Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (120)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Charlie Munger ValueWalk PDF Final-1Documento43 pagineCharlie Munger ValueWalk PDF Final-1DhritimanDas90% (21)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Executive Compensation SurveyDocumento22 pagineExecutive Compensation SurveyAbhinav ChowdaryNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Template SAP B1 Pre-Sales Questionnaire V2Documento6 pagineTemplate SAP B1 Pre-Sales Questionnaire V2Ndru Dru50% (2)

- Carrefour S.ADocumento1 paginaCarrefour S.ATeja_Siva_89090% (1)

- Business Planning Insurance 2020 Question Bank SampleDocumento50 pagineBusiness Planning Insurance 2020 Question Bank SampleIsavic Alsina100% (1)

- DI Questions For IBPS Exam 2017Documento534 pagineDI Questions For IBPS Exam 2017Abhishek KrNessuna valutazione finora

- RestAssured For API TestingDocumento25 pagineRestAssured For API Testingpriyanshushekhar50% (2)

- Company Law Last Day Revision Notes CA InterDocumento2 pagineCompany Law Last Day Revision Notes CA InterGANESH KUNJAPPA POOJARI100% (1)

- Enriquez v. Ramos 6 SCRA 219 (1962)Documento8 pagineEnriquez v. Ramos 6 SCRA 219 (1962)Neil bryan MoninioNessuna valutazione finora

- 000 315Documento9 pagine000 315Jameel KhanNessuna valutazione finora

- Message SetDocumento22 pagineMessage SetJameel KhanNessuna valutazione finora

- WMB TroubleshootingDocumento42 pagineWMB TroubleshootingJameel KhanNessuna valutazione finora

- Hero Motocorp: (Herhon)Documento9 pagineHero Motocorp: (Herhon)ayushNessuna valutazione finora

- AO - Annexure A - InvestorDocumento10 pagineAO - Annexure A - InvestorShivam kesarwaniNessuna valutazione finora

- T Homaslloyd Cleantech Infrastructure Fund SICAV Prospectus-2018-05-23Documento108 pagineT Homaslloyd Cleantech Infrastructure Fund SICAV Prospectus-2018-05-23Georgio RomaniNessuna valutazione finora

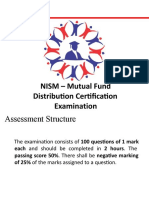

- NISM - Mutual Fund Distribution Certification ExaminationDocumento169 pagineNISM - Mutual Fund Distribution Certification ExaminationPMNessuna valutazione finora

- Underwriting of Shares and Debentures: Class 1Documento26 pagineUnderwriting of Shares and Debentures: Class 1Sneha GopalNessuna valutazione finora

- TB ch07Documento27 pagineTB ch07carolevangelist4657Nessuna valutazione finora

- Company Law ProjectDocumento6 pagineCompany Law ProjectKumar HarshNessuna valutazione finora

- Financial Analysis On GOPAL GROUP Group: Submitted To Prof. D.V RamanaDocumento60 pagineFinancial Analysis On GOPAL GROUP Group: Submitted To Prof. D.V RamanaSumit PandeyNessuna valutazione finora

- Rule: Securities: Securities Offerings Reform Registration Communications, and Offering Processes ModificationDocumento111 pagineRule: Securities: Securities Offerings Reform Registration Communications, and Offering Processes ModificationJustia.com100% (4)

- USAG Financial DocumentsDocumento23 pagineUSAG Financial DocumentsDeadspinNessuna valutazione finora

- Inflation AccountingDocumento4 pagineInflation AccountinganjalikapoorNessuna valutazione finora

- Strategic Buyers Vs Private EquityDocumento20 pagineStrategic Buyers Vs Private EquityGaboNessuna valutazione finora

- FIN300 Homework 3Documento4 pagineFIN300 Homework 3JohnNessuna valutazione finora

- Banking Finance and Insurance: A Report On Financial Analysis of IDBI BankDocumento8 pagineBanking Finance and Insurance: A Report On Financial Analysis of IDBI BankRaven FormourneNessuna valutazione finora

- CG Issues in MNC FinalDocumento16 pagineCG Issues in MNC FinalGuneet SaurabhNessuna valutazione finora

- OtorajaParts PRICE LIST Oct 2022 PDFDocumento14 pagineOtorajaParts PRICE LIST Oct 2022 PDFDedi wahyudiNessuna valutazione finora

- Intermarket Analysis and Asset AllocationDocumento31 pagineIntermarket Analysis and Asset Allocationpderby1Nessuna valutazione finora

- Medrano PRDocumento10 pagineMedrano PRRhealynMarananNessuna valutazione finora

- 19 Circular For Internal Audit Requirement For RTAs and Issuers Having Electronic Connectivity With NSDLDocumento3 pagine19 Circular For Internal Audit Requirement For RTAs and Issuers Having Electronic Connectivity With NSDLnayana savalaNessuna valutazione finora

- Start Up Capital (Start Up Budget) and Its SourcesDocumento19 pagineStart Up Capital (Start Up Budget) and Its SourcesJaymilyn Rodas SantosNessuna valutazione finora

- Statutory ReportsDocumento46 pagineStatutory Reportsguptadeepu905Nessuna valutazione finora

- Equity and DebtDocumento30 pagineEquity and DebtsandyNessuna valutazione finora