Potrebbero piacerti anche

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Na Fianna Tune BookDocumento41 pagineNa Fianna Tune BookDavid LairsonNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Mandel 1965 Thesis On Jish Immign 1882-1914Documento580 pagineMandel 1965 Thesis On Jish Immign 1882-1914Gerald SackNessuna valutazione finora

- Coop Updates 3Documento52 pagineCoop Updates 3nelsonpm81Nessuna valutazione finora

- Ontario G1 TEST PracticeDocumento9 pagineOntario G1 TEST Practicen_fawwaazNessuna valutazione finora

- Lungi Dal Caro Bene by Giuseppe Sarti Sheet Music For Piano, Bass Voice (Piano-Voice)Documento1 paginaLungi Dal Caro Bene by Giuseppe Sarti Sheet Music For Piano, Bass Voice (Piano-Voice)Renée LapointeNessuna valutazione finora

- Office of The City Prosecutor: Counter - AffidavitDocumento6 pagineOffice of The City Prosecutor: Counter - AffidavitApril Elenor JucoNessuna valutazione finora

- What Is Corporate RestructuringDocumento45 pagineWhat Is Corporate RestructuringPuneet GroverNessuna valutazione finora

- RIBA WorkstagesDocumento1 paginaRIBA WorkstagesCong TranNessuna valutazione finora

- Avila V BarabatDocumento2 pagineAvila V BarabatRosana Villordon SoliteNessuna valutazione finora

- 135 Enlisted Political Parties With BioDocumento12 pagine135 Enlisted Political Parties With BioRabab RazaNessuna valutazione finora

- Department of Education: Attendance SheetDocumento2 pagineDepartment of Education: Attendance SheetLiam Sean Han100% (1)

- SAN JUAN ES. Moncada North Plantilla 1Documento1 paginaSAN JUAN ES. Moncada North Plantilla 1Jasmine Faye Gamotea - CabayaNessuna valutazione finora

- Tamil Nadu Public Service Commission Regulations, 1954: (Corrected Up To 29.02.2020)Documento93 pagineTamil Nadu Public Service Commission Regulations, 1954: (Corrected Up To 29.02.2020)DhivakaranNessuna valutazione finora

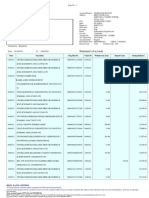

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocumento3 pagineStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceHiten AhirNessuna valutazione finora

- US v. Esmedia G.R. No. L-5749 PDFDocumento3 pagineUS v. Esmedia G.R. No. L-5749 PDFfgNessuna valutazione finora

- 10 FixedAsset 21 FixedAsset InitSettingsDocumento32 pagine10 FixedAsset 21 FixedAsset InitSettingsCrazy TechNessuna valutazione finora

- SurrogacyDocumento17 pagineSurrogacypravas naikNessuna valutazione finora

- New LLM Corporate PDFDocumento20 pagineNew LLM Corporate PDFshubhambulbule7274Nessuna valutazione finora

- CloverfieldDocumento1 paginaCloverfieldKaran HanamanNessuna valutazione finora

- Method NIFTY Equity Indices PDFDocumento130 pagineMethod NIFTY Equity Indices PDFGita ThoughtsNessuna valutazione finora

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Documento1 paginaTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)RMNessuna valutazione finora

- Informal Market and Work Decent 212689Documento507 pagineInformal Market and Work Decent 212689Lenin Dos Santos PiresNessuna valutazione finora

- PWC Permanent Establishments at The Heart of The Matter FinalDocumento24 paginePWC Permanent Establishments at The Heart of The Matter Finalvoyager8002Nessuna valutazione finora

- The Last Hacker: He Called Himself Dark Dante. His Compulsion Led Him To Secret Files And, Eventually, The Bar of JusticeDocumento16 pagineThe Last Hacker: He Called Himself Dark Dante. His Compulsion Led Him To Secret Files And, Eventually, The Bar of JusticeRomulo Rosario MarquezNessuna valutazione finora

- Assignment On Satyam Scam PGDM Vii A 2009-2011Documento5 pagineAssignment On Satyam Scam PGDM Vii A 2009-2011mishikaachuNessuna valutazione finora

- Foaming at The MouthDocumento1 paginaFoaming at The Mouth90JDSF8938JLSNF390J3Nessuna valutazione finora

- In The Matter of The IBP 1973Documento6 pagineIn The Matter of The IBP 1973Nana SanNessuna valutazione finora

- Credcases Atty. BananaDocumento12 pagineCredcases Atty. BananaKobe BullmastiffNessuna valutazione finora

- Notice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsDocumento1 paginaNotice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsJustia.comNessuna valutazione finora

- Child OffendersDocumento35 pagineChild OffendersMuhd Nur SadiqinNessuna valutazione finora