Potrebbero piacerti anche

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Indian Chief Motorcycles, 1922-1953 (Motorcycle Color History)Documento132 pagineIndian Chief Motorcycles, 1922-1953 (Motorcycle Color History)Craciun Sabian100% (6)

- PSI 8.8L ServiceDocumento197 paginePSI 8.8L Serviceedelmolina100% (1)

- WSM - Ziale - Commercial Law NotesDocumento36 pagineWSM - Ziale - Commercial Law NotesElizabeth Chilufya100% (1)

- Unit I Lesson Ii Roles of A TeacherDocumento7 pagineUnit I Lesson Ii Roles of A TeacherEvergreens SalongaNessuna valutazione finora

- Practice Career Professionalis PDFDocumento29 paginePractice Career Professionalis PDFRo Ma SantaNessuna valutazione finora

- SYLVANIA W6413tc - SMDocumento46 pagineSYLVANIA W6413tc - SMdreamyson1983100% (1)

- NYPE93Documento0 pagineNYPE93gvsprajuNessuna valutazione finora

- Bank Reconciliation and Proof of CashDocumento2 pagineBank Reconciliation and Proof of CashDarwyn HonaNessuna valutazione finora

- Buyer Persona TemplateDocumento18 pagineBuyer Persona TemplateH ANessuna valutazione finora

- 5d814c4d6437b300fd0e227a - Scorch Product Sheet 512GB PDFDocumento1 pagina5d814c4d6437b300fd0e227a - Scorch Product Sheet 512GB PDFBobby B. BrownNessuna valutazione finora

- Witness Affidavit of Emeteria B, ZuasolaDocumento4 pagineWitness Affidavit of Emeteria B, ZuasolaNadin MorgadoNessuna valutazione finora

- Calculate PostageDocumento4 pagineCalculate PostageShivam ThakurNessuna valutazione finora

- TUV300 T4 Plus Vs TUV300 T6 Plus Vs TUV300 T8 Vs TUV300 T10 - CarWaleDocumento12 pagineTUV300 T4 Plus Vs TUV300 T6 Plus Vs TUV300 T8 Vs TUV300 T10 - CarWalernbansalNessuna valutazione finora

- FairyDocumento1 paginaFairyprojekti.jasminNessuna valutazione finora

- Turn Pet1 Plastic Bottles Into 3d Filament With The Recreator 3d Mk5kit Ender3 b7936987 A5e5 4b10 80fa 8754423f3ee8Documento11 pagineTurn Pet1 Plastic Bottles Into 3d Filament With The Recreator 3d Mk5kit Ender3 b7936987 A5e5 4b10 80fa 8754423f3ee8Meet MehtaNessuna valutazione finora

- Marine Products: SL-3 Engine ControlsDocumento16 pagineMarine Products: SL-3 Engine ControlsPedro GuerraNessuna valutazione finora

- Which Among The Following Statement Is INCORRECTDocumento7 pagineWhich Among The Following Statement Is INCORRECTJyoti SinghNessuna valutazione finora

- PCB Design PCB Design: Dr. P. C. PandeyDocumento13 paginePCB Design PCB Design: Dr. P. C. PandeyengshimaaNessuna valutazione finora

- By Daphne Greaves Illustrated by Michela GalassiDocumento15 pagineBy Daphne Greaves Illustrated by Michela GalassiLucian DilgociNessuna valutazione finora

- Rosmary PollockDocumento4 pagineRosmary PollockhbNessuna valutazione finora

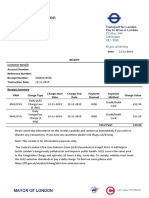

- Transport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDocumento1 paginaTransport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDanyy MaciucNessuna valutazione finora

- Landini Tractor 7000 Special Parts Catalog 1820423m1Documento22 pagineLandini Tractor 7000 Special Parts Catalog 1820423m1katrinaflowers160489rde100% (122)

- Today Mass Coloration in The Lndustri-Al Environment: Lenzinger BerichteDocumento5 pagineToday Mass Coloration in The Lndustri-Al Environment: Lenzinger BerichteAditya ShrivastavaNessuna valutazione finora

- Case Study: Meera P NairDocumento9 pagineCase Study: Meera P Nairnanditha menonNessuna valutazione finora

- Catalogo AMF Herramientas para AtornillarDocumento76 pagineCatalogo AMF Herramientas para Atornillarabelmonte_geotecniaNessuna valutazione finora

- Unix Training ContentDocumento5 pagineUnix Training ContentsathishkumarNessuna valutazione finora

- Trabajo Final CERVEZA OLMECADocumento46 pagineTrabajo Final CERVEZA OLMECAramon nemeNessuna valutazione finora

- Intermediate Microeconomics and Its Application 12th Edition Nicholson Solutions ManualDocumento9 pagineIntermediate Microeconomics and Its Application 12th Edition Nicholson Solutions Manualchiliasmevenhandtzjz8j100% (27)

- Surveillance of Healthcare-Associated Infections in Indonesian HospitalsDocumento12 pagineSurveillance of Healthcare-Associated Infections in Indonesian HospitalsRidha MardiyaniNessuna valutazione finora

- Hippa and ISO MappingDocumento13 pagineHippa and ISO Mappingnidelel214Nessuna valutazione finora