Potrebbero piacerti anche

- Kelly's Finance Cheat Sheet V6Documento2 pagineKelly's Finance Cheat Sheet V6Kelly Koh100% (4)

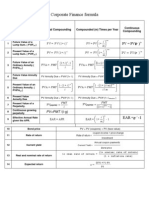

- Corporate Finance Formula SheetDocumento4 pagineCorporate Finance Formula Sheetogsunny100% (3)

- Finance Cheat SheetDocumento4 pagineFinance Cheat SheetRudolf Jansen van RensburgNessuna valutazione finora

- Corporate Finance Math SheetDocumento19 pagineCorporate Finance Math Sheetmweaveruga100% (3)

- Corporate Finance - FormulasDocumento3 pagineCorporate Finance - FormulasAbhijit Pandit100% (1)

- CheatSheet (Finance)Documento1 paginaCheatSheet (Finance)Guan Yu Lim100% (3)

- Corporate Finance FormulasDocumento3 pagineCorporate Finance FormulasMustafa Yavuzcan83% (12)

- CheatDocumento1 paginaCheatIshmo KueedNessuna valutazione finora

- Fnce 100 Final Cheat SheetDocumento2 pagineFnce 100 Final Cheat SheetToby Arriaga100% (2)

- Cheat Sheet Final - FMVDocumento3 pagineCheat Sheet Final - FMVhanifakih100% (2)

- Cheat Sheet Corporate - FinanceDocumento2 pagineCheat Sheet Corporate - FinanceAnna BudaevaNessuna valutazione finora

- Finance Cheat SheetDocumento2 pagineFinance Cheat SheetMarc MNessuna valutazione finora

- Accounting Cheat SheetDocumento7 pagineAccounting Cheat Sheetopty100% (15)

- Bonds Exam Cheat SheetDocumento2 pagineBonds Exam Cheat SheetSergi Iglesias CostaNessuna valutazione finora

- FIN6215-Cheat Sheet BigDocumento3 pagineFIN6215-Cheat Sheet BigJojo Kittiya100% (1)

- CFA Level 1 Corporate Finance - Our Cheat Sheet - 300hoursDocumento14 pagineCFA Level 1 Corporate Finance - Our Cheat Sheet - 300hoursMichNessuna valutazione finora

- Cheat Sheet - AccountingDocumento2 pagineCheat Sheet - AccountingJeffery KaoNessuna valutazione finora

- Cheat Sheet For Financial AccountingDocumento1 paginaCheat Sheet For Financial Accountingmikewu101Nessuna valutazione finora

- Financial Accounting: Tools For Business Decision-Making, Third Canadian EditionDocumento6 pagineFinancial Accounting: Tools For Business Decision-Making, Third Canadian Editionapi-19743565100% (1)

- Corporate FinanceDocumento19 pagineCorporate FinanceBilal Shahid100% (4)

- Fin Cheat SheetDocumento3 pagineFin Cheat SheetChristina RomanoNessuna valutazione finora

- CFA Formula Cheat SheetDocumento9 pagineCFA Formula Cheat SheetChingWa ChanNessuna valutazione finora

- 3 - FCF CalculationDocumento2 pagine3 - FCF CalculationAman ManjiNessuna valutazione finora

- Corporate Finance CheatsheetDocumento4 pagineCorporate Finance CheatsheetLynetteNessuna valutazione finora

- Finance Cheat Sheet - Formulas and Concepts - RM NISPEROSDocumento27 pagineFinance Cheat Sheet - Formulas and Concepts - RM NISPEROSCHANDAN C KAMATHNessuna valutazione finora

- Corporate Finance Cheat SheetDocumento3 pagineCorporate Finance Cheat Sheetdiscreetmike50Nessuna valutazione finora

- BF2201 Cheat Sheet FinalsDocumento2 pagineBF2201 Cheat Sheet Finalssiewhong93100% (1)

- Cfa Level I - Us Gaap Vs IfrsDocumento4 pagineCfa Level I - Us Gaap Vs IfrsSanjay RathiNessuna valutazione finora

- Module 2 Introducting Financial Statements - 6th EditionDocumento7 pagineModule 2 Introducting Financial Statements - 6th EditionjoshNessuna valutazione finora

- Inventory Turnover Cost of Sales / Avg Inventory High Is Effective Inv MGMT Days of Inventory On Hand (DOH) 365/inv TurnoverDocumento3 pagineInventory Turnover Cost of Sales / Avg Inventory High Is Effective Inv MGMT Days of Inventory On Hand (DOH) 365/inv Turnoverjoe91bmwNessuna valutazione finora

- Accounting Cheat SheetsDocumento4 pagineAccounting Cheat SheetsGreg BealNessuna valutazione finora

- Technical Finance Interview Prep (Student)Documento261 pagineTechnical Finance Interview Prep (Student)fernando.torrealbatesiNessuna valutazione finora

- Accounting Cheat SheetDocumento2 pagineAccounting Cheat Sheetanoushes1100% (2)

- Cheat Sheet For AccountingDocumento4 pagineCheat Sheet For AccountingshihuiNessuna valutazione finora

- Corporate Finance OutlineDocumento45 pagineCorporate Finance Outlinemweaveruga100% (5)

- Test Questions and Solutions True-FalseDocumento99 pagineTest Questions and Solutions True-Falsekabirakhan2007100% (1)

- Management Cheat SheetDocumento2 pagineManagement Cheat Sheetnightmonkey215100% (2)

- Corporate Finance - Beny W2011Documento38 pagineCorporate Finance - Beny W2011cparka12Nessuna valutazione finora

- ACCT 101 Cheat SheetDocumento1 paginaACCT 101 Cheat SheetAndrea NingNessuna valutazione finora

- Answers To Problem Sets: How Much Should A Corporation Borrow?Documento8 pagineAnswers To Problem Sets: How Much Should A Corporation Borrow?priyanka GayathriNessuna valutazione finora

- Answers To Problem Sets: How Much Should A Corporation Borrow?Documento10 pagineAnswers To Problem Sets: How Much Should A Corporation Borrow?mandy YiuNessuna valutazione finora

- Brealey - Principles of Corporate Finance - 13e - Chap18 - SMDocumento10 pagineBrealey - Principles of Corporate Finance - 13e - Chap18 - SMShivamNessuna valutazione finora

- Formulas and ConceptsDocumento7 pagineFormulas and Conceptscolen.anneNessuna valutazione finora

- FINA2222 Formula SheetDocumento6 pagineFINA2222 Formula SheetDaksh ParasharNessuna valutazione finora

- Finance NoteDocumento19 pagineFinance NoteHui YiNessuna valutazione finora

- Pln-Cmams - Cost of CapitalDocumento26 paginePln-Cmams - Cost of Capitaldwi suhartantoNessuna valutazione finora

- Manajemen Keuangan RangkumanDocumento6 pagineManajemen Keuangan RangkumanDanty Christina SitalaksmiNessuna valutazione finora

- Chapter 19 Financing and ValuationDocumento8 pagineChapter 19 Financing and ValuationLovely MendozaNessuna valutazione finora

- Exam Cheat Sheet VSJDocumento3 pagineExam Cheat Sheet VSJMinh ANhNessuna valutazione finora

- Finalexam - Financial Management FicheDocumento6 pagineFinalexam - Financial Management FicheLouis BarbierNessuna valutazione finora

- FIN 401 - Cheat SheetDocumento2 pagineFIN 401 - Cheat SheetStephanie NaamaniNessuna valutazione finora

- Formula Sheet FIMDocumento4 pagineFormula Sheet FIMYNessuna valutazione finora

- Formulas Öecture SlidesDocumento2 pagineFormulas Öecture SlidesChristine KwanNessuna valutazione finora

- Topic04 WACCDocumento28 pagineTopic04 WACCGaukhar RyskulovaNessuna valutazione finora

- AFM. Resources. Useful FormulasDocumento4 pagineAFM. Resources. Useful FormulasAnonymous MeNessuna valutazione finora

- Formula Sheet Midterm2021Documento5 pagineFormula Sheet Midterm2021Derin OlenikNessuna valutazione finora

- CPA Review Notes 2019 - BEC (Business Environment Concepts)Da EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Valutazione: 4 su 5 stelle4/5 (9)

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Da EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Valutazione: 3.5 su 5 stelle3.5/5 (17)

- Second Bite at CherryDocumento4 pagineSecond Bite at Cherrysubtle69Nessuna valutazione finora

- Nigerian Islamists Add Schools To Hit ListDocumento1 paginaNigerian Islamists Add Schools To Hit Listsubtle69Nessuna valutazione finora

- Lunch 27.50may Du Jour 3.05.12Documento1 paginaLunch 27.50may Du Jour 3.05.12subtle69Nessuna valutazione finora

- Rhubarb Bellini 8 Olives 3.5, Salumi 8: AntipastiDocumento2 pagineRhubarb Bellini 8 Olives 3.5, Salumi 8: Antipastisubtle69Nessuna valutazione finora

- Menu Du Jour Starters: Zack Saghir, Head Sommelier Recommends The Following WinesDocumento1 paginaMenu Du Jour Starters: Zack Saghir, Head Sommelier Recommends The Following Winessubtle69Nessuna valutazione finora

- Beginners Cycling Training Schedule PDFDocumento1 paginaBeginners Cycling Training Schedule PDFNazRule Az-OneNessuna valutazione finora

- Lunch: For All The GuestsDocumento1 paginaLunch: For All The Guestssubtle69Nessuna valutazione finora

- Sample Lunch MenuDocumento1 paginaSample Lunch Menusubtle69Nessuna valutazione finora

- f4868 2011 Tax File ExtensionDocumento4 paginef4868 2011 Tax File ExtensionBurt BoiceNessuna valutazione finora

- f4868 2011 Tax File ExtensionDocumento4 paginef4868 2011 Tax File ExtensionBurt BoiceNessuna valutazione finora

- Directions To University of London UnionDocumento1 paginaDirections To University of London Unionsubtle69Nessuna valutazione finora

- Instrucciones 1040Documento189 pagineInstrucciones 1040Charlie GmNessuna valutazione finora

- How To Calculate Your Taxable Profits: Helpsheet 222Documento14 pagineHow To Calculate Your Taxable Profits: Helpsheet 222subtle69Nessuna valutazione finora

- f4868 2011 Tax File ExtensionDocumento4 paginef4868 2011 Tax File ExtensionBurt BoiceNessuna valutazione finora

- Self Employed Form - Low EarningsDocumento1 paginaSelf Employed Form - Low EarningsYumi TeflTeacherNessuna valutazione finora

- Social Security Form OnlineDocumento5 pagineSocial Security Form OnlineDiego PinedoNessuna valutazione finora

- Brunch Menu 2012Documento1 paginaBrunch Menu 2012subtle69Nessuna valutazione finora

- Starters Mains: All Items Above Come With A Side of Your ChoiceDocumento1 paginaStarters Mains: All Items Above Come With A Side of Your Choicesubtle69Nessuna valutazione finora

- Past ExamDocumento10 paginePast Examsubtle69Nessuna valutazione finora

- RPFHM 16-Week Intermediate Half Marathon Programme 2011Documento4 pagineRPFHM 16-Week Intermediate Half Marathon Programme 2011roscowooNessuna valutazione finora

- Peritivosy Opas: T & T S G C B P O Q HDocumento1 paginaPeritivosy Opas: T & T S G C B P O Q Hsubtle69Nessuna valutazione finora

- MasterChef CookbookDocumento402 pagineMasterChef CookbookGilberto Liera100% (2)

- RPFHM 16-Week Beginner Half Marathon Programme 2011Documento4 pagineRPFHM 16-Week Beginner Half Marathon Programme 2011subtle69Nessuna valutazione finora

- 1116 - 2012 (Instructions)Documento23 pagine1116 - 2012 (Instructions)subtle69Nessuna valutazione finora

- CRPDocumento164 pagineCRPsubtle69Nessuna valutazione finora

- Course Syllabus (NEW)Documento4 pagineCourse Syllabus (NEW)subtle690% (1)

- Grad Rep QuestionsDocumento1 paginaGrad Rep Questionssubtle69Nessuna valutazione finora

- EMBA 2013 Business Skills 1and2Documento6 pagineEMBA 2013 Business Skills 1and2subtle69Nessuna valutazione finora

- Exhibitor A-Z ManualDocumento6 pagineExhibitor A-Z Manualsubtle69Nessuna valutazione finora

- Standard Tube MapDocumento2 pagineStandard Tube MappastaiNessuna valutazione finora

- Jahn Teller DistortionDocumento7 pagineJahn Teller DistortionBharath Reddy100% (1)

- Prelim5 MCQ PDFDocumento4 paginePrelim5 MCQ PDFanandyadav090Nessuna valutazione finora

- CH05Documento6 pagineCH05Sumeet DesaiNessuna valutazione finora

- FROG Chapter02 PDFDocumento73 pagineFROG Chapter02 PDF신재호Nessuna valutazione finora

- CFA Level 1 Study GuideDocumento40 pagineCFA Level 1 Study GuideTom RomanoNessuna valutazione finora

- Submission 2Documento2 pagineSubmission 2lxNessuna valutazione finora

- ReportDocumento1 paginaReportarun_algoNessuna valutazione finora

- Thesis Impacts of Remedial Rights On Construction Contractors by Solomon MDocumento130 pagineThesis Impacts of Remedial Rights On Construction Contractors by Solomon MMichael McfarlandNessuna valutazione finora

- Chapter 16 SolutionsDocumento10 pagineChapter 16 SolutionsShaoxin LuNessuna valutazione finora

- Diluted Earnings Per Share QDocumento2 pagineDiluted Earnings Per Share Qjano_art210% (4)

- Reaction Mechanisms OverviewDocumento19 pagineReaction Mechanisms OverviewHanhHongDaoNessuna valutazione finora

- Nova Chemical CorporationDocumento28 pagineNova Chemical Corporationrzannat94100% (2)

- Lesson Plan Intermolecular Forces BaruDocumento30 pagineLesson Plan Intermolecular Forces BaruIrvan AdisthaNessuna valutazione finora

- ConvertibleBondStudy (TF and AFV Model)Documento32 pagineConvertibleBondStudy (TF and AFV Model)Zheng GaoNessuna valutazione finora

- Financing PPPs. Project Finance. BBVA PDFDocumento23 pagineFinancing PPPs. Project Finance. BBVA PDFErnesto CanoNessuna valutazione finora

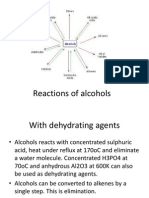

- Reactions of AlcoholsDocumento10 pagineReactions of AlcoholsNeen NaazNessuna valutazione finora

- CatalogDocumento2 pagineCataloglangtu2011Nessuna valutazione finora

- Covalent Bonding v1.0Documento45 pagineCovalent Bonding v1.0jt100% (1)

- Accounting of Share CapitalDocumento102 pagineAccounting of Share Capitalmohanraokp22790% (1)

- Finance Assignment 1Documento9 pagineFinance Assignment 1NikhilBaveja50% (2)

- Form 57ADocumento4 pagineForm 57AMiguel TancangcoNessuna valutazione finora

- S-Block Chemistry: Answers To Worked ExamplesDocumento11 pagineS-Block Chemistry: Answers To Worked ExamplesRabin ShresthaNessuna valutazione finora

- Chemistry Honors Final Review WorksheetDocumento12 pagineChemistry Honors Final Review Worksheetjb12355Nessuna valutazione finora

- Saponification-The Process of Making Soap: What Are Fatty Acids?Documento5 pagineSaponification-The Process of Making Soap: What Are Fatty Acids?Anonymous UoRu4sNessuna valutazione finora

- Alcohols Phenols PDFDocumento88 pagineAlcohols Phenols PDFAnanda VijayasarathyNessuna valutazione finora

- EX1 PracticeDocumento5 pagineEX1 PracticeDiljitSinghNessuna valutazione finora

- 9701 w12 Ms 41Documento11 pagine9701 w12 Ms 41Matthew Vinodh RajNessuna valutazione finora

- Chapter 8 PracticeQDocumento20 pagineChapter 8 PracticeQKevin Peng0% (1)

- SPD HybridizationDocumento9 pagineSPD HybridizationRose Marie VicenteNessuna valutazione finora