Potrebbero piacerti anche

- HK (Ifric) Int 12Documento41 pagineHK (Ifric) Int 12Wahid Ben MohamedNessuna valutazione finora

- ToaDocumento5 pagineToaGelyn CruzNessuna valutazione finora

- Intangibles, Wasting A, ImpairmentDocumento4 pagineIntangibles, Wasting A, ImpairmentJobelle Candace Flores AbreraNessuna valutazione finora

- Studet Practical Accounting Ch17 PPE AcquisitionDocumento16 pagineStudet Practical Accounting Ch17 PPE Acquisitionsabina del monteNessuna valutazione finora

- Installment Method Tax Reporting GuideDocumento2 pagineInstallment Method Tax Reporting GuideJadeNessuna valutazione finora

- Finals Exercise 2 - WC Management InventoryDocumento3 pagineFinals Exercise 2 - WC Management Inventorywin win0% (1)

- Mahusay Acc3112 Major Output 2Documento2 pagineMahusay Acc3112 Major Output 2Jeth Mahusay100% (1)

- Aud Theo Reviewer Chap 3 To 5Documento55 pagineAud Theo Reviewer Chap 3 To 5Angelica DuarteNessuna valutazione finora

- Capital Structure Policy: Fourth EditionDocumento48 pagineCapital Structure Policy: Fourth EditionNatasya FlorenciaNessuna valutazione finora

- Auditing Problems Key Answers/solutions: Problem No. 1 1.A, 2.C, 3.B, 4.B, 5.DDocumento14 pagineAuditing Problems Key Answers/solutions: Problem No. 1 1.A, 2.C, 3.B, 4.B, 5.DKim Cristian MaañoNessuna valutazione finora

- Accounting for Debt InstrumentsDocumento4 pagineAccounting for Debt InstrumentsKeahlyn Boticario CapinaNessuna valutazione finora

- Try This - Cost ConceptsDocumento6 pagineTry This - Cost ConceptsStefan John SomeraNessuna valutazione finora

- FINALS - Theory of AccountsDocumento8 pagineFINALS - Theory of AccountsAngela ViernesNessuna valutazione finora

- Credit 5Documento7 pagineCredit 5Maria SyNessuna valutazione finora

- Preweek ReviewDocumento31 paginePreweek ReviewLeah Hope CedroNessuna valutazione finora

- Polytechnic University of The Philippines College of AccountancyDocumento11 paginePolytechnic University of The Philippines College of AccountancyRonel CacheroNessuna valutazione finora

- A. Property, Plant and Equipment:: Current Appraised Value Seller's Original CostDocumento3 pagineA. Property, Plant and Equipment:: Current Appraised Value Seller's Original CostNORLYN CINCONessuna valutazione finora

- Philippine Interpretations Committee (Pic) Questions and Answers (Q&As)Documento6 paginePhilippine Interpretations Committee (Pic) Questions and Answers (Q&As)verycooling100% (1)

- FAR - Estimating Inventory - StudentDocumento3 pagineFAR - Estimating Inventory - StudentPamelaNessuna valutazione finora

- (Fingerprints Group) 2011 CIMA Global Business Challenge ReportDocumento23 pagine(Fingerprints Group) 2011 CIMA Global Business Challenge Reportcrazyfrog1991Nessuna valutazione finora

- Midterm Quiz 2Documento11 pagineMidterm Quiz 2SGwannaBNessuna valutazione finora

- Ac3a Qe Oct2014 (TQ)Documento15 pagineAc3a Qe Oct2014 (TQ)Julrick Cubio EgbusNessuna valutazione finora

- Heats Corporation Current and Noncurrent LiabilitiesDocumento1 paginaHeats Corporation Current and Noncurrent LiabilitiesjhobsNessuna valutazione finora

- Examination About Investment 8Documento3 pagineExamination About Investment 8BLACKPINKLisaRoseJisooJennieNessuna valutazione finora

- Auditing and Assurance: Specialized Industries - Midterm ExaminationDocumento14 pagineAuditing and Assurance: Specialized Industries - Midterm ExaminationHannah SyNessuna valutazione finora

- Far Eastern University - Makati: Discussion ProblemsDocumento2 pagineFar Eastern University - Makati: Discussion ProblemsMarielle SidayonNessuna valutazione finora

- Preweek Practical Accounting 1Documento24 paginePreweek Practical Accounting 1alellieNessuna valutazione finora

