valutazione finora

- Factors Affecting Cost of CapitalDocumento40 pagineFactors Affecting Cost of CapitalKartik AroraNessuna valutazione finora

- Practice Question Paper - Financial AccountingDocumento6 paginePractice Question Paper - Financial AccountingNaomi SaldanhaNessuna valutazione finora

- 46793bosinter p8 Seca cp5 PDFDocumento42 pagine46793bosinter p8 Seca cp5 PDFIsavic AlsinaNessuna valutazione finora

- CFP - Module 1 - IIFP - StudentsDocumento269 pagineCFP - Module 1 - IIFP - StudentsmodisahebNessuna valutazione finora

- Tutorial 1 Bond ValuationDocumento2 pagineTutorial 1 Bond Valuationtai kianhongNessuna valutazione finora

- Assignment 8 AnswersDocumento6 pagineAssignment 8 AnswersMyaNessuna valutazione finora

- FFM Updated AnswersDocumento79 pagineFFM Updated AnswersSrikrishnan SNessuna valutazione finora

- PPT of NBFC SDocumento31 paginePPT of NBFC SsagarkharpatilNessuna valutazione finora

- 1164914469ls 1Documento112 pagine1164914469ls 1krishnan bhuvaneswariNessuna valutazione finora

- Fund Flow StatementDocumento7 pagineFund Flow StatementvipulNessuna valutazione finora

- Time Value of Money QuestionDocumento1 paginaTime Value of Money Questionਨਿਖਿਲ ਬਹਿਲ100% (1)

- Problem Solving 16Documento11 pagineProblem Solving 16Ehab M. Abdel HadyNessuna valutazione finora

- FINMATHS Assignment2Documento15 pagineFINMATHS Assignment2Wei Wen100% (1)

- Dividend Policy Gorden, Walter & MM Model Practice QuestionsDocumento1 paginaDividend Policy Gorden, Walter & MM Model Practice QuestionsAmjad AliNessuna valutazione finora

- Consignment Accounting FA - II 1643714291Documento43 pagineConsignment Accounting FA - II 1643714291SWAPNA IS FUNNYNessuna valutazione finora

- Homework Chapter 18 and 19Documento7 pagineHomework Chapter 18 and 19doejohn150Nessuna valutazione finora

- Cost of Capital Lecture Slides in PDF FormatDocumento18 pagineCost of Capital Lecture Slides in PDF FormatLucy UnNessuna valutazione finora

- Ebit Eps AnalysisDocumento4 pagineEbit Eps Analysispranajaya2010Nessuna valutazione finora

- ExerciseDocumento1 paginaExerciseflorentinaNessuna valutazione finora

- Interest Under Debt Alternative $50 (Million) × 10% $5 (Million) EPS (Debt Financing) EPS (Equity Financing)Documento6 pagineInterest Under Debt Alternative $50 (Million) × 10% $5 (Million) EPS (Debt Financing) EPS (Equity Financing)Sthephany GranadosNessuna valutazione finora

- MAN 321 Corporate Finance Final Examination: Fall 2001Documento8 pagineMAN 321 Corporate Finance Final Examination: Fall 2001Suzette Faith LandinginNessuna valutazione finora

- EBIT-eps AnalysisDocumento6 pagineEBIT-eps AnalysisMeghna Badkul JainNessuna valutazione finora

- Capital StructureDocumento9 pagineCapital StructureShrinivasan IyengarNessuna valutazione finora

- Continental CarriersDocumento8 pagineContinental CarriersYaser Al-Torairi100% (3)

- SFPC Operational Definition InstructionsDocumento2 pagineSFPC Operational Definition InstructionsJann KerkyNessuna valutazione finora

- KFC CaseDocumento2 pagineKFC CaseJann KerkyNessuna valutazione finora

- Food Safety and Hygiene LayoutDocumento9 pagineFood Safety and Hygiene LayoutJann Kerky100% (1)

- Precision Delivery Inc. Case StudyDocumento2 paginePrecision Delivery Inc. Case StudyJann Kerky0% (1)

- Cash BudgetDocumento3 pagineCash BudgetJann Kerky0% (1)

- Horizontal and Vertical Analysis DetailsDocumento9 pagineHorizontal and Vertical Analysis DetailsJann KerkyNessuna valutazione finora

- Unsecured ST FinancingDocumento5 pagineUnsecured ST FinancingJann KerkyNessuna valutazione finora

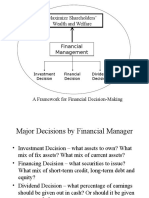

- Maximize Shareholders' Wealth and Welfare: Investment Decision Financial Decision Dividend DecisionDocumento6 pagineMaximize Shareholders' Wealth and Welfare: Investment Decision Financial Decision Dividend DecisionJann KerkyNessuna valutazione finora

- 10 AxiomsDocumento6 pagine10 AxiomsJann KerkyNessuna valutazione finora

- Telfer - Food As ArtDocumento10 pagineTelfer - Food As ArtJann Kerky100% (1)

- Accord 2013 BrochureDocumento25 pagineAccord 2013 BrochureJann KerkyNessuna valutazione finora

