Potrebbero piacerti anche

- Sample Cover Letter For Job ApplicationDocumento5 pagineSample Cover Letter For Job ApplicationFierdzz XieeraNessuna valutazione finora

- Business Plan For Sino Cargo Truck: By: Gebeyaw Tebeje KassawDocumento16 pagineBusiness Plan For Sino Cargo Truck: By: Gebeyaw Tebeje KassawSamson Awoke100% (6)

- Freight Broker Business Startup 2023: Step-by-Step Blueprint to Successfully Launch and Grow Your Own Commercial Freight Brokerage Company Using Expert Secrets to Get Up and RunningDa EverandFreight Broker Business Startup 2023: Step-by-Step Blueprint to Successfully Launch and Grow Your Own Commercial Freight Brokerage Company Using Expert Secrets to Get Up and RunningNessuna valutazione finora

- Assignment BBPW3203 Financial Management IIDocumento10 pagineAssignment BBPW3203 Financial Management IIafif120750% (2)

- Industrial ElectronicsDocumento2 pagineIndustrial ElectronicsMartinFS110380% (5)

- Cholamandalam Investment and Finance Company LimitedDocumento11 pagineCholamandalam Investment and Finance Company LimitedAnjana RajeevNessuna valutazione finora

- Hotel Audit PolicyDocumento6 pagineHotel Audit PolicyZiaul Huq50% (2)

- The Entering EsDocumento95 pagineThe Entering Esthomas100% (1)

- Practice Exercises # 2 - CH 14Documento4 paginePractice Exercises # 2 - CH 14Hamna AzeezNessuna valutazione finora

- Case Study Lyons DocumentDocumento3 pagineCase Study Lyons DocumentSandip GumtyaNessuna valutazione finora

- Pag-IBIG Provident Benefits Claim FormDocumento2 paginePag-IBIG Provident Benefits Claim FormCarlo Beltran Valerio0% (2)

- Garrison Lecture Chapter 8Documento92 pagineGarrison Lecture Chapter 8Gelyn CruzNessuna valutazione finora

- A Study On Financial Performance Analysis of The Sundaram Finance LTDDocumento56 pagineA Study On Financial Performance Analysis of The Sundaram Finance LTDSindhuja Venkatapathy88% (8)

- Transport Services Business Plan by Lorato TampiDocumento10 pagineTransport Services Business Plan by Lorato TampiLovlov TampiNessuna valutazione finora

- The Business Guide: Investment and Trade in the UKDa EverandThe Business Guide: Investment and Trade in the UKNessuna valutazione finora

- Transmile Group Assignment - Project Paper SampleDocumento42 pagineTransmile Group Assignment - Project Paper SampleRied-Zall Hasan100% (11)

- Innovation in Shriram Finance ProjectDocumento30 pagineInnovation in Shriram Finance ProjectsugandhirajanNessuna valutazione finora

- Takaful Investment Portfolios: A Study of the Composition of Takaful Funds in the GCC and MalaysiaDa EverandTakaful Investment Portfolios: A Study of the Composition of Takaful Funds in the GCC and MalaysiaNessuna valutazione finora

- Model Bankable Projects - GoatDocumento39 pagineModel Bankable Projects - GoatSuresh Murugesan100% (2)

- Investment CompaniesDocumento6 pagineInvestment CompaniesJared LibiranNessuna valutazione finora

- A Study On Financial Performance Analysis of Sundaram Finance LimitedDocumento56 pagineA Study On Financial Performance Analysis of Sundaram Finance LimitedAnonymous lOz8e6tl0Nessuna valutazione finora

- Disclosure No. 140 2021 Annual Report For Fiscal Year Ended September 30 2020 SEC Form 17 ADocumento153 pagineDisclosure No. 140 2021 Annual Report For Fiscal Year Ended September 30 2020 SEC Form 17 AJan Nicklaus S. BunagNessuna valutazione finora

- L&T FinanceDocumento24 pagineL&T FinanceArpita NagarNessuna valutazione finora

- What Is LeasingDocumento9 pagineWhat Is LeasingHassan KianiNessuna valutazione finora

- About IIFL: IIFL/India Infoline Refer To India Infoline LTD and Its Subsidiaries/ Group CompaniesDocumento52 pagineAbout IIFL: IIFL/India Infoline Refer To India Infoline LTD and Its Subsidiaries/ Group CompaniesHarika AnkamNessuna valutazione finora

- A Report On Credit RatingDocumento29 pagineA Report On Credit RatingShuvo HasanNessuna valutazione finora

- Taxi Investor Summary July 2012lDocumento4 pagineTaxi Investor Summary July 2012lMark John WaiteNessuna valutazione finora

- Company Analysis Accounting For Managers: (An Investment Firm)Documento35 pagineCompany Analysis Accounting For Managers: (An Investment Firm)Arya Mishra100% (1)

- Al Zamin Leasing CorporationDocumento70 pagineAl Zamin Leasing CorporationAqsa MoizNessuna valutazione finora

- Almarai Part B and CDocumento14 pagineAlmarai Part B and CQusai BassamNessuna valutazione finora

- 2006 Annual Report SEC Form 17-A PDFDocumento135 pagine2006 Annual Report SEC Form 17-A PDFJessa LomibaoNessuna valutazione finora

- Trend Analysis FinanceDocumento17 pagineTrend Analysis FinanceNarasimhaPrasadNessuna valutazione finora

- Dividend Policy - Project On Ashok LeylandDocumento15 pagineDividend Policy - Project On Ashok LeylandRuchi MadiyaNessuna valutazione finora

- Benefits To The Public Sector: Course: Authorized Economic Operator Unit 2: AEO Program BenefitsDocumento6 pagineBenefits To The Public Sector: Course: Authorized Economic Operator Unit 2: AEO Program Benefitsjhon jNessuna valutazione finora

- MB0041Documento8 pagineMB0041Gaurang VyasNessuna valutazione finora

- Cholamandalam Investment and Finance Company Limited: 1. IntroductionDocumento13 pagineCholamandalam Investment and Finance Company Limited: 1. Introductiongr8zeeyaNessuna valutazione finora

- Ashok LeylandDocumento12 pagineAshok LeylandvenkatmatsNessuna valutazione finora

- L1 Reporting EnvironmentDocumento41 pagineL1 Reporting EnvironmentAlice LowNessuna valutazione finora

- Case Study: FLC GroupDocumento44 pagineCase Study: FLC GroupPhạm Ngọc Phương AnhNessuna valutazione finora

- Shriram Transport Finance Company LTD, MeghanDocumento26 pagineShriram Transport Finance Company LTD, MeghanAnil Bambule100% (1)

- MB0041-Fin & MGMT AccountingDocumento12 pagineMB0041-Fin & MGMT AccountingRamesh SoniNessuna valutazione finora

- Financial Analysis of Engro Corporation (2013-2010Documento17 pagineFinancial Analysis of Engro Corporation (2013-2010Asad MuhammadNessuna valutazione finora

- A Study On Portfolio Management and AnalysisDocumento12 pagineA Study On Portfolio Management and AnalysisSunny SharmaNessuna valutazione finora

- Freight Car Rental Business Business PlanDocumento14 pagineFreight Car Rental Business Business PlanJustusNessuna valutazione finora

- Dolphin Offshore's History as India's First Underwater Engineering CompanyDocumento12 pagineDolphin Offshore's History as India's First Underwater Engineering CompanyAnjum SamiraNessuna valutazione finora

- Amb Newsletter Screen1 PDFDocumento13 pagineAmb Newsletter Screen1 PDFMark AldissNessuna valutazione finora

- Financial Analysis of PTCLDocumento30 pagineFinancial Analysis of PTCLmeherNessuna valutazione finora

- Analysis of Investment Plans for Sundaram FinanceDocumento78 pagineAnalysis of Investment Plans for Sundaram FinancemanuNessuna valutazione finora

- Cherat-Cement-Company Final Report 2Documento21 pagineCherat-Cement-Company Final Report 2UbaidNessuna valutazione finora

- Annual Report 2010-11-02Documento151 pagineAnnual Report 2010-11-02Harish BhardwajNessuna valutazione finora

- Annual Report 2010-11-02Documento151 pagineAnnual Report 2010-11-02anupraipurNessuna valutazione finora

- TCS 2010 AnalysisDocumento22 pagineTCS 2010 AnalysisDilip KumarNessuna valutazione finora

- Kompella Investment Adviser September 2015 EditionDocumento59 pagineKompella Investment Adviser September 2015 EditionbhaskarjalanNessuna valutazione finora

- Funds Flow Statement ExplainedDocumento35 pagineFunds Flow Statement ExplainedDeepshikha YadavNessuna valutazione finora

- Fundamental Analysis of Telecom SectorDocumento74 pagineFundamental Analysis of Telecom SectorAishwarya Patnekar 807Nessuna valutazione finora

- North South University: "Financial Statement Analysis Techniques For Comparison" Group Name: 330Documento27 pagineNorth South University: "Financial Statement Analysis Techniques For Comparison" Group Name: 330limon islamNessuna valutazione finora

- Results Press Release For December 31, 2016 (Result)Documento10 pagineResults Press Release For December 31, 2016 (Result)Shyam SunderNessuna valutazione finora

- R2003D10581013 Assignment 1 - Finance & Strategic ManagementDocumento10 pagineR2003D10581013 Assignment 1 - Finance & Strategic ManagementMandy Nyaradzo MangomaNessuna valutazione finora

- IPO of SUMMIT ALLIANCE PORT LIMITED (SAPL)Documento30 pagineIPO of SUMMIT ALLIANCE PORT LIMITED (SAPL)Mohammad Asrarul HaqueNessuna valutazione finora

- Solidarity Group's Islamic banking and finance operationsDocumento10 pagineSolidarity Group's Islamic banking and finance operationsKashif DayoNessuna valutazione finora

- Sundaram Finance LTD - Financial Analysis StudyDocumento10 pagineSundaram Finance LTD - Financial Analysis StudyFinance Project ReportsNessuna valutazione finora

- Orix 1Documento11 pagineOrix 1haroonameerNessuna valutazione finora

- OrixDocumento31 pagineOrixharoonameerNessuna valutazione finora

- A. First Metro Investment CorporationDocumento2 pagineA. First Metro Investment CorporationJeth Vigilla NangcaNessuna valutazione finora

- Continuing Reforms to Stimulate Private Sector Investment: A Private Sector Assessment for Solomon IslandsDa EverandContinuing Reforms to Stimulate Private Sector Investment: A Private Sector Assessment for Solomon IslandsNessuna valutazione finora

- Pacific Private Sector Development Initiative: A Decade of Reform: Annual Progress Report 2015-2016Da EverandPacific Private Sector Development Initiative: A Decade of Reform: Annual Progress Report 2015-2016Nessuna valutazione finora

- IPSAS Explained: A Summary of International Public Sector Accounting StandardsDa EverandIPSAS Explained: A Summary of International Public Sector Accounting StandardsNessuna valutazione finora

- Elegent ResumeDocumento2 pagineElegent Resumesudipto royNessuna valutazione finora

- Elegent ResumeDocumento2 pagineElegent Resumesudipto royNessuna valutazione finora

- Daily Closing Sales Lipat Square Bandar Sri Perdana Lahad DatuDocumento2 pagineDaily Closing Sales Lipat Square Bandar Sri Perdana Lahad DatuFierdzz XieeraNessuna valutazione finora

- Daily Closing Sales Lipat Square Bandar Sri Perdana Lahad DatuDocumento2 pagineDaily Closing Sales Lipat Square Bandar Sri Perdana Lahad DatuFierdzz XieeraNessuna valutazione finora

- List of Furnitures Office EquipmentDocumento4 pagineList of Furnitures Office EquipmentFierdzz XieeraNessuna valutazione finora

- Daily Closing Sales Lipat Square Bandar Sri Perdana Lahad DatuDocumento2 pagineDaily Closing Sales Lipat Square Bandar Sri Perdana Lahad DatuFierdzz XieeraNessuna valutazione finora

- Question 1Documento2 pagineQuestion 1Fierdzz XieeraNessuna valutazione finora

- Readme PDFDocumento1 paginaReadme PDFFierdzz XieeraNessuna valutazione finora

- View FileDocumento2 pagineView FileFierdzz XieeraNessuna valutazione finora

- Taxpayer Access Point (TAP)Documento1 paginaTaxpayer Access Point (TAP)Fierdzz XieeraNessuna valutazione finora

- ThreeDocumento6 pagineThreeFierdzz XieeraNessuna valutazione finora

- Responden Oumh2203Documento8 pagineResponden Oumh2203Fierdzz XieeraNessuna valutazione finora

- Vacancy (Bintulu) : Operation Logistic - 1 Post Clerk - 1 PostDocumento1 paginaVacancy (Bintulu) : Operation Logistic - 1 Post Clerk - 1 PostFierdzz XieeraNessuna valutazione finora

- Assignment AnswersDocumento4 pagineAssignment AnswersFierdzz XieeraNessuna valutazione finora

- Assignment Bis Law KamDocumento20 pagineAssignment Bis Law KamFierdzz XieeraNessuna valutazione finora

- 1 Malaysia MakanDocumento2 pagine1 Malaysia MakanFierdzz XieeraNessuna valutazione finora

- Content Oumh2203 2Documento21 pagineContent Oumh2203 2Fierdzz XieeraNessuna valutazione finora

- Real Questionaire RMDocumento6 pagineReal Questionaire RMFierdzz XieeraNessuna valutazione finora

- UM Sabah Labuan Case Study 2 Business StatisticsDocumento1 paginaUM Sabah Labuan Case Study 2 Business StatisticsFierdzz XieeraNessuna valutazione finora

- Shwal Amie Binti Nailie BG10110470 HE19 Financial AccountingDocumento1 paginaShwal Amie Binti Nailie BG10110470 HE19 Financial AccountingFierdzz XieeraNessuna valutazione finora

- Islamic Finance Group AssignmentDocumento1 paginaIslamic Finance Group AssignmentFierdzz XieeraNessuna valutazione finora

- AccountDocumento2 pagineAccountFierdzz XieeraNessuna valutazione finora

- Tate & Lyle (Financial Statement Analysis)Documento30 pagineTate & Lyle (Financial Statement Analysis)Fierdzz XieeraNessuna valutazione finora

- Kamarul Ahmat KamarudinDocumento2 pagineKamarul Ahmat KamarudinFierdzz XieeraNessuna valutazione finora

- Comparing the Strengths of Two Business DealsDocumento6 pagineComparing the Strengths of Two Business DealsFierdzz Xieera100% (1)

- Comparing the Strengths of Two Business DealsDocumento6 pagineComparing the Strengths of Two Business DealsFierdzz Xieera100% (1)

- ReviewDocumento5 pagineReviewFierdzz XieeraNessuna valutazione finora

- ReviewDocumento5 pagineReviewFierdzz XieeraNessuna valutazione finora

- Vision Mission: We Stand For National ValuesDocumento18 pagineVision Mission: We Stand For National ValuesfaisalamynNessuna valutazione finora

- GBI SD ExercisesDocumento40 pagineGBI SD Exercisesdivyajeevan89Nessuna valutazione finora

- Chapter 4 Land Value Determination and Tax Maps 353172 7Documento38 pagineChapter 4 Land Value Determination and Tax Maps 353172 7Andri SuhartoNessuna valutazione finora

- Analisis Pengukuran Tingkat Kesehatan Perbankan Syariah Dengan Menggunakan Metode Camel Pada Pt. Bank Mandiri Syariah TBKDocumento21 pagineAnalisis Pengukuran Tingkat Kesehatan Perbankan Syariah Dengan Menggunakan Metode Camel Pada Pt. Bank Mandiri Syariah TBKKey JannahNessuna valutazione finora

- Branch AccountsDocumento42 pagineBranch AccountsJafari SelemaniNessuna valutazione finora

- Taxation I-P1 - (NOV-08), ICABDocumento2 pagineTaxation I-P1 - (NOV-08), ICABgundapolaNessuna valutazione finora

- Allianz SE (ALVG - De) Understanding Buy-Back CapabilitiesDocumento13 pagineAllianz SE (ALVG - De) Understanding Buy-Back CapabilitiesYang LiNessuna valutazione finora

- GENERAL Rules For The Statement of Cash Flows (Indirect Method)Documento2 pagineGENERAL Rules For The Statement of Cash Flows (Indirect Method)DaggarothNessuna valutazione finora

- FA1Documento289 pagineFA1Abhishek BhatnagarNessuna valutazione finora

- Test Series: October, 2018 Mock Test Paper - 2 Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingDocumento7 pagineTest Series: October, 2018 Mock Test Paper - 2 Intermediate (New) : Group - Ii Paper - 5: Advanced Accountingsahil kumarNessuna valutazione finora

- IA3 Balance SheetDocumento6 pagineIA3 Balance SheetJoebin Corporal LopezNessuna valutazione finora

- Chapter 6-Cost TheoryDocumento28 pagineChapter 6-Cost TheoryFuad HasanNessuna valutazione finora

- Keyman Insurance Policy-White PaperDocumento12 pagineKeyman Insurance Policy-White PaperbeingviswaNessuna valutazione finora

- TM Case Study NotesDocumento3 pagineTM Case Study NoteslylavanesNessuna valutazione finora

- Retirement and Dissolution of Firm Class TestDocumento2 pagineRetirement and Dissolution of Firm Class TestHarish RajputNessuna valutazione finora

- Scanner CAP II Income Tax VATDocumento162 pagineScanner CAP II Income Tax VATEdtech NepalNessuna valutazione finora

- PRR PDFDocumento6 paginePRR PDFv siva kumarNessuna valutazione finora

- VAT and SD Rules 2016 EnglishDocumento59 pagineVAT and SD Rules 2016 EnglishSadia Yasmin100% (3)

- Data Market Inquiry SummaryDocumento24 pagineData Market Inquiry SummaryJanice Healing100% (4)

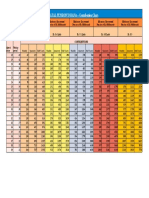

- Atal Pension Yojana contribution chart and minimum guaranteed pension amountsDocumento1 paginaAtal Pension Yojana contribution chart and minimum guaranteed pension amountsG Pavan Kumar100% (1)

- Chapter 2 PQ FMDocumento5 pagineChapter 2 PQ FMRohan SharmaNessuna valutazione finora