- CMA Exam Review - Part 2 AssessmentDocumento66 pagineCMA Exam Review - Part 2 AssessmentAlyssa PilapilNessuna valutazione finora

- Prelims Ms1Documento6 paginePrelims Ms1ALMA MORENANessuna valutazione finora

- Intangibles PDFDocumento5 pagineIntangibles PDFJer RamaNessuna valutazione finora

- Practical Accounting Problems SolutionsDocumento11 paginePractical Accounting Problems SolutionsjustjadeNessuna valutazione finora

- Mas QuestionsDocumento2 pagineMas QuestionsEll VNessuna valutazione finora

- College of Accountancy & Economics Auditing Theory DocumentDocumento15 pagineCollege of Accountancy & Economics Auditing Theory DocumentmaekaellaNessuna valutazione finora

- ReceivablesDocumento4 pagineReceivablesKentaro Panergo NumasawaNessuna valutazione finora

- Bastrcsx q1m Set BDocumento9 pagineBastrcsx q1m Set BAdrian MontemayorNessuna valutazione finora

- Peer Mentoring PostTestDocumento7 paginePeer Mentoring PostTestronnelNessuna valutazione finora

- FAR.3405 PPE-Acquisition and Subsequent ExpendituresDocumento6 pagineFAR.3405 PPE-Acquisition and Subsequent ExpendituresMonica GarciaNessuna valutazione finora

- HW On Operating Segments BDocumento3 pagineHW On Operating Segments BJazehl Joy ValdezNessuna valutazione finora

- MIdterm ExamDocumento8 pagineMIdterm ExamMarcellana ArianeNessuna valutazione finora

- Consolidated Net Income and NCII CaseDocumento9 pagineConsolidated Net Income and NCII CaseJeth MahusayNessuna valutazione finora

- Discussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocumento3 pagineDiscussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoRaymond RosalesNessuna valutazione finora

- Management Advisory ServicesDocumento11 pagineManagement Advisory ServicesAnonymous 7m9SLrNessuna valutazione finora

- Book 7Documento2 pagineBook 7Actg SolmanNessuna valutazione finora

- Investment in Associate Problems AnswersDocumento9 pagineInvestment in Associate Problems AnswersMytha Isabel SalesNessuna valutazione finora

- Acct 3Documento25 pagineAcct 3Diego Salazar100% (1)

- Quiz InvestmentsDocumento2 pagineQuiz InvestmentsstillwinmsNessuna valutazione finora

- CA51017 Departmentals Quiz 2 and Quiz 3Documento13 pagineCA51017 Departmentals Quiz 2 and Quiz 3artemisNessuna valutazione finora

- App ADocumento87 pagineApp AJessica Cola0% (1)

- Investment PropertyDocumento3 pagineInvestment PropertyacyNessuna valutazione finora

- Batch 18 1st Preboard (P1)Documento14 pagineBatch 18 1st Preboard (P1)Jericho PedragosaNessuna valutazione finora

- Fitz Music Company Financial Accounting 2 ReviewDocumento5 pagineFitz Music Company Financial Accounting 2 ReviewFitz Gerald BalbaNessuna valutazione finora

- Aud Prob Part 2Documento52 pagineAud Prob Part 2Ma. Hazel Donita DiazNessuna valutazione finora

- Bonds Payable: Prepare The Entries To Record The Above TransactionsDocumento6 pagineBonds Payable: Prepare The Entries To Record The Above TransactionsJay-L TanNessuna valutazione finora

- REVIEW QUESTIONS Investment in Debt SecuritiesDocumento1 paginaREVIEW QUESTIONS Investment in Debt SecuritiesJake BundokNessuna valutazione finora

- Chapter 5 Property, Plant and Equipment GuideDocumento14 pagineChapter 5 Property, Plant and Equipment GuideNaSheeng100% (1)

- Cuartero - Unit 3 - Accounting Changes and Error CorrectionDocumento10 pagineCuartero - Unit 3 - Accounting Changes and Error CorrectionAim RubiaNessuna valutazione finora

- Intangible MCDocumento49 pagineIntangible MCAnonymous zpUO2SNessuna valutazione finora

- AAA TOA Review QuizbowlDocumento50 pagineAAA TOA Review QuizbowlVINCENT GAYRAMONNessuna valutazione finora

- Midterm - Exam PDFDocumento16 pagineMidterm - Exam PDFLouisse Marie Catipay100% (1)

- Manual OiDocumento30 pagineManual Oiudhaya kumarNessuna valutazione finora

- CFO in Denver Colorado Resume Bruce PeeleDocumento2 pagineCFO in Denver Colorado Resume Bruce PeeleBruce PeeleNessuna valutazione finora

