Documenti di Didattica

Documenti di Professioni

Documenti di Cultura

IFTA CFTe Syllabus

Caricato da

No NameTitolo originale

Copyright

Formati disponibili

Condividi questo documento

Condividi o incorpora il documento

Hai trovato utile questo documento?

Questo contenuto è inappropriato?

Segnala questo documentoCopyright:

Formati disponibili

IFTA CFTe Syllabus

Caricato da

No NameCopyright:

Formati disponibili

Certified

Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Certified Financial Technician (CFTe)

Syllabus for CFTe Level I & Level II

Document

Change

History

Revision

Date

22

August

2014

25

June

2014

29 May 2014

20 May 2014

Summary

of

Changes

Page

17.

Corrected

the

chapter

numbers

(3-5)

on

reading

material

for

V.

Jeremy

Du

Plessis:

The

Definitive

Guide

to

Point

and

Figure

Page

87.

Added

Appendix

D:

Point

and

Figure

Techniques

(IFTA

Required

CFTe

I

Reading

Material)

Page

17.

Updated

#3:

Required

additional

IFTA

reading

material

(see

Appendices)

Page

18.

Added

to

XI.

Charles

D.

Kirkpatrick,

Julie

R.

Dahlquist:

Technical

Analysis:

The

Complete

Resource

for

Financial

Markets

Technicians:

Chapter

9.

Temporal

Patterns

and

Cycles

and

Chapter

19.

Cycles.

Page

10.

Updated

Outline

of

Topics

Item

21.

Page

17.

Added

VI.

Yukitoshi

Higashino,

MFTA:

Primer

on

ICHIMOKU

(Appendix

E)

(IFTA

Required

CFTe

II

Reading

Material)

Page

17./

Page

18.

Moved

XII.

David

Linton:

Cloud

Charts:

Trading

Success

with

the

Ichimoku

Technique

[Hardcover]

from

IFTA

Required

CFTe

II

Readiing

Material

(Page

17)

to

IFTA

Recommended

(Additional)

CFTe

II

Reading

Material

(Page

18)

Page

95.

Added

Appendix

E:

VI.

Yukitoshi

Higashino,

MFTA:

Primer

on

ICHIMOKU

)

(IFTA

Required

CFTe

II

Reading

Material)

11 March 2014

Page

46:

Added:

Appendix

B:

Breadth

Analysis

(IFTA

Required

CFTe

I

Reading

Material)

Page

20.

Added:

Appendix

A:

The

Elliott

Wave

Principle

(EWP)

(IFTA

Required

CFTe

I

Reading

Material)

Last updated: 22.08.14 11:22 AM

Page 1 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Outline of Topics

1

HISTORY OF TECHNICAL ANALYSIS.............................................................................................................3

PHILOSOPHY OF TECHNICAL ANALYSIS AND MARKETS ...........................................................................3

CHART CONSTRUCTION ...............................................................................................................................3

DOW THEORY................................................................................................................................................3

CONCEPTS OF TREND ...................................................................................................................................4

CLASSICAL BAR CHART PATTERNS..............................................................................................................4

SHORT TERM PRICE PATTERNS ...................................................................................................................5

POINT AND FIGURES CHARTING ..................................................................................................................5

CANDLE STICK CHARTING ............................................................................................................................6

10

ICHIMOKU CHARTS.......................................................................................................................................6

11

OTHER CHARTING METHODS ......................................................................................................................6

12

MARKET PROFILE..........................................................................................................................................6

13

ELLIOTT WAVE THEORY ...............................................................................................................................7

14

BASIC ELEMENTS OF GANN THEORY ..........................................................................................................7

15

BASIC QUANTITATIVE TECHNIQUES............................................................................................................7

16

MOVING AVERAGES......................................................................................................................................8

17

OSCILLATORS AND CONTRARY OPINION ...................................................................................................8

18

RELATIVE STRENGTH ....................................................................................................................................8

19

TIME CYCLES .................................................................................................................................................9

20

VOLUME AND STOCK MARKET INDICATORS..............................................................................................9

21

OTHER TECHNICAL IDEAS .......................................................................................................................... 10

22

TECHNICAL SYSTEMS ................................................................................................................................. 10

23

ACADEMIC FINDINGS ON TA ...................................................................................................................... 10

24

SENTIMENT AND CONTRARY OPINION..................................................................................................... 10

25

BEHAVIORAL FINANCE & INVESTMENT PSYCHOLOGY ............................................................................. 11

26

ETHICS .......................................................................................................................................................... 11

Last updated: 22.08.14 11:22 AM

Page 2 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Outline of Topics (continued)

1

History of Technical Analysis

Early days: Dow, Schabaker, Wykoff

Major Publications

Philosophy of Technical Analysis and Markets

Technical versus Fundamental Forecasting

Technical Approach to Trading and Investing

What is a trend and how are they identified?

