Potrebbero piacerti anche

- Writ of MandamusDocumento2 pagineWrit of MandamusMalikBey100% (3)

- PAO OFFICIALS and Contact InformationDocumento28 paginePAO OFFICIALS and Contact InformationClaire Culminas50% (2)

- Aboitiz Shipping vs. CADocumento1 paginaAboitiz Shipping vs. CAHenri VasquezNessuna valutazione finora

- Template Workplace PoliciesDocumento26 pagineTemplate Workplace PoliciesJCapskyNessuna valutazione finora

- Insurance Cases Judge Ella EscalanteDocumento10 pagineInsurance Cases Judge Ella EscalanteJeckNessuna valutazione finora

- Insurance Digests - PolicyDocumento15 pagineInsurance Digests - Policyviva_33Nessuna valutazione finora

- Insurance Suretyship Case-DigestDocumento8 pagineInsurance Suretyship Case-DigestBleizel TeodosioNessuna valutazione finora

- Joining Report Cum Employment FormDocumento8 pagineJoining Report Cum Employment Formameetranjan73% (15)

- Sample Affidavit To The Company For Time Gap in JoiningDocumento2 pagineSample Affidavit To The Company For Time Gap in Joiningwww.aletterformat.com100% (1)

- Syllabus. Legal Philo 2021-2022Documento4 pagineSyllabus. Legal Philo 2021-2022JCapskyNessuna valutazione finora

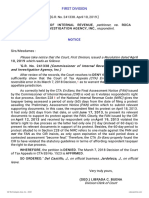

- Roca V CIRDocumento2 pagineRoca V CIRJemima Rachel CruzNessuna valutazione finora

- Harmony and Brothers and Sisters ForeverDocumento11 pagineHarmony and Brothers and Sisters ForeverJCapskyNessuna valutazione finora

- R S CPC: Epresentative Uits UnderDocumento18 pagineR S CPC: Epresentative Uits UnderektaNessuna valutazione finora

- FINALS Case Digests CompilationDocumento154 pagineFINALS Case Digests Compilationviva_3388% (8)

- EASA Air OPS Regulation 965/2012 10/2019Documento1.764 pagineEASA Air OPS Regulation 965/2012 10/2019aviaqualNessuna valutazione finora

- ConfessionsDocumento100 pagineConfessionsLameck80% (5)

- Pacific Timber Export Corporation Vs CADocumento1 paginaPacific Timber Export Corporation Vs CAZoe Velasco100% (1)

- A.M. No. 10-3-10-SC RULES OF PROCEDURE For IP Cases PDFDocumento43 pagineA.M. No. 10-3-10-SC RULES OF PROCEDURE For IP Cases PDFNikki MendozaNessuna valutazione finora

- Ltia OrientationDocumento16 pagineLtia OrientationCA T He100% (3)

- 11 ALBANO - Atty Ed Albano - July 8-9, 2017Documento44 pagine11 ALBANO - Atty Ed Albano - July 8-9, 2017JCapskyNessuna valutazione finora

- Pnb-Republic Bank V. NLRC GR No. 117460 January 6, 1997Documento3 paginePnb-Republic Bank V. NLRC GR No. 117460 January 6, 1997compiler123Nessuna valutazione finora

- Pacific Timber v. CADocumento2 paginePacific Timber v. CAkmand_lustregNessuna valutazione finora

- Cpcu 552 TocDocumento3 pagineCpcu 552 Tocshanmuga89Nessuna valutazione finora

- Mayer Steel Pipe Corporation Vs Court of AppealsDocumento3 pagineMayer Steel Pipe Corporation Vs Court of AppealsIhon BaldadoNessuna valutazione finora

- Lim V Sunlife G.R. No. L-15774 November 29, 1920: I. PolicyDocumento5 pagineLim V Sunlife G.R. No. L-15774 November 29, 1920: I. PolicyNFNLNessuna valutazione finora

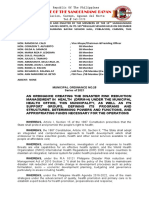

- Municipal Ordinance No. 25-2021 DRRM-HDocumento5 pagineMunicipal Ordinance No. 25-2021 DRRM-HJason Lape0% (1)

- Pacific Timber Export Corporation vs. CADocumento2 paginePacific Timber Export Corporation vs. CAMarry LasherasNessuna valutazione finora

- DOJ Circular No. 70Documento3 pagineDOJ Circular No. 70Sharmen Dizon Gallenero100% (1)

- Digest - Pacific Timber v. CADocumento2 pagineDigest - Pacific Timber v. CAAleli GuintoNessuna valutazione finora

- 19 - Pacific Timber Export Corp vs. CA G.R. L-38613Documento4 pagine19 - Pacific Timber Export Corp vs. CA G.R. L-38613Lemuel Montes Jr.Nessuna valutazione finora

- Pacific Timber Export Corp Vs CADocumento2 paginePacific Timber Export Corp Vs CAthornapple25Nessuna valutazione finora

- 136574-1982-Pacific Timber Export Corp. v. Court Of20160306-3896-2qktesDocumento7 pagine136574-1982-Pacific Timber Export Corp. v. Court Of20160306-3896-2qktesKim RoxasNessuna valutazione finora

- Pacific Timber Vs CADocumento5 paginePacific Timber Vs CAShiena Lou B. Amodia-RabacalNessuna valutazione finora

- CovernoteDocumento4 pagineCovernoteHelen Grace M. BautistaNessuna valutazione finora

- Pacific Timber Export Corp Vs Court of Appeals Et Al 112 SCRA 199 PDFDocumento5 paginePacific Timber Export Corp Vs Court of Appeals Et Al 112 SCRA 199 PDFemmaniago08Nessuna valutazione finora

- Pacific Timber Export Corporation v. Court of AppealsDocumento3 paginePacific Timber Export Corporation v. Court of AppealsJUAN REINO CABITACNessuna valutazione finora

- 4.the Policy Insurance FULLTXTDocumento27 pagine4.the Policy Insurance FULLTXTHyuga NejiNessuna valutazione finora

- Pacific Timber Export Corporations Case GR 38613Documento4 paginePacific Timber Export Corporations Case GR 38613Alvin-Evelyn GuloyNessuna valutazione finora

- Chapter 6a Insurance CaseDocumento35 pagineChapter 6a Insurance CaseAliyah SandersNessuna valutazione finora

- Pacific Timber vs. CADocumento2 paginePacific Timber vs. CAAiza GiltendezNessuna valutazione finora

- Insurance Batch3Documento8 pagineInsurance Batch3asdfghjkattNessuna valutazione finora

- Pacific Timber Export vs. CADocumento2 paginePacific Timber Export vs. CALaika CorralNessuna valutazione finora

- Pacific Timber Export Corporation vs. Court of AppealsDocumento2 paginePacific Timber Export Corporation vs. Court of Appealsmario navalezNessuna valutazione finora

- Pacific vs. CA (Cover Note)Documento14 paginePacific vs. CA (Cover Note)SERVEN GAMINGNessuna valutazione finora

- Week 2 CasesDocumento26 pagineWeek 2 CasesSachieCasimiroNessuna valutazione finora

- Pacific Timber V CA FactsDocumento15 paginePacific Timber V CA FactsNivla XolerNessuna valutazione finora

- Supreme Court: de Castro, J.Documento8 pagineSupreme Court: de Castro, J.nikkimaxinevaldezNessuna valutazione finora

- Pacific Timber Export v. CADocumento2 paginePacific Timber Export v. CANico HilarioNessuna valutazione finora

- Insurance 2Documento15 pagineInsurance 2Nicole Ann Delos ReyesNessuna valutazione finora

- G.R. No. 76145 June 30, 1987 CATHAY INSURANCE CO., Petitioner, Hon. Court of Appeals, and Remington Industrial Sales Corporation, Respondents. Paras, J.Documento19 pagineG.R. No. 76145 June 30, 1987 CATHAY INSURANCE CO., Petitioner, Hon. Court of Appeals, and Remington Industrial Sales Corporation, Respondents. Paras, J.jimart10Nessuna valutazione finora

- United States Court of Appeals Second Circuit.: No. 356. Docket 26837Documento8 pagineUnited States Court of Appeals Second Circuit.: No. 356. Docket 26837Scribd Government DocsNessuna valutazione finora

- G.R. No. 168402 August 6, 2008 Aboitiz Shipping Corporation, Petitioner, Insurance Company of North America, Respondent. Decision REYES, R.T., J.Documento32 pagineG.R. No. 168402 August 6, 2008 Aboitiz Shipping Corporation, Petitioner, Insurance Company of North America, Respondent. Decision REYES, R.T., J.nina armadaNessuna valutazione finora

- Insurance CaseDocumento11 pagineInsurance CaseWEa MaTrizNessuna valutazione finora

- Phil Phoenix Surety Vs Woodworks IncDocumento3 paginePhil Phoenix Surety Vs Woodworks IncJane FrioloNessuna valutazione finora

- Insurance Digests PP 1-3Documento8 pagineInsurance Digests PP 1-3krisipsaloquiturNessuna valutazione finora

- Insurance Case DigestsDocumento11 pagineInsurance Case DigestsviktoriavilloNessuna valutazione finora

- choa-tiek-seng-v-CADocumento12 paginechoa-tiek-seng-v-CADagul JauganNessuna valutazione finora

- Aboitiz V New India G..R. No. 156978 May 2, 2006 Ang Giok Chip V Springfield G.R. No. L-33637 December 31, 1931Documento20 pagineAboitiz V New India G..R. No. 156978 May 2, 2006 Ang Giok Chip V Springfield G.R. No. L-33637 December 31, 1931Jlyne TrlsNessuna valutazione finora

- Lim V Sunlife G.R. No. L-15774 November 29, 1920: I. PolicyDocumento5 pagineLim V Sunlife G.R. No. L-15774 November 29, 1920: I. PolicyNFNLNessuna valutazione finora

- Pacific Timber Export Vs CA, 112 SCRA 199Documento1 paginaPacific Timber Export Vs CA, 112 SCRA 199rengieNessuna valutazione finora

- Choa Tiek Seng Vs CA G.R. No. 84507. March 15, 1990Documento6 pagineChoa Tiek Seng Vs CA G.R. No. 84507. March 15, 1990Lolph ManilaNessuna valutazione finora

- Pacific Timber Export Vs CA, 112 SCRA 199Documento1 paginaPacific Timber Export Vs CA, 112 SCRA 199rengieNessuna valutazione finora

- 1 Aboitiz Shipping v. Insurance Company of AmericaDocumento9 pagine1 Aboitiz Shipping v. Insurance Company of AmericaC SNessuna valutazione finora

- Insurance Cases MidDocumento29 pagineInsurance Cases MidRasmirah BeaumNessuna valutazione finora

- Petitioner VS.: SyllabusDocumento21 paginePetitioner VS.: SyllabusbelleNessuna valutazione finora

- Compania Maritima v. Court of AppealsDocumento8 pagineCompania Maritima v. Court of AppealsChristian VillarNessuna valutazione finora

- Aboitiz V Insurance Company of North America GR168402Documento13 pagineAboitiz V Insurance Company of North America GR168402Jesus Angelo DiosanaNessuna valutazione finora

- Manila Steamship Co - TyDocumento20 pagineManila Steamship Co - TyLester BalagotNessuna valutazione finora

- 124757-1997-Malayan Insurance Corp. v. Court of AppealsDocumento9 pagine124757-1997-Malayan Insurance Corp. v. Court of AppealsVener Angelo MargalloNessuna valutazione finora

- Great Lakes ReinsuranceDocumento4 pagineGreat Lakes ReinsuranceRahel RimonNessuna valutazione finora

- Cases 1Documento4 pagineCases 1Jucca Noreen SalesNessuna valutazione finora

- m3. Oriental Assurance Corporation vs. Court of AppealsDocumento6 paginem3. Oriental Assurance Corporation vs. Court of AppealsBLACK mambaNessuna valutazione finora

- 11 Loadstar Shipping Co. vs. CA, 315 SCRA 339Documento13 pagine11 Loadstar Shipping Co. vs. CA, 315 SCRA 339blessaraynesNessuna valutazione finora

- 13 Mayer Steel V CADocumento3 pagine13 Mayer Steel V CAChescaSeñeresNessuna valutazione finora

- 6 Eastern Shipping LinesDocumento4 pagine6 Eastern Shipping LinesMary Louise R. ConcepcionNessuna valutazione finora

- Roque v. IAC, G.R. No. L 66935, Nov. 11, 1985Documento9 pagineRoque v. IAC, G.R. No. L 66935, Nov. 11, 1985Kharol EdeaNessuna valutazione finora

- 12 Mayer Steel Pipe Corp., Et Al vs. CA, G.R. No. 124050 PDFDocumento8 pagine12 Mayer Steel Pipe Corp., Et Al vs. CA, G.R. No. 124050 PDFpa0l0sNessuna valutazione finora

- Diy ItemsDocumento13 pagineDiy ItemsJCapskyNessuna valutazione finora

- Requirements For Change of NameDocumento1 paginaRequirements For Change of NameJCapskyNessuna valutazione finora

- Affidavit of Non Tax Filing - BlankDocumento1 paginaAffidavit of Non Tax Filing - BlankJCapskyNessuna valutazione finora

- Personal Data Sheet: Filipino Dual Citizenship by Birth by NaturalizationDocumento10 paginePersonal Data Sheet: Filipino Dual Citizenship by Birth by NaturalizationJCapskyNessuna valutazione finora

- Requirements Upang Maging Opisyal Na Kliyente NG PAODocumento2 pagineRequirements Upang Maging Opisyal Na Kliyente NG PAOJCapskyNessuna valutazione finora

- Legal Formalism NotesDocumento3 pagineLegal Formalism NotesJCapskyNessuna valutazione finora

- Danemart Pasalubong Center FlyersDocumento4 pagineDanemart Pasalubong Center FlyersJCapskyNessuna valutazione finora

- Danemart Pasalubong Center FlyersDocumento4 pagineDanemart Pasalubong Center FlyersJCapskyNessuna valutazione finora

- Ham Song 1Documento1 paginaHam Song 1JCapskyNessuna valutazione finora

- Alpha Table NumberDocumento9 pagineAlpha Table NumberJCapskyNessuna valutazione finora

- September 2018: LFX Webinars With Ely, Michael & VinsonDocumento1 paginaSeptember 2018: LFX Webinars With Ely, Michael & VinsonJCapskyNessuna valutazione finora

- Raffy Songs W Remarks UPDATEDDocumento6 pagineRaffy Songs W Remarks UPDATEDJCapskyNessuna valutazione finora

- ReceiptDocumento2 pagineReceiptJCapskyNessuna valutazione finora

- Envelope StickerDocumento2 pagineEnvelope StickerJCapskyNessuna valutazione finora

- Updated Seat Plan 1 - Special Guests 2 - Solis 3 - Sto. Nino Community 4 - Neighbors 5 - Jaise GuestsDocumento3 pagineUpdated Seat Plan 1 - Special Guests 2 - Solis 3 - Sto. Nino Community 4 - Neighbors 5 - Jaise GuestsJCapskyNessuna valutazione finora

- FX Major D1 H4 H1 15M SupportDocumento2 pagineFX Major D1 H4 H1 15M SupportJCapskyNessuna valutazione finora

- Korea TourDocumento3 pagineKorea TourJCapskyNessuna valutazione finora

- 2017 Pds GuidelinesDocumento4 pagine2017 Pds GuidelinesManuel J. Degyan75% (4)

- 16 Kupalourd Rule 30 FinalDocumento3 pagine16 Kupalourd Rule 30 FinalJCapskyNessuna valutazione finora

- Envelope StickerDocumento1 paginaEnvelope StickerJCapskyNessuna valutazione finora

- Table NumbersDocumento1 paginaTable NumbersJCapskyNessuna valutazione finora

- 17 Kupalourd Rule 31 - FinalDocumento2 pagine17 Kupalourd Rule 31 - FinalJCapskyNessuna valutazione finora

- 10 Kupalourd Rule 19 InterventionDocumento1 pagina10 Kupalourd Rule 19 InterventionJCapskyNessuna valutazione finora

- Art. 814 - Ventura Vs VenturaDocumento11 pagineArt. 814 - Ventura Vs VenturaGladys BantilanNessuna valutazione finora

- Affidavit of Loss PRC CardDocumento1 paginaAffidavit of Loss PRC CardMarie Jade Ebol AranetaNessuna valutazione finora

- PerquisitesDocumento6 paginePerquisitesBalajiNessuna valutazione finora

- Security Council - Background GuideDocumento33 pagineSecurity Council - Background GuideRomeMUN2013Nessuna valutazione finora

- Stern vs. Levine & City of Miami BeachDocumento10 pagineStern vs. Levine & City of Miami BeachGrant SternNessuna valutazione finora

- NatureUganda ConstitutionDocumento20 pagineNatureUganda ConstitutionAhaisibwe GeofreyNessuna valutazione finora

- MABX 2015 Buyers GuideDocumento140 pagineMABX 2015 Buyers Guidemabx_PANessuna valutazione finora

- Government Laws and Regulations of Compensation, Incentives and BenefitsDocumento33 pagineGovernment Laws and Regulations of Compensation, Incentives and BenefitsJacobfranNessuna valutazione finora

- BatmanDocumento3 pagineBatmanFeaona MoiraNessuna valutazione finora

- Bank CertificateDocumento1 paginaBank CertificateUCO BANKNessuna valutazione finora

- PDS Word 2022 PrintDocumento4 paginePDS Word 2022 PrintMark Cesar VillanuevaNessuna valutazione finora

- BC AttestationDocumento1 paginaBC AttestationEmmerson MoralesNessuna valutazione finora

- Application For Leave: Republic of The PhilippinesDocumento3 pagineApplication For Leave: Republic of The PhilippinesEva MaeNessuna valutazione finora

- People Vs YumanDocumento4 paginePeople Vs YumanKM MacNessuna valutazione finora

- YOGESH JAIN V SUMESH CHADHADocumento7 pagineYOGESH JAIN V SUMESH CHADHASubrat TripathiNessuna valutazione finora

- 1st Sem 2021 22 Finals ScheduleDocumento5 pagine1st Sem 2021 22 Finals ScheduleRyan ChristianNessuna valutazione finora

- Stephen D. Gardner Chief Counsel: Commercial Law Development ProgramDocumento14 pagineStephen D. Gardner Chief Counsel: Commercial Law Development ProgramxcygonNessuna valutazione finora

- Peoria County Jail Booking Sheet For Oct. 4, 2016Documento7 paginePeoria County Jail Booking Sheet For Oct. 4, 2016Journal Star police documents0% (1)

- Aboitiz Shipping Corporation v. CA (569 SCRA 294) - FULL TEXTDocumento16 pagineAboitiz Shipping Corporation v. CA (569 SCRA 294) - FULL TEXTAdrian Joseph TanNessuna valutazione finora