- Energy TransformationDocumento6 pagineEnergy TransformationJann KerkyNessuna valutazione finora

- Sample FinalDocumento9 pagineSample FinalJann KerkyNessuna valutazione finora

- APARICIO Frances Et Al. (Eds.) - Musical Migrations Transnationalism and Cultural Hybridity in Latino AmericaDocumento218 pagineAPARICIO Frances Et Al. (Eds.) - Musical Migrations Transnationalism and Cultural Hybridity in Latino AmericaManuel Suzarte MarinNessuna valutazione finora

- Exercise On Relative ClausesDocumento5 pagineExercise On Relative ClausesSAmuel QuinteroNessuna valutazione finora

- Rules and IBA Suggestions On Disciplinary ProceedingsDocumento16 pagineRules and IBA Suggestions On Disciplinary Proceedingshimadri_bhattacharje100% (1)

- Business Enterprise Simulation Quarter 3 - Module 2 - Lesson 1: Analyzing The MarketDocumento13 pagineBusiness Enterprise Simulation Quarter 3 - Module 2 - Lesson 1: Analyzing The MarketJtm GarciaNessuna valutazione finora

- 2009FallCatalog PDFDocumento57 pagine2009FallCatalog PDFMarta LugarovNessuna valutazione finora

- Thai Reader Project Volume 2Documento215 pagineThai Reader Project Volume 2geoffroNessuna valutazione finora

- Persona Core Poster - Creative Companion1 PDFDocumento1 paginaPersona Core Poster - Creative Companion1 PDFAdemola OgunlaluNessuna valutazione finora

- Crim Pro Exam Sheet at A Glance.Documento5 pagineCrim Pro Exam Sheet at A Glance.Heather Kinsaul Foster80% (5)

- Virtue EpistemologyDocumento32 pagineVirtue EpistemologyJorge Torres50% (2)

- Far 1 - Activity 1 - Sept. 09, 2020 - Answer SheetDocumento4 pagineFar 1 - Activity 1 - Sept. 09, 2020 - Answer SheetAnonn100% (1)

- 479f3df10a8c0mathsproject QuadrilateralsDocumento18 pagine479f3df10a8c0mathsproject QuadrilateralsAnand PrakashNessuna valutazione finora

- CH 13 ArqDocumento6 pagineCH 13 Arqneha.senthilaNessuna valutazione finora

- ART 6 LEARNING PACKET Week2-3Documento10 pagineART 6 LEARNING PACKET Week2-3Eljohn CabantacNessuna valutazione finora

- Compare and Contrast Two Cultures Celebrate Between Bali and JavaDocumento1 paginaCompare and Contrast Two Cultures Celebrate Between Bali and JavaqonitazmiNessuna valutazione finora

- English Literature in The 20th CenturyDocumento2 pagineEnglish Literature in The 20th CenturyNguyễn Trung ViệtNessuna valutazione finora

- Avatar Legends The Roleplaying Game 1 12Documento12 pagineAvatar Legends The Roleplaying Game 1 12azeaze0% (1)

- Pavnissh K Sharma 9090101066 Ahmedabad, GujratDocumento51 paginePavnissh K Sharma 9090101066 Ahmedabad, GujratPavnesh SharmaaNessuna valutazione finora

- How To Write An Argumented EssayDocumento35 pagineHow To Write An Argumented EssayFarhad UllahNessuna valutazione finora

- Human Resource Planning in Health CareDocumento3 pagineHuman Resource Planning in Health CarevishalbdsNessuna valutazione finora

- Asher - Bacteria, Inc.Documento48 pagineAsher - Bacteria, Inc.Iyemhetep100% (1)

- Boxnhl MBS (Design-D) Check SheetDocumento13 pagineBoxnhl MBS (Design-D) Check SheetKumari SanayaNessuna valutazione finora

- FR-A800 Plus For Roll To RollDocumento40 pagineFR-A800 Plus For Roll To RollCORTOCIRCUITANTENessuna valutazione finora

- ECON2100 CO Abdool W21Documento5 pagineECON2100 CO Abdool W21Imran AbdoolNessuna valutazione finora

- Potato Lab ReportDocumento10 paginePotato Lab ReportsimplylailaNessuna valutazione finora

- Nurse Implemented Goal Directed Strategy To.97972Documento7 pagineNurse Implemented Goal Directed Strategy To.97972haslinaNessuna valutazione finora

- Network Firewall SecurityDocumento133 pagineNetwork Firewall Securitysagar323Nessuna valutazione finora

- Neurolinguistic ProgrammingDocumento9 pagineNeurolinguistic ProgrammingMartin MontecinoNessuna valutazione finora

- NHÓM ĐỘNG TỪ BẤT QUY TẮCDocumento4 pagineNHÓM ĐỘNG TỪ BẤT QUY TẮCNhựt HàoNessuna valutazione finora

- Unit 5 - Simulation of HVDC SystemDocumento24 pagineUnit 5 - Simulation of HVDC Systemkarthik60% (10)

- 001 Ipack My School BagDocumento38 pagine001 Ipack My School BagBrock JohnsonNessuna valutazione finora