Supply and Demand

Assumptions of Technical Analysis

Random Walk Theory, Fat Tails, Proportion of Scale

Market Efficiency, Prediction of the Future

Criticism of Technical Analysis

Financial Markets and the Business Cycles

Chart Construction

Types of Charts: Line, Bar, Candle, Point and Figures

Construction of Charts

Arithmetic or Logarithmic Scale

Volume, Open Interest

Time Frame

Dow Theory

Basic Ideas

Closing Prices and Lines

Primary Trend, Secondary Trend, Minor Trend

Concept of Confirmation

Importance of Volume

The Dow Theorys Defects

Last

updated:

22.08.14

11:22

AM

Page 3 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Outline of Topics (continued)

5

Concepts of Trend

Definition of Trend

Directions of Trend

Support and Resistance

Trendlines and Channels

Major Trendlines

Fan Principles

Strength of a trend

Percentage Retracements

Consolidations and Corrections

Breakouts

Speed Lines

Unconventional Trendlines

Internal Trendlines

Regression

How does psychology impact trends

Classical Bar Chart Patterns

Basics

Psychology and Patterns

Reversal and Continuation Patterns

Patterns and Volume

Patterns and Price Objectives / measured moves

Head and Shoulder Patterns (normal and reversed)

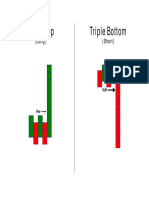

Double Tops and Bottoms

Triple Tops and Bottoms

Rounding tops and bottoms

Saucers and Spikes

Triangles (symmetrical, ascending, descending)

Diamond Tops

Last updated: 22.08.14 11:22 AM

Page 4 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Outline of Topics (continued)

Broadening Formation

Flags and Pennants

Wedge Formation

Rectangle Formation

Gaps

Short Term Price Patterns

Basics and Pattern construction

Gaps

Spike (wide range bar, low range bar)

Dead cat bounce

Island reversal

Reversal Days Run Days

Thrust Days

Two-bar or three-bar patterns

Point and Figures Charting

Basics

Chart Construction: Time and Volume Omitted

Box Count

Box Size and Reversal Filter

Price Patterns: Breakouts, Double Tops, Triple Tops

Support and Resistance

Trendlines

Measuring Techniques and Price Objectives

Point and Figures and Relative Strength

Point and Figures and other Technical Indicators

Last

updated:

22.08.14

11:22

AM

Page 5 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Outline of Topics (continued)

9

Candle Stick Charting

Basics

Chart Construction

Bullish Reversal Patterns (i.e. Hammer, Engulfing Patterns, Harami ...)

Bearish Reversal Patterns (i.e. Hanging Man, Engulfing Pattern, Dark Cloud pattern ...)

Bullish Continuation Patters (i.e. separating Lines, upside Tasuki gap, ...)

Bearish Continuation Patterns (i.e. separating line, three line strike ...)

Candle Patterns and Filters

10

Ichimoku Charts

Basics

Chart and Cloud Construction

Turning Line

Standard Line

Span 1

Span 2

Lagging Line

Interpretation of clouds

11

12

Other

Charting

Methods

(Kagai

Charts,

Renko

Charts

and

Three

Line

Break

Charts

are

included

in

the

CFTe

Level

II

reading

material

section.

The

rest

of

the

reading

material

in

this

section

will

be

added

later.)

