Potrebbero piacerti anche

- Documentary Stamp TaxDocumento120 pagineDocumentary Stamp Taxnegotiator50% (2)

- Business Plan Sample Cleaning ServiceDocumento29 pagineBusiness Plan Sample Cleaning ServiceCarlos Silva100% (11)

- Practice Exam 1 - ACC 3365Documento21 paginePractice Exam 1 - ACC 3365Jessica Colin100% (2)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Da EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Valutazione: 5 su 5 stelle5/5 (1)

- Slm-Strategic Financial Management - 0 PDFDocumento137 pagineSlm-Strategic Financial Management - 0 PDFdadapeer h mNessuna valutazione finora

- Review Notes in Corporation Law 2023Documento13 pagineReview Notes in Corporation Law 2023Se'f BenitezNessuna valutazione finora

- Business Plan From DTIDocumento10 pagineBusiness Plan From DTIfregil_64100% (1)

- MCQ of Corporate Finance PDFDocumento11 pagineMCQ of Corporate Finance PDFsinghsanjNessuna valutazione finora

- Corporate Finance MCQDocumento35 pagineCorporate Finance MCQRohan RoyNessuna valutazione finora

- Mca - 204 - FM & CFDocumento28 pagineMca - 204 - FM & CFjaitripathi26Nessuna valutazione finora

- Finance MCQDocumento46 pagineFinance MCQPallavi GNessuna valutazione finora

- FM MCQsDocumento58 pagineFM MCQsPervaiz ShahidNessuna valutazione finora

- FXTM - Model Question PaperDocumento36 pagineFXTM - Model Question PaperRajiv Warrier0% (1)

- CH 3Documento10 pagineCH 3asem shabanNessuna valutazione finora

- Question Bank-MCQ FM&CF (KMBN, KMBA 204)Documento27 pagineQuestion Bank-MCQ FM&CF (KMBN, KMBA 204)Amit ThakurNessuna valutazione finora

- EMBA ResumeBookDocumento221 pagineEMBA ResumeBooknikunjhandaNessuna valutazione finora

- IA 3 MidtermDocumento9 pagineIA 3 MidtermMelanie Samsona100% (1)

- Management Accounting Midterm ExamDocumento9 pagineManagement Accounting Midterm ExamMarjun Segismundo Tugano IIINessuna valutazione finora

- MCQ On FM PDFDocumento28 pagineMCQ On FM PDFharsh snehNessuna valutazione finora

- CHALLENEGE STATUS-Sample Paper Stage 1Documento26 pagineCHALLENEGE STATUS-Sample Paper Stage 1Neelam Jain100% (1)

- Debtor'S Culture, Psychology, Practices and Idiosyncracies Filipino Traditional Practices Related With Credit and CollectionDocumento6 pagineDebtor'S Culture, Psychology, Practices and Idiosyncracies Filipino Traditional Practices Related With Credit and CollectionRoseanne Binayao Lontian100% (1)

- MCQ-Financial AccountingDocumento13 pagineMCQ-Financial AccountingArchana100% (1)

- Working Capital Management Maruti SuzukiDocumento76 pagineWorking Capital Management Maruti SuzukiAbhay Gupta81% (32)

- Marketing Management Full Notes Mba AnirudhDocumento308 pagineMarketing Management Full Notes Mba AnirudhKumaran ThayumanavanNessuna valutazione finora

- Mcqs On AccountspdfDocumento37 pagineMcqs On AccountspdfEkta SharmaNessuna valutazione finora

- Services MarketingDocumento7 pagineServices MarketingKumaran Thayumanavan0% (1)

- FINC512 Assignement QuestionsDocumento37 pagineFINC512 Assignement QuestionsNaina Malhotra0% (1)

- Finance 3Documento10 pagineFinance 3Jesfer Averie ManarangNessuna valutazione finora

- Traditional Financial Analysis: Some ShortcomingsDocumento11 pagineTraditional Financial Analysis: Some ShortcomingsEvan AzizNessuna valutazione finora

- FM Recollected QuestionsDocumento8 pagineFM Recollected Questionsmevrick_guyNessuna valutazione finora

- Last Assignment of PRC-04 September 2023Documento119 pagineLast Assignment of PRC-04 September 2023zahidmubeen270Nessuna valutazione finora

- CAIIB Bank Financial Management - Questions and AnswersDocumento15 pagineCAIIB Bank Financial Management - Questions and Answerssuperman1293Nessuna valutazione finora

- FINC521Documento10 pagineFINC521All rounder NitinNessuna valutazione finora

- O D e V Leverage and Capital StructureDocumento9 pagineO D e V Leverage and Capital StructureYaldiz YaldizNessuna valutazione finora

- Questions Based On F Inancial Managem EntDocumento21 pagineQuestions Based On F Inancial Managem EntHemant kumarNessuna valutazione finora

- PRC-04 (ITA) Last Assignment January 2024-1Documento132 paginePRC-04 (ITA) Last Assignment January 2024-1contact.samamaNessuna valutazione finora

- MCQ (Set-1)Documento1 paginaMCQ (Set-1)gourav bNessuna valutazione finora

- MFC 2nd SEMESTER FM Assignment 1 FMDocumento6 pagineMFC 2nd SEMESTER FM Assignment 1 FMSumayaNessuna valutazione finora

- Financial Management Credit OfficerDocumento11 pagineFinancial Management Credit OfficerMonika ChhatwaniNessuna valutazione finora

- Financial Management - SmuDocumento0 pagineFinancial Management - SmusirajrNessuna valutazione finora

- PRATIMA MBA-1 Mang. Account - 120811Documento36 paginePRATIMA MBA-1 Mang. Account - 120811Mavani snehaNessuna valutazione finora

- Leverage and Capital Structure: Multiple Choice QuestionsDocumento30 pagineLeverage and Capital Structure: Multiple Choice QuestionsRodNessuna valutazione finora

- Practice Midterm1 - ADMS 1500Documento13 paginePractice Midterm1 - ADMS 1500Anita SharmaNessuna valutazione finora

- BC0044 Accounting and Financial ManagementDocumento12 pagineBC0044 Accounting and Financial ManagementSeekEducationNessuna valutazione finora

- CostingDocumento23 pagineCostingApurva ChaudhariNessuna valutazione finora

- Ross12e Chapter06 TBDocumento26 pagineRoss12e Chapter06 TBHải YếnNessuna valutazione finora

- Accounts MCQDocumento41 pagineAccounts MCQHaripriya VNessuna valutazione finora

- 100 QuestionsDocumento17 pagine100 QuestionsNikki Jean HonaNessuna valutazione finora

- TB CH 2Documento7 pagineTB CH 2Jaz AliNessuna valutazione finora

- Acc564 HW 3Documento4 pagineAcc564 HW 3Aaryan PatelNessuna valutazione finora

- MCQ-Chapter 6 and 7-Answer PDFDocumento7 pagineMCQ-Chapter 6 and 7-Answer PDFpiratekingNessuna valutazione finora

- Practice Exam #2Documento12 paginePractice Exam #2Mat MorashNessuna valutazione finora

- Fin202 Full Exams With Answeres 2023-1-137Documento137 pagineFin202 Full Exams With Answeres 2023-1-137Stephen ThukuNessuna valutazione finora

- Unit 2 MCQ Business FinanceDocumento6 pagineUnit 2 MCQ Business FinancePrateek Yadav100% (1)

- Com 3Documento12 pagineCom 3Murad AliNessuna valutazione finora

- FXTM - Model AnswersDocumento17 pagineFXTM - Model AnswersRajiv WarrierNessuna valutazione finora

- Mock Exam-1: Post: Accounts Officer & Jr. Executive Accounts. Circle Correct Answers (1 Mark For Each Correct Answer)Documento8 pagineMock Exam-1: Post: Accounts Officer & Jr. Executive Accounts. Circle Correct Answers (1 Mark For Each Correct Answer)Bilawal GillaniNessuna valutazione finora

- MCQ On FMDocumento32 pagineMCQ On FMShubhada AmaneNessuna valutazione finora

- Caiib FM Mod D MCQDocumento7 pagineCaiib FM Mod D MCQSanjeev GuptaNessuna valutazione finora

- Sample QP 2 Jan2020Documento23 pagineSample QP 2 Jan2020M Rafeeq100% (1)

- ACF End Term 2015Documento8 pagineACF End Term 2015SharmaNessuna valutazione finora

- Accountancy Model Paper 1Documento9 pagineAccountancy Model Paper 1Hashim SethNessuna valutazione finora

- Compilation of FMSM Telegram McqsDocumento17 pagineCompilation of FMSM Telegram McqsAddvit ShrivastavaNessuna valutazione finora

- CF Chap 2Documento29 pagineCF Chap 2Thu Hiền KhươngNessuna valutazione finora

- MULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionDocumento13 pagineMULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionCHAU Nguyen Ngoc BaoNessuna valutazione finora

- Exit Exam Tutorial ClassDocumento58 pagineExit Exam Tutorial Classkedirmahammed8Nessuna valutazione finora

- I Semester MCQDocumento8 pagineI Semester MCQJoshva FranklinNessuna valutazione finora

- Off-Balance Sheet Financing & Financial AnalysisDocumento10 pagineOff-Balance Sheet Financing & Financial AnalysisEvan AzizNessuna valutazione finora

- EE2253 CS 2marks 2013Documento14 pagineEE2253 CS 2marks 2013selvi0412100% (1)

- OB Notes-Unit IDocumento1 paginaOB Notes-Unit IKumaran ThayumanavanNessuna valutazione finora

- Minimum Wages Act, 1948Documento16 pagineMinimum Wages Act, 1948Priya Mittal0% (1)

- Minimum Wages Act 1948Documento20 pagineMinimum Wages Act 1948Kumaran Thayumanavan0% (1)

- Body LanguageDocumento12 pagineBody LanguageJaspal DosanjhNessuna valutazione finora

- BA7207 BusinessResearchMethodsquestionbankDocumento8 pagineBA7207 BusinessResearchMethodsquestionbankKumaran ThayumanavanNessuna valutazione finora

- MB0038 Answer KeysDocumento18 pagineMB0038 Answer KeysRehan QuadriNessuna valutazione finora

- 07MB104 - Organizational Behaviour - OKDocumento27 pagine07MB104 - Organizational Behaviour - OKKumaran Thayumanavan100% (1)

- MB0038 Answer KeysDocumento18 pagineMB0038 Answer KeysRehan QuadriNessuna valutazione finora

- MB0038 Answer KeysDocumento18 pagineMB0038 Answer KeysRehan QuadriNessuna valutazione finora

- Managerial Work-Unit 1 PDFDocumento12 pagineManagerial Work-Unit 1 PDFKumaran ThayumanavanNessuna valutazione finora

- UGC Guidelines-2013-Refer Page 99Documento129 pagineUGC Guidelines-2013-Refer Page 99PavanNessuna valutazione finora

- Corporate Social ResponsibilityDocumento19 pagineCorporate Social ResponsibilityKumaran ThayumanavanNessuna valutazione finora

- Customer Satisfaction and Service Analysis Tvs Motors Project Report MbaDocumento73 pagineCustomer Satisfaction and Service Analysis Tvs Motors Project Report MbaKumaran Thayumanavan67% (3)

- Abjamesola Tailoring Services Case StudyDocumento17 pagineAbjamesola Tailoring Services Case StudyTintin Tao-onNessuna valutazione finora

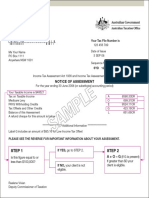

- Step 1 Step 2: Notice of AssessmentDocumento1 paginaStep 1 Step 2: Notice of Assessmentabinash manandharNessuna valutazione finora

- ADVANCED FA Chap IIIDocumento7 pagineADVANCED FA Chap IIIFasiko Asmaro100% (1)

- Startups - Financial PrudenceDocumento12 pagineStartups - Financial PrudenceNeelajit ChandraNessuna valutazione finora

- Mananquil, Julieta P. - Jeths JefrenDocumento12 pagineMananquil, Julieta P. - Jeths JefrenMarissa Bucad GomezNessuna valutazione finora

- Eicher Motors BSDocumento2 pagineEicher Motors BSVaishnav SunilNessuna valutazione finora

- Tally Accounting Book by Ca MD ImranDocumento6 pagineTally Accounting Book by Ca MD ImranMd ImranNessuna valutazione finora

- Riiitzaiit6F5T-L I: R1 Official Form 1) (12/11Documento41 pagineRiiitzaiit6F5T-L I: R1 Official Form 1) (12/11Chapter 11 DocketsNessuna valutazione finora

- ReceiptDocumento3 pagineReceiptAhsan KhanNessuna valutazione finora

- Collateral Document Delivery Request Form v2Documento1 paginaCollateral Document Delivery Request Form v2Teena BarrettoNessuna valutazione finora

- Mid (Zara)Documento4 pagineMid (Zara)hbuzdarNessuna valutazione finora

- Taskforce On Nature Related Financial Disclosures (TNFD) - Summary - NCDocumento5 pagineTaskforce On Nature Related Financial Disclosures (TNFD) - Summary - NCNiraj ChourasiaNessuna valutazione finora

- Quarterly Publication of Individuals, Who Have Chosen To Expatriate, As Required by Section 6039GDocumento17 pagineQuarterly Publication of Individuals, Who Have Chosen To Expatriate, As Required by Section 6039GKelly Phillips ErbNessuna valutazione finora

- Currency FuturesDocumento14 pagineCurrency Futurestelesor13Nessuna valutazione finora

- Taslima - InternshipDocumento22 pagineTaslima - InternshipEasy Learning AcademyNessuna valutazione finora

- The Accounting Cycle: Preparing An Annual Report: Irwin/Mcgraw-HillDocumento36 pagineThe Accounting Cycle: Preparing An Annual Report: Irwin/Mcgraw-HillJumma KhanNessuna valutazione finora

- Bank Reconciliation StatementDocumento39 pagineBank Reconciliation StatementinnovativiesNessuna valutazione finora

- Member Statement: Questions?Documento8 pagineMember Statement: Questions?Michael CarsonNessuna valutazione finora

- Accounting Words IDocumento1 paginaAccounting Words IArnold SilvaNessuna valutazione finora

- SSS' EE and ER DefinitionsDocumento4 pagineSSS' EE and ER Definitionspaula_bagnesNessuna valutazione finora

- FY23 Maximus Investor Presentation - AugDocumento15 pagineFY23 Maximus Investor Presentation - AugMarisa DemarcoNessuna valutazione finora

- Islamic Banking: Financial Institutions and Markets Final ProjectDocumento27 pagineIslamic Banking: Financial Institutions and Markets Final ProjectNaina Azfar GondalNessuna valutazione finora

- Negotiating A Venture Capital Term SheetDocumento2 pagineNegotiating A Venture Capital Term SheetmikeslackenernyNessuna valutazione finora