- 72 Inventory Management and Financial PeDocumento22 pagine72 Inventory Management and Financial PeKiersteen AnasNessuna valutazione finora

- CH 4 The Dawn of A New Order in Commodity TradingDocumento7 pagineCH 4 The Dawn of A New Order in Commodity TradingDevang BharaniaNessuna valutazione finora

- CH 15Documento20 pagineCH 15grace guiuanNessuna valutazione finora

- Problem Overview:: 2B PeopleDocumento5 pagineProblem Overview:: 2B PeopleSebastian AlexNessuna valutazione finora

- WSO Experienced Deals Resume Template-Transaction-Exp2 (1) 0Documento2 pagineWSO Experienced Deals Resume Template-Transaction-Exp2 (1) 0jason.sevin02Nessuna valutazione finora

- IDirect KalpataruPower Q2FY20Documento10 pagineIDirect KalpataruPower Q2FY20QuestAviatorNessuna valutazione finora

- EPD Handbook 2012electronic VersionDocumento265 pagineEPD Handbook 2012electronic VersionAnonymous iVNvuRKGVNessuna valutazione finora

- SHARESDocumento5 pagineSHARESMohammad Tariq AnsariNessuna valutazione finora

- High Probability Trading Setups For The Currency Market PDFDocumento100 pagineHigh Probability Trading Setups For The Currency Market PDFDavid VenancioNessuna valutazione finora

- MIC ELECTRONICS LTD BUY OPPORTUNITYDocumento17 pagineMIC ELECTRONICS LTD BUY OPPORTUNITYSudipta BoseNessuna valutazione finora

- A Case Study Entitled: The Collapse of Lehman BrothersDocumento10 pagineA Case Study Entitled: The Collapse of Lehman BrothersRoby IbeNessuna valutazione finora

- NRI Investments in IndiaDocumento3 pagineNRI Investments in IndiaRahul BediNessuna valutazione finora

- Inflation Impact on Monthly Expenditure over 30 YearsDocumento8 pagineInflation Impact on Monthly Expenditure over 30 Yearslove4u1lyNessuna valutazione finora

- UK Financial Regulations (Easily Understood) - Revision Guide For CeMap/CeFA 1 SampleDocumento14 pagineUK Financial Regulations (Easily Understood) - Revision Guide For CeMap/CeFA 1 Sampleadetomiruksons100% (1)

- Nikko AM Shenton Singapore Dividend Equity Fund SGD - Fund Fact SheetDocumento3 pagineNikko AM Shenton Singapore Dividend Equity Fund SGD - Fund Fact SheetSaran SNessuna valutazione finora

- Individual Assignment 1 PDFDocumento5 pagineIndividual Assignment 1 PDFNanthini KrishnanNessuna valutazione finora

- Revenue StreamDocumento11 pagineRevenue Stream1B053Faura Finda FantasticNessuna valutazione finora

- Feed The Future, Tanzania Land Tenure Assistance: DAI GlobalDocumento57 pagineFeed The Future, Tanzania Land Tenure Assistance: DAI GlobalJacob PeterNessuna valutazione finora

- Nasdaq Composite White PaperDocumento8 pagineNasdaq Composite White PaperavaresearchNessuna valutazione finora

- Business Plan for Green Investments Financial Service CompanyDocumento25 pagineBusiness Plan for Green Investments Financial Service CompanyAyush BakshiNessuna valutazione finora

- Mod 1 - Framework For Analysis & ValuationDocumento33 pagineMod 1 - Framework For Analysis & ValuationbobdoleNessuna valutazione finora

- Curso Forex Novato A Professional Más 60 Vídeos Explicativos PDFDocumento5 pagineCurso Forex Novato A Professional Más 60 Vídeos Explicativos PDFLUISA SANCHEZNessuna valutazione finora

- Session 1 - FM Function and Basic Investment Appraisal: ACCA F9 Financial ManagementDocumento8 pagineSession 1 - FM Function and Basic Investment Appraisal: ACCA F9 Financial ManagementKodwoPNessuna valutazione finora

- Questions Number One P LTD and Its Subsidiary Consolidated Income Statement For The Year Ended 31 December 2003Documento29 pagineQuestions Number One P LTD and Its Subsidiary Consolidated Income Statement For The Year Ended 31 December 2003JOHN KAMANDANessuna valutazione finora