Equivolume

Swing charts

Kagi Charts

Renko Charts

Three Line Break Charts

Heikin Ashi Charts

Drummond Geometry

Market Profile

Basics, Construction and graphics

Market Profile organizing Principles

Last updated: 22.08.14 11:22 AM

Page 6 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Outline of Topics (continued)

Range

Development

and

Profile

Patterns:

Normal

day,

Trend

day,

neutral

day,

non

trend

day,

double

distribution

day

TPO

Point of Control

Value Area

13

Elliott Wave Theory

Basics and History

Principles of Wave Counting

Corrective Waves

Rule of Alternation

Channelling

Wave 4

Fibonacci Numbers, Ratios and Retracements

Fibonacci Time Targets

14

Basic Elements of Gann Theory (reading material to be added later)

Basics and History

Gann Fan Lines

Fibonacci numbers and Gann lines

Gann Two-Day Swing Method

15

Basic Quantitative Techniques (reading material to be added later)

Mean, Variance, Skewness

Frequency and Probability

Basic Time Series Concepts

Random Walk Theory

Yield Math Concepts

Time Value of Money / Present Value Concept

Compounding

Last updated: 22.08.14 11:22 AM

Page 7 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Outline of Topics (continued)

Performance Measurement

Test procedures

16

Moving Averages

Different Types of Moving Averages (Simple, Weighted, Exponential, Geometric, Triangular ...)

Moving Average Envelopes

Moving Average crossovers

Bollinger Bands

Bollinger Bands and Bandwidth

Moving Averages and Cycles

Estimating the Length of a Moving Average

Adaptive Moving Average

17

Oscillators and Contrary Opinion

Principles of Oscillation

Oscillator usage and Trend

Measuring Momentum

Rate of Change

Double Moving Averages

Commodity Channel Index

Relative Strength Index

Stochastics

Williams %R

Directional Movement Indicator

Parabolics

Moving Average Convergence/Divergence (indicator and histogram)

18

Relative Strength

Basics

Ratios, Spreads, Rankings,

Relative Strength Levy

Last updated: 22.08.14 11:22 AM

Page 8 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Outline of Topics (continued)

Comparative Relative Strength

Relative Performance

How to Interpret Relative Strength Charts

19

Time Cycles

Basics

Cycle Concept

Amplitude, Length, Phase, Harmonicity, Synchronicity

Detrending

Dominant Cycles

Cycles and Trends

Left and Right Translation

How to Estimate Cycles

Seasonalities

Stock Market Cycles

Fourier Analysis

Maximum Entrophy Spectral Analysis

20

Volume and Stock Market Indicators

Measuring Volume and Open Interest

Volume and Chart Patterns

Volume Signals

On Balance Volume

Volume Accumulator

Measuring Market Breadth

Comparing Market Averages

Advance-Decline Line and Divergence

Different Time frames

McClellan Oscillator

New Highs Versus New Lows

Upside versus Downside Volume

Last updated: 22.08.14 11:22 AM

Page 9 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Outline of Topics (continued)

Arms Index

TRIN and TICK

Equivolume Charting

21

Other technical Ideas (*reading material to be added later)

CoT Data Filtering*

Trend indicators

Volatility Indicators

Range / Momentum Indicators

Cyclical Indicators

Hurst Exponent*

DeMark Indicators = fixed Pattern systems

22

Technical Systems

Construction

Typical elements

Proper testing

Evaluation

Optimisation

Typical systems

23

Academic findings on TA

Testing procedures

Testing objectives

Efficient Market Hypotheses

24

Sentiment and Contrary Opinion

Principle of contrarian Opinion

Crowd Behaviour and the Concept of Contrary Opinion

Investor Sentiment readings

Investor Intelligence Numbers

Last updated: 22.08.14 11:22 AM

Page 10 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Outline of Topics (continued)

Commitments of Trades Report

Net Traders Positions

Open Interest in Options

Put/Call Ratios

Polls

Insiders

Investors Psychology Individual and Group

25

Behavioural Finance & Investment psychology (reading material to be added later)

Prospect Theory

Typical Behavioural Effects

Single Investors Behaviour

26

Ethic (reading material to be added later)

Last updated: 22.08.14 11:22 AM

Page 11 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

CFTe Level I

Reading Material

CORE READING MATERIAL:

I. Edwards, Robert D. and Magee, John, Technical Analysis of Stock Trends, 9th (or current) Edition (2001-2008),

John Magee Inc., Chicago Illinois 2001, ISBN 1-57444-292-9

Chapters:

