Potrebbero piacerti anche

- Project Financing To The SME Sector: by N.Thanesh Credit Workshop RHO-JaffnaDocumento38 pagineProject Financing To The SME Sector: by N.Thanesh Credit Workshop RHO-Jaffnachintu_thakkar9Nessuna valutazione finora

- Working Capital ManagementDocumento55 pagineWorking Capital ManagementsharmamunuNessuna valutazione finora

- F307 Lecture NotesDocumento49 pagineF307 Lecture Noteskjiang123Nessuna valutazione finora

- Understanding Working Capital Management and Financing: Management of Current AssetsDocumento42 pagineUnderstanding Working Capital Management and Financing: Management of Current AssetsShubham KesharwaniNessuna valutazione finora

- Assessment of Working CapitalDocumento55 pagineAssessment of Working CapitalShivam Goyal0% (1)

- Effective Working CapitalDocumento23 pagineEffective Working CapitalUmmed SinghoyaNessuna valutazione finora

- PgcWorking Capital AssessmentDocumento39 paginePgcWorking Capital AssessmentTapan Kumar DasNessuna valutazione finora

- Assessment: Canterbury Business CollegeDocumento28 pagineAssessment: Canterbury Business Collegemilan shrestha20% (5)

- Discounted Cash Flow Demystified: A Comprehensive Guide to DCF BudgetingDa EverandDiscounted Cash Flow Demystified: A Comprehensive Guide to DCF BudgetingNessuna valutazione finora

- L-5&6 642 ReserveDocumento44 pagineL-5&6 642 ReserveNiloy AhmedNessuna valutazione finora

- Short Term Finance and PlanningDocumento32 pagineShort Term Finance and PlanningAnonymous jGew8BNessuna valutazione finora

- Fin650 Lectures 1-2Documento64 pagineFin650 Lectures 1-2Arif H JewelNessuna valutazione finora

- An Introduction To Treasury Management: David ChefneuxDocumento39 pagineAn Introduction To Treasury Management: David ChefneuxAmitNessuna valutazione finora

- Credit AppraisalDocumento46 pagineCredit AppraisalApekshaNessuna valutazione finora

- An Introduction To Treasury Management: David ChefneuxDocumento39 pagineAn Introduction To Treasury Management: David ChefneuxJerome RandolphNessuna valutazione finora

- The New CFO Financial Leadership ManualDa EverandThe New CFO Financial Leadership ManualValutazione: 3.5 su 5 stelle3.5/5 (3)

- Idbi Bank LTDDocumento39 pagineIdbi Bank LTDFahad KhanNessuna valutazione finora

- S 13 - Cash and Credit ManagementDocumento41 pagineS 13 - Cash and Credit ManagementAninda DuttaNessuna valutazione finora

- Tarea 6 MergedDocumento20 pagineTarea 6 MergedJulio Pablo García VásquezNessuna valutazione finora

- 11 Working Capital ManagementDocumento34 pagine11 Working Capital Managementaashulheda100% (1)

- Series 24 Exam Study Guide 2022 + Test BankDa EverandSeries 24 Exam Study Guide 2022 + Test BankNessuna valutazione finora

- SERIES 24 EXAM STUDY GUIDE 2021 + TEST BANKDa EverandSERIES 24 EXAM STUDY GUIDE 2021 + TEST BANKNessuna valutazione finora

- Working Capital Mgt.Documento18 pagineWorking Capital Mgt.preetirblNessuna valutazione finora

- Lending Operations 7Documento19 pagineLending Operations 7Faraz Ahmed FarooqiNessuna valutazione finora

- PDFDocumento507 paginePDFAmol MandhaneNessuna valutazione finora

- Market and Demand AnalysisDocumento13 pagineMarket and Demand Analysistheanuuradha1993gmaiNessuna valutazione finora

- Assets & Liabilities Management AT The Union Co-Operative Bank LTDDocumento21 pagineAssets & Liabilities Management AT The Union Co-Operative Bank LTDapluNessuna valutazione finora

- CF Module 7 - Scflows Pas 7Documento13 pagineCF Module 7 - Scflows Pas 7Jomic QuimsonNessuna valutazione finora

- Series 22 Exam Study Guide 2022 + Test BankDa EverandSeries 22 Exam Study Guide 2022 + Test BankNessuna valutazione finora

- Receivables ManagementDocumento8 pagineReceivables Managementramteja_hbs14Nessuna valutazione finora

- Chapter - 1: Snack BarDocumento60 pagineChapter - 1: Snack BarWasim KhanNessuna valutazione finora

- Presentation On Appraisal of Project Report: Bank's PerspectiveDocumento19 paginePresentation On Appraisal of Project Report: Bank's PerspectivejvijaymbaNessuna valutazione finora

- Project Appraisal and Financing: Dr. Sudhindra BhatDocumento56 pagineProject Appraisal and Financing: Dr. Sudhindra Bhatgaurang1111Nessuna valutazione finora

- Bank LendingDocumento21 pagineBank LendingSRINIVASDARBHANessuna valutazione finora

- Baskin RobbinsDocumento65 pagineBaskin RobbinsShikha AgrawalNessuna valutazione finora

- ICRA Securitisation Rating Methodology PDFDocumento32 pagineICRA Securitisation Rating Methodology PDFShivani AgarwalNessuna valutazione finora

- Bank Financial Analysis PresentationDocumento24 pagineBank Financial Analysis PresentationlevuthiNessuna valutazione finora

- Citi Trade May14Documento23 pagineCiti Trade May14Marlon RelatadoNessuna valutazione finora

- Theories of Liquidity ManagementDocumento12 pagineTheories of Liquidity Managementamir_saheedNessuna valutazione finora

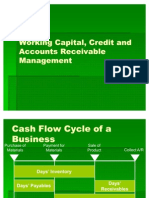

- Working Capital, Credit and Accounts Receivable ManagementDocumento31 pagineWorking Capital, Credit and Accounts Receivable ManagementAnkit AgarwalNessuna valutazione finora

- CH 11 PPTsDocumento76 pagineCH 11 PPTshariyadi030267313Nessuna valutazione finora

- Managing Financial Principles and TechniquesDocumento16 pagineManaging Financial Principles and TechniquesGimhan Godawatte50% (2)

- Dividend Policy & Working Capital ManagementDocumento17 pagineDividend Policy & Working Capital ManagementRitika AswaniNessuna valutazione finora

- Chapter Eleven: Liquidity and Reserve Management: Strategies and PoliciesDocumento23 pagineChapter Eleven: Liquidity and Reserve Management: Strategies and PoliciesTarique AdnanNessuna valutazione finora

- Working Capital Management: Executive Development ProgramDocumento148 pagineWorking Capital Management: Executive Development ProgramsajjukrishNessuna valutazione finora

- Series 22 Exam Review Study GuideDa EverandSeries 22 Exam Review Study GuideNessuna valutazione finora

- Fixed Income Markets: Instruments, Applications, MathematicsDa EverandFixed Income Markets: Instruments, Applications, MathematicsNessuna valutazione finora

- Role of Financial Manager: Objective Is To AssessDocumento31 pagineRole of Financial Manager: Objective Is To AssessMarc Benedict TalamayanNessuna valutazione finora

- Credit Risk MGTDocumento9 pagineCredit Risk MGTPrakashSahaNessuna valutazione finora

- CF Assignment 1Documento22 pagineCF Assignment 1Er. THAMIZHMANI MNessuna valutazione finora

- QuestionnairesDocumento3 pagineQuestionnairesshahidjappaNessuna valutazione finora

- Monitoring & Follow Up of Advances: H S Sharma, Guest Faculty, IIBFDocumento51 pagineMonitoring & Follow Up of Advances: H S Sharma, Guest Faculty, IIBFBhaskara Sita Ramayya PNessuna valutazione finora

- Overview of Financial ManagementDocumento97 pagineOverview of Financial ManagementKhadim HussainNessuna valutazione finora

- Wiley CMA Learning System Exam Review 2013, Financial Decision Making, + Test BankDa EverandWiley CMA Learning System Exam Review 2013, Financial Decision Making, + Test BankValutazione: 5 su 5 stelle5/5 (1)

- Wiley CMA Learning System Exam Review 2013, Financial Decision Making, Online Intensive Review + Test BankDa EverandWiley CMA Learning System Exam Review 2013, Financial Decision Making, Online Intensive Review + Test BankNessuna valutazione finora

- Overview of Credit AppraisalDocumento14 pagineOverview of Credit AppraisalAsim MahatoNessuna valutazione finora

- Customer-Anchored Supply Chains: An Executive’S Guide to Building Competitive Advantage in the Oil PatchDa EverandCustomer-Anchored Supply Chains: An Executive’S Guide to Building Competitive Advantage in the Oil PatchNessuna valutazione finora

- Session 03: Principles of Working Capital ManagementDocumento47 pagineSession 03: Principles of Working Capital ManagementiitrbatNessuna valutazione finora

- Goals-Based Wealth Management: An Integrated and Practical Approach to Changing the Structure of Wealth Advisory PracticesDa EverandGoals-Based Wealth Management: An Integrated and Practical Approach to Changing the Structure of Wealth Advisory PracticesNessuna valutazione finora

- E3sconf Netid2021 02032Documento7 pagineE3sconf Netid2021 02032prabathnilanNessuna valutazione finora

- Summer Training SwapnilDocumento94 pagineSummer Training SwapnilSwapnil Kumar SinghNessuna valutazione finora

- Competing GloballyDocumento59 pagineCompeting GloballyTarun GargNessuna valutazione finora

- 2023.07.07 HS PaeDocumento2 pagine2023.07.07 HS Paehanis0% (1)

- SAP MM - Procurement ScenarioDocumento6 pagineSAP MM - Procurement Scenariosyamsu866764100% (1)

- Purchase Order Financing AgreementDocumento6 paginePurchase Order Financing AgreementMoffat Nyamadzawo100% (1)

- Business Plan Format Commercial BankDocumento5 pagineBusiness Plan Format Commercial Bankassefamenelik1100% (2)

- Speed-To-Fashion Managing Global Supply Chain in ZaraDocumento6 pagineSpeed-To-Fashion Managing Global Supply Chain in Zararabna akbarNessuna valutazione finora

- Aurora Textile CompanyDocumento47 pagineAurora Textile CompanyMoHadrielCharki63% (8)

- DSM Textile Industry at KarurDocumento79 pagineDSM Textile Industry at KarurMeena Sivasubramanian0% (1)

- Building The Virtual Lab - Global Licensing and Partnering at MerckDocumento1 paginaBuilding The Virtual Lab - Global Licensing and Partnering at MerckrobertsNessuna valutazione finora

- Case Application: Higher and HigherDocumento6 pagineCase Application: Higher and HigherJomarie AlcanoNessuna valutazione finora

- Project On Comparison Between Stock BrokersDocumento15 pagineProject On Comparison Between Stock BrokersankitsawhneyNessuna valutazione finora

- Calderon, Reynan C. Bsa-32a1 Current Market Description, Demand Supply AnalysisDocumento4 pagineCalderon, Reynan C. Bsa-32a1 Current Market Description, Demand Supply AnalysisReynan Calo CalderonNessuna valutazione finora

- Unit 3 - Bookkeping-1-2Documento2 pagineUnit 3 - Bookkeping-1-2JHON ALEJANDRO GALLEGO GALINDONessuna valutazione finora

- MGT603 Solved MCQs From Book by Fred (Chap 7)Documento4 pagineMGT603 Solved MCQs From Book by Fred (Chap 7)Fan CageNessuna valutazione finora

- Assessing Financial Health (Part-A)Documento17 pagineAssessing Financial Health (Part-A)kohacNessuna valutazione finora

- APQP Timing Plan TemplateDocumento9 pagineAPQP Timing Plan TemplatemuthuselvanNessuna valutazione finora

- Titan IndustryDocumento13 pagineTitan IndustryVeera KumarNessuna valutazione finora

- Lenovo Case AnalysisDocumento4 pagineLenovo Case AnalysisYasmin Gloria100% (1)

- MPRA Paper 36046Documento30 pagineMPRA Paper 36046LiYi ChenNessuna valutazione finora

- 11 AccDocumento6 pagine11 AccPushpinder KumarNessuna valutazione finora

- Stork Risk Management ToolboxDocumento37 pagineStork Risk Management ToolboxSamuelFarfanNessuna valutazione finora

- Auditing ManualTC7Documento264 pagineAuditing ManualTC7Alinafe SteshaNessuna valutazione finora

- DSS, GDSSDocumento49 pagineDSS, GDSSAhmed MujtabaNessuna valutazione finora

- BUSINESS FINANCE (Week 6)Documento4 pagineBUSINESS FINANCE (Week 6)elyra blythe salcedoNessuna valutazione finora

- Cocacola TQM ProjectDocumento18 pagineCocacola TQM ProjectOmer Farooq92% (13)

- MComDocumento32 pagineMComTuki DasNessuna valutazione finora

- Ptmail - m1221 - Ss - 2 High Growth Stocks For A Millionaires Portfolio Dec21Documento16 paginePtmail - m1221 - Ss - 2 High Growth Stocks For A Millionaires Portfolio Dec21PIYUSH GOPALNessuna valutazione finora

- Sox-Itgc Compliance & Pci: Archisman Sen Clément Renouvel Deepa Pravinchandra Patel Justine MerletDocumento38 pagineSox-Itgc Compliance & Pci: Archisman Sen Clément Renouvel Deepa Pravinchandra Patel Justine MerletThais Ribeiro100% (1)