- PR - Order in The Matter of M/s. Phenix Properties LimitedDocumento2 paginePR - Order in The Matter of M/s. Phenix Properties LimitedShyam SunderNessuna valutazione finora

- Chapter No. 4: Currency Pairs, Foreign Exchange Market and ImsDocumento52 pagineChapter No. 4: Currency Pairs, Foreign Exchange Market and ImsCh MoonNessuna valutazione finora

- Abfm Formula PDFDocumento20 pagineAbfm Formula PDFSandeep KumarNessuna valutazione finora

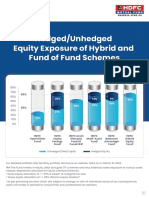

- Leaflet - Hedged and Unhedged Exposure of Hybrid FundsDocumento2 pagineLeaflet - Hedged and Unhedged Exposure of Hybrid FundsDeepakNessuna valutazione finora

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsDa EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNessuna valutazione finora

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Da EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Valutazione: 5 su 5 stelle5/5 (75)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantDa EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantValutazione: 4 su 5 stelle4/5 (104)

- Rich Nurse Poor Nurses The Critical Stuff Nursing School Forgot To Teach YouDa EverandRich Nurse Poor Nurses The Critical Stuff Nursing School Forgot To Teach YouNessuna valutazione finora

- Make Your Money Work For You: Think big, start smallDa EverandMake Your Money Work For You: Think big, start smallNessuna valutazione finora

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassDa EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNessuna valutazione finora

- Sacred Success: A Course in Financial MiraclesDa EverandSacred Success: A Course in Financial MiraclesValutazione: 5 su 5 stelle5/5 (15)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesDa EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesValutazione: 4.5 su 5 stelle4.5/5 (30)

- Improve Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouDa EverandImprove Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouValutazione: 5 su 5 stelle5/5 (5)

- How to Teach Economics to Your Dog: A Quirky IntroductionDa EverandHow to Teach Economics to Your Dog: A Quirky IntroductionNessuna valutazione finora

- How To Budget And Manage Your Money In 7 Simple StepsDa EverandHow To Budget And Manage Your Money In 7 Simple StepsValutazione: 5 su 5 stelle5/5 (4)

- Swot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessDa EverandSwot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessValutazione: 4.5 su 5 stelle4.5/5 (4)

- Happy Go Money: Spend Smart, Save Right and Enjoy LifeDa EverandHappy Go Money: Spend Smart, Save Right and Enjoy LifeValutazione: 5 su 5 stelle5/5 (4)

- The Best Team Wins: The New Science of High PerformanceDa EverandThe Best Team Wins: The New Science of High PerformanceNessuna valutazione finora

- Basic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonDa EverandBasic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonValutazione: 5 su 5 stelle5/5 (9)

- Budgeting: The Ultimate Guide for Getting Your Finances TogetherDa EverandBudgeting: The Ultimate Guide for Getting Your Finances TogetherValutazione: 5 su 5 stelle5/5 (14)

- Money Made Easy: How to Budget, Pay Off Debt, and Save MoneyDa EverandMoney Made Easy: How to Budget, Pay Off Debt, and Save MoneyValutazione: 5 su 5 stelle5/5 (1)

- Retirement Reality Check: How to Spend Your Money and Still Leave an Amazing LegacyDa EverandRetirement Reality Check: How to Spend Your Money and Still Leave an Amazing LegacyNessuna valutazione finora

- Lean but Agile: Rethink Workforce Planning and Gain a True Competitive EdgeDa EverandLean but Agile: Rethink Workforce Planning and Gain a True Competitive EdgeNessuna valutazione finora

- Money Management: The Ultimate Guide to Budgeting, Frugal Living, Getting out of Debt, Credit Repair, and Managing Your Personal Finances in a Stress-Free WayDa EverandMoney Management: The Ultimate Guide to Budgeting, Frugal Living, Getting out of Debt, Credit Repair, and Managing Your Personal Finances in a Stress-Free WayValutazione: 3.5 su 5 stelle3.5/5 (2)

- The New York Times Pocket MBA Series: Forecasting Budgets: 25 Keys to Successful PlanningDa EverandThe New York Times Pocket MBA Series: Forecasting Budgets: 25 Keys to Successful PlanningValutazione: 4.5 su 5 stelle4.5/5 (8)

- How to Save Money: 100 Ways to Live a Frugal LifeDa EverandHow to Save Money: 100 Ways to Live a Frugal LifeValutazione: 5 su 5 stelle5/5 (1)