1. The Technical Approach to Trading and Investing

2. Charts

3. The Dow Theory

4. The Dow Theory in Practice

5. The Dow Theorys Defects

6. Important Reversal Patterns

7. Important Reversal Patterns Continued

8. Important Reversal Patterns The Triangles

9. Important Reversal Patterns Continued

10. Other Reversal Phenomena

11. Consolidation Formations

12. Gaps

13. Support and Resistance

14. Trendlines and Channels

15. Major Trendlines

16. Technical Analysis of Commodity Charts

17. A Summary of Some Concluding Comments

17.2 Advancements in Investment Technology

18. The Tactical Problem

18.1 Strategies and Tactics for the Long-Term Investor

20. The Kind of Stocks we Want: The Speculators View Point

20.1 The Kind of Stocks we Want: The Long-Term Investors View Point

23. Choosing and Managing High-Risk Stocks: Tulip Stocks, Internet Sector and Speculative Frenzies

24. The Probable Moves of Your Stocks

25. Two Touchy Questions

27. Stop Orders

28. What is a Bottom - What is a Top?

29. Trendlines in Action

30. Use of Support and Resistance

Last updated: 22.08.14 11:22 AM

Page 12 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

CFTe Level I (Continued)

Reading Material

33. Tactical Review of Chart Action

34. A Quick Summation of Tactical Methods

36. Automated Trendlines: The Moving Average

38. Balanced and Diversified

39. Trial and Error

40. How Much Capital to Use in Trading

41. Application of Capital in Practice

42. Portfolio Risk Management

43. Stick to Your Guns

II. Murphy, John J.: Technical Analysis of the Financial Markets, New York Institute of Finance, New York, NY,

1999, ISBN 0-7352-0066-1

Chapters:

1. Philosophy of Technical Analysis

2. Dow Theory

3. Chart Construction

4. Basic Concepts of Trend

7. Volume and Open Interest

14. Time Cycles

III. Pring, Martin J.: Technical Analysis Explained, 4th (or current) Edition, McGraw Hill Book Company, New York,

NY, 2001, ISBN 0-07-138193-7

Chapters:

2. Financial Markets and the Business Cycle

4. Typical Parameters for Intermediate Trends

12. Individual Momentum Indicators II

16. The Concept of Relative Strength

18. Price: The Major Averages

20. Time: Longer-Term Cycles

22. General Principles

26. Sentiment Indicators

Last updated: 22.08.14 11:22 AM

Page 13 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

CFTe Level I (Continued)

Reading Material

IV.

Le

Beau

Charles,

Lucas

David:

Technical

Traders

Guide

to

Computer

Analysis

of

the

Futures

Market

Chapters:

1.

System

Building

2.

Technical

Studies

4.

Day

Trading

V.

Nison

Steve:

Candlestick

Charting

Techniques,

Second

Edition

Chapters:

1.

Introduction

2.

A

historical

background

3.

Constructing

the

candlestick

lines

4.

Reversal

patterns

5.

Stars

6.

More

Reversal

Patterns

7.

Continuation

Patterns

8.

The

Magic

Doji

9.

Putting

it

all

Together

VI.

Du

Plessis

Jeremy:

The

Definitive

Guide

to

Point

and

Figure

Chapters:

1.

Introduction

to

Point

and

Figure

Charts

2.

Characteristics

and

Construction

3.

Understanding

Point

and

Figure

Charts

4.

Projecting

Price

Targets

5.

Analysing

Point

and

Figure

Charts

Last updated: 22.08.14 11:22 AM

Page 14 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

CFTe Level I (Continued)

Reading Material

Required additional IFTA reading material (see Appendices):

1. Elliott Wave Theory (Appendix A)

2. Breadth Indicators (Appendix B)

3. Time Cycles Analysis (Appendix C: additional reading material to be added. Note: The questions on the

exam for this topic will be pulled from Murphy, John J. recommended reading listed above. )

4. Point and Figure Techniques (Appendix D)

RECOMMEDED (ADDITIONAL) READING:

VII: Elder, Alexander Dr.: Trading for a Living, Psychology, Trading Tactics, Money Management

Chapters:

1. Individual Psychology

2. Mass Psychology

3. Classical Chart Analysis

4. Computerized Technical Analysis

5. The Neglected Essentials

6. Stock Market Indicators

7. Psychological Indicators

10. Risk Management

Last updated: 22.08.14 11:22 AM

Page 15 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

CFTe Level II

Reading Material

Core Readings

I. Edwards, Robert and Magee, John, Technical Analysis of Stock Trends, 9th Edition

II. Martin J. Pring: Technical Analysis Explained

Chapters:

1. The Market Cycle model

2. Financial Markets and the Business Cycle

16. The concept of Relative Strength

18. Price: The Major Averages

19 Price: Group Rotation

20. Time: Longer-Term Cycles

III. Le Beau Charles, Lucas David: Technical Traders Guide to Computer Analysis of the Futures Market

Chapters:

1. System Building

2. Technical Studies

4. Day Trading

IV. Steve Nison: Beyond Candlesticks: New Japanese Charting Techniques Revealed (Wiley Finance, Nov 10,

1994)

Chapters:

2. The Basics

3. Patterns

4. Candles and the Overall Technical Picture

5. How the Japanese use Moving Averages

6. Three-Line Break Charts

7. Renko Charts

8. Kagi Charts

Last updated: 22.08.14 11:22 AM

Page 16 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

CFTe Level II (Continued)

Reading Material

V. Jeremy Du Plessis: The Definitive Guide to Point and Figure

Chapters:

1. Introduction to Point and Figure Charts

2. Characteristics and Construction

3. Understanding Point and Figure Charts

4. Projecting Price Targets

5. Analysing Point and Figure Charts

VI. Yukitoshi Higashino, MFTA: Primer on ICHIMOKU (Appendix E)

VII. J. Peter Steidlmayer and Steven B. Hawkins: SteidlMayer On Markets. Trading with Market Profile. Second

Editon

Chapters:

6. Understanding Market Profile

7. Liquidity Data Bank, On Floor information, and Volume @ Time

8. The Steidlmayer Theory of Markets

9. The Steidlmayer Distribution

10. The You

11. Anatomy of a trade

12. Profile of a Successful Trader

13. Trading, Technology, and the Future

VIII. Howard B. Bandy: Quantitative Trading Systems, Practical Methods for Design, Testing, and Validation

IX. Brian Millard: Future Trends from Past Cycles

Chapters:

3. How Prices Move (I)

4. How Prices Move (II)

6. Cycles and the Market

8. Properties of Moving Averages

9. Averages as Proxies for Trends

10. Trend Turning Points (I)

11. Trend Turning Points (II)

Last updated: 22.08.14 11:22 AM

Page 17 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

12.

Trend

Turning

Points

(III)

13.

Cycles

and

Sum

of

Cycles

14.

Bringing

it

all

Together

CFTe Level II (Continued)

Reading Material

X.

A.J.

Frost,

Robert

R.

Prechter:

Elliott

Wave

Principle:

Key

To

Market

Behavior

Chapters:

1.

The

Broad

Concept

2.

Guidelines

of

the

Wave

Formation

3.

Historical

and

Mathematical

Background

of

the

Wave

Principle

4.

Ratio

Analysis

and

Fibonacci

Time

Sequence.

XI.

Charles

D.

Kirkpatrick,

Julie

R.

Dahlquist:

Technical

Analysis:

The

Complete

Resource

for

Financial

Markets

Technicians

Chapters:

3.

History

of

Technical

Analysis

4.

The

Technical

Analysis

Controversy

5.

An

overview

of

Markets

7.

Sentiment

8.

Measuring

Market

Strength

9.

Temporal

Patterns

and

Cycles

10.

Flow

of

Funds

13.

Breakouts,

Stops,

and

Retracements

18.

Confirmation

19.

Cycles

21.

Selection

of

Markets

and

Issues:

Trading

and

Investing

22.

System

Testing

and

Management

Last updated: 22.08.14 11:22 AM

Page 18 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

CFTe Level II (Continued)

Reading Material

RECOMMEDED (ADDITIONAL) READING:

XII. David Linton: Cloud Charts: Trading Success with the Ichimoku Technique [Hardcover]

Chapters:

8 . Cloud Chart Construction

9. Interpreting Cloud Charts

10. Multiple Time Frame Analysis

11. Japanese Patterns Techniques

12. Clouds Charts with other techniques

13. Ichimoku indicator techniques

14. Back-testing and Cloud Trading Strategies

15. Cloud Market Breadth analysis

16. Conclusion

Notice to CFTe II Candidates: IFTA will supply additional reading material for the CFTe II on: Quantitative

Analysis, and Behavioral Finance. This material, along with reading material highlighted above (if applicable),

will be posted in the Appendices by 30 June 2014.

Last updated: 22.08.14 11:22 AM

Page 19 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Appendix A

The Elliott Wave Principle (EWP)

(IFTA Required CFTe I Reading Material)

Mohamed ElSaiid, CFTe, MFTA

Egyptian Society of Technical Analysts (ESTA)

Introduction

In this chapter, the Elliott Wave Principle is introduced to the candidate. The general form and essential

concepts of the Elliott Wave structureand role, as well as the psychology and characteristics underlying the

theory. Additionally, the chapter explains the relationship of the Elliott Wave Principle with the Dow Theory and

classical approach in technical analysis.

The chapter is partially designed in study guide format, offering various visual organizers, in an effort to help

the reader connect the related concepts offered in the material and ultimately increasing comprehension of the

basic principles of the EWP.

Part One: The Elliott Wave Principle; historical background and basic tenants

The Elliott Wave Principle (EWP) or Elliott Wave Theory (EWT) is a technical analysis approach developed by

Ralph Nelson Elliott (R.N. Elliott) in the early 1900s that was primarily intended to describe or explain the action

of the market index, namely; the Dow Jones Index (DJI).

Prior to his works and findings on the EWP, R. N. Elliott was an accountant working for railways and a

restaurant. During the early 1930sand while recuperating from a severe illness, he became interested in the

Dow Theory. The various development of market phases as viewed via Dow Theory piqued his interest.

Specifically, he became interested in categorizing the time-frames of the observed market trends.

Through his meticulous research, R. N. Elliott measured the movements in the DJI and identified specific

relationships between these movements later termed as waves. The relations between these waves varied

from a size and time-related one, to a structure and role-related one. With respect to wave-role, R. N. Elliott

contended that there were two types of waves; waves that move in the main trend direction, and waves that

move against the main trend direction. R. N. Elliott organized his observations and findings and developed the

EWP. R.N. Elliott initially introduced the EWP through a publication titled The Wave Principle in 1938. This was

followed by a more detailed book; Natures Laws: The Secret of the Universe in 1946, just before his death in

1948.

Over the years since his death, several followers and pioneering practitioners of the EWP continued to promote

the wave principle by offering publications and newsletters to the investors and the financial community. Of

those followers were, Charles Collins, publisher of the book "Wave Principle", Hamilton Bolton, who was

accredited for introducing the EWP to a wide readership in the mid 1900s, and finally A.J. Frost and Robert R.

Prechter who co-authored Elliott Wave Principle in 1978; a book which is regarded by many EW practitioners

to be the best available description and validation of the EWP to date.

Last updated: 22.08.14 11:22 AM

Page 20 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

The general form and basic tenants of the Elliott Wave Principle

The Five Wave Pattern

Elliott Wave patterns take the form of five waves of a specific pattern. Three of these waves (labeled 1, 3

and 5), cause the development of the overall directional movement of prices. They are separated by two

interruptions against the trend direction (labeled 2 and 4) which, in turn, cause the fluctuation that is

naturally observed in the price action. In other words, waves 1, 3 and 5 describe the main direction of the

move, while waves two and four are seen as pauses. Each of these five waves play a critical role in the

construction of the waves and the overall description of the movement.

Figure

1:

the

basic

five

wave

EW

Pattern

sequence

Last updated: 22.08.14 11:22 AM

Page 21 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

The Complete EW Cycle

The EWP contends that the progression of the five-wave pattern completes a single wave of a larger degree

which ultimately builds the directional move. Following this progression, a three wave pattern develops to

partially counteract this directional move. These three waves act as an interruption to the progression and

complete the formation of a single EW cycle, consisting of eight waves.

This idealized complete EW cycle, consists of two fundamentally distinct structures or modes. These two modes

are referred to as the motive mode and the corrective mode. In this idealized cycle, the (five-wave) motive

modes are always denoted by the numbers (1, 2, 3, 4 and 5). Meanwhile, the (three-wave)

corrective modes are always denoted by the letters (A, B, C). The concept of wave modes will be later

discussed in details in part three.

Figure 2: the complete idealized eight wave EW cycle

Last updated: 22.08.14 11:22 AM

Page 22 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Wave degrees

Initially, R.N. Elliott recognized nine different degrees of waves. They ranged from degrees as small as ripples

on an hourly chart to the largest wave degree he could assume existed from the data that was available to him

at the time. Since, as the theory implies, the degree progression in both directions is infinite, both A.J. Frost and

Robert R. Prechter have suggested six additional wave degrees, of which three were of larger degree than the

initial nine, while the remaining three were of lesser degree. Both Frost and Prechter have been accredited for

standardizing the original labeling scheme, initially added by R.N. Elliott. In addition to that, they have

suggested a general-but-more-detailed framework of the various wave degrees with respect to the range of

span or duration of each degree. This addition, suggested that the most adequate or relevant time-frame chart

for each wave degree would appear visibly. This is deemed as a very important aspect in EWP application, as it

represents common grounds for EW practitioners when applying the EWT in practical life; imagine counting a

wave degree without knowing what the minimum and maximum durations of this wave are, as well as what

time-frame charts to use to chart this wave degree.

Table

1:

The

initial

nine-

degree

waves

of

the

EWP

Table

1

depicts

the

nomenclature

of

the

initial

nine

EW

degrees,

with

each

wave

degree

following

a

unique

labeling

process.

The

maximum

and

minimum

durations

as

well

as

the

corresponding

proposed

time-frame

chart

for

each

wave

degree

are

also

offered

as

guidelines

to

aid

in

charting

the

waves.

The

rationale

behind

the

overriding

(5-3)

structure

Last updated: 22.08.14 11:22 AM

Page 23 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

It is consistently observed in all price actions that progression in either direction always takes the form of

fluctuations (meaning that there are actions in the opposite direction as part of the entire move). EWP adds

that since a one-wave occurrence does not allow fluctuation (action in the opposite direction), the minimum

requirement for achieving fluctuation is three waves. Three waves in two opposite directions do not allow

progress. Hence, to achieve a net progress or development in one direction over the other (i.e. the interrupting

three waves), the main trend must contain at least a five-wave structure.

Part Two: Wave personality: characteristics and psychology of the E-Waves

Wave personality offers an in-depth focus on the aspect of crowd psychology and behavior of the market

participants. The EWP attempts to offer a framework that enhances our understanding of the market action

and behavior that was initially introduced and discussed in the classical approach of technical analysis.

The personality of each wave in the Elliott Wave sequence plays an integral part in the reflection of the mass

psychology it embodies. As such, EW Analysts assume that each wave has its own mark or "signature" which

generally reflects the psychology of that phase under observation. Thus, understanding how and why the

waves develop is key to the application of the EWP.

The characteristics which will be described are in reference to the idealized form of the EW cycle previously

presented in figure 2.

Characteristics of Wave(s) 1:

Commonly,

during

the

bottom

(start)

of

waves

1,

the

accompanied

news

is

generally

bad,

the

period

often

exhibits

the

occurrences

of

recession

(during

intermediate

wave

degrees),

or

even

depression

and

war

(during

large

wave

degrees).

At

this

point

and

given

that

the

input

information

on

the

current

economic

situation

does

not

look

good,

fundamental

analysts

continue

to

lower

their

earnings

estimates.

Quite

commonly,

waves

1

are

formed

as

a

part

of

the

bottoming

phase

or

more

generally,

during

periods

of

disbelief

and

thus,

tend

to

demonstrate

deeper

corrective

movement

in

wave

2.

Wave

1,

the

rebound

from

a

preceding

bear

trend,

is

constructive

and

offers

a

more

structured

rebound

from

undervalued

price

levels.

This

move

often

displays

a

subtle

increase

in

volume

and

is

relatively

supported

by

market

breadth.

The

short

interest

level

peaks

as

the

majority

of

market

participants

believe

that

the

overall

trend

is

to

the

downside.

Investors

view

the

rally

as

a

last

chance

to

sell

and

get

out.

When

waves

1

rise

from

either

large

bases

formed

by

the

previous

correction,

or

from

extreme

compression.

They

appear

as

dynamic

and

dramatