Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- 10 - Chapter 3Documento54 pagine10 - Chapter 3yibungoNessuna valutazione finora

- 09 - Chapter 2Documento44 pagine09 - Chapter 2yibungoNessuna valutazione finora

- 11 - Chapter 4Documento25 pagine11 - Chapter 4yibungoNessuna valutazione finora

- Lecture 2 Market Prices and Present Value Printout FinalDocumento28 pagineLecture 2 Market Prices and Present Value Printout FinalyibungoNessuna valutazione finora

- Simple Linear Regression: Y XI. XI XDocumento25 pagineSimple Linear Regression: Y XI. XI XyibungoNessuna valutazione finora

- 08 - Chapter 1Documento45 pagine08 - Chapter 1yibungoNessuna valutazione finora

- British Administration of Manipur by Kh. Ibochou Singh MADocumento1 paginaBritish Administration of Manipur by Kh. Ibochou Singh MAyibungoNessuna valutazione finora

- Startup PolicyDocumento1 paginaStartup PolicyyibungoNessuna valutazione finora

- 15.415x Foundations of Modern Finance: Lecture 1: IntroductionDocumento37 pagine15.415x Foundations of Modern Finance: Lecture 1: IntroductionyibungoNessuna valutazione finora

- Actions Required For Building A Strong Startup Ecosystem in ManipurDocumento3 pagineActions Required For Building A Strong Startup Ecosystem in ManipuryibungoNessuna valutazione finora

- 12 Ways To Be More Search SavvyDocumento5 pagine12 Ways To Be More Search SavvyyibungoNessuna valutazione finora

- Propose Evaluation Rubric INITIAL SCREENING For IDEA Stage StartupDocumento2 paginePropose Evaluation Rubric INITIAL SCREENING For IDEA Stage StartupyibungoNessuna valutazione finora

- Canal IrrigationDocumento4 pagineCanal IrrigationyibungoNessuna valutazione finora

- 10 Ethical Issues Confronting IT ManagersDocumento5 pagine10 Ethical Issues Confronting IT ManagersyibungoNessuna valutazione finora

- Engineering: Engineering Is The Application of Science To The OptimumDocumento53 pagineEngineering: Engineering Is The Application of Science To The OptimumyibungoNessuna valutazione finora

- Case Study of EBay IncDocumento3 pagineCase Study of EBay IncyibungoNessuna valutazione finora

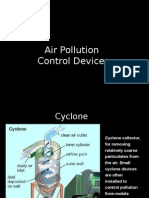

- Air Pollution Control DevicesDocumento16 pagineAir Pollution Control Devicesyibungo0% (1)

- Shear Force and Bending MomentDocumento23 pagineShear Force and Bending Momentyibungo100% (2)

- Bamboo Based CowshedDocumento47 pagineBamboo Based CowshedyibungoNessuna valutazione finora

- Civil EngineeringDocumento27 pagineCivil EngineeringyibungoNessuna valutazione finora

- Non Linear Pushover AnalysisDocumento10 pagineNon Linear Pushover AnalysisyibungoNessuna valutazione finora

- Sample Banking Presentation 0 0Documento12 pagineSample Banking Presentation 0 0Marcos LopezNessuna valutazione finora

- Amoya Mcbean Family and Resource Mangement PortfolioDocumento108 pagineAmoya Mcbean Family and Resource Mangement PortfolioJahiem BenjaminNessuna valutazione finora

- Final MCom Dissertation Lloyd Uta 482059Documento126 pagineFinal MCom Dissertation Lloyd Uta 482059Phi BaiNessuna valutazione finora

- Act3 StatDocumento33 pagineAct3 StatAllecks Juel Luchana0% (1)

- New Product Development WikipediaDocumento9 pagineNew Product Development WikipediaBreylin CastilloNessuna valutazione finora

- Module 5 (Week 7 and 8)Documento11 pagineModule 5 (Week 7 and 8)elma anacletoNessuna valutazione finora

- Queen Mary Dissertation DeadlineDocumento4 pagineQueen Mary Dissertation DeadlinePaySomeoneToDoMyPaperSanDiego100% (1)

- Volkswagens Emission Scandal Case StudyDocumento18 pagineVolkswagens Emission Scandal Case StudyTran Vu Thu TrangNessuna valutazione finora

- MCQs - Chapters 13 - 14Documento10 pagineMCQs - Chapters 13 - 14Anh Thư SparkyuNessuna valutazione finora

- Build BacklinksDocumento17 pagineBuild BacklinksKashif NaeemNessuna valutazione finora

- Inventory ManagementDocumento15 pagineInventory ManagementAnna Lyssa BatasNessuna valutazione finora

- Consort Utilizing Consolidation To Lower Transport CostsDocumento12 pagineConsort Utilizing Consolidation To Lower Transport CostsDenis Mendoza QuispeNessuna valutazione finora

- IPD Export: Indonesia Export Shipment RatesDocumento6 pagineIPD Export: Indonesia Export Shipment RatesVia Anggi TastietranNessuna valutazione finora

- General Principles of Contracts & Transactions in Islamic PDFDocumento19 pagineGeneral Principles of Contracts & Transactions in Islamic PDFMuhammad Ammar100% (1)

- Chapter 10 Audit 1Documento2 pagineChapter 10 Audit 1Ismah ParkNessuna valutazione finora

- Caterpillar Sqep Procedures: May 3, 2017 SQEP Process OwnerDocumento33 pagineCaterpillar Sqep Procedures: May 3, 2017 SQEP Process OwnerDurai NaiduNessuna valutazione finora

- A Economics Gr. 12 Monopoly PresentationDocumento22 pagineA Economics Gr. 12 Monopoly PresentationHari prakarsh NimiNessuna valutazione finora

- Module Title: Identifying Suitability For Micro Business TTLM Code: EIS CWS2 M07 TTLM 0919v1 This Module Includes The Following Learning GuidesDocumento53 pagineModule Title: Identifying Suitability For Micro Business TTLM Code: EIS CWS2 M07 TTLM 0919v1 This Module Includes The Following Learning GuidesUm ShagizNessuna valutazione finora

- 31 (2) Sbi and IciciDocumento6 pagine31 (2) Sbi and IciciShyla PascalNessuna valutazione finora

- Pizza Hutt Accepting Maximum M Orders. Orders Are ...Documento2 paginePizza Hutt Accepting Maximum M Orders. Orders Are ...Mohammad Jahangir AmeenNessuna valutazione finora

- Chapter 11Documento13 pagineChapter 11Zhairra Mae ElaironNessuna valutazione finora

- Shabbir AhmadDocumento2 pagineShabbir AhmadEkhlas AmmariNessuna valutazione finora

- Becoming A Leader PDFDocumento1 paginaBecoming A Leader PDFCrestian Nebreja Morta44% (16)

- (TOEIC650) Exam Practice 1 (16 Bản)Documento10 pagine(TOEIC650) Exam Practice 1 (16 Bản)Hải YếnNessuna valutazione finora

- Standard Costing Practice Questions FinalDocumento5 pagineStandard Costing Practice Questions FinalShehrozSTNessuna valutazione finora

- Intercompany-Profit Transaction: Plant AssetDocumento29 pagineIntercompany-Profit Transaction: Plant AssetCici SintamayaNessuna valutazione finora

- Audit of Intangibles - AudProb SolutionDocumento13 pagineAudit of Intangibles - AudProb SolutionPaula De RuedaNessuna valutazione finora

- CS2023 SunnyDocumento2 pagineCS2023 Sunnyrohit. remooNessuna valutazione finora

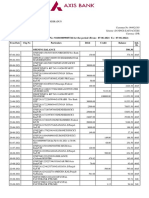

- Statement of Axis Account No:921010009005726 For The Period (From: 07-06-2021 To: 07-06-2022)Documento22 pagineStatement of Axis Account No:921010009005726 For The Period (From: 07-06-2021 To: 07-06-2022)TusharNessuna valutazione finora

- Luther Directors Duties and LiabilitiesDocumento43 pagineLuther Directors Duties and LiabilitiesKaung Khant WanaNessuna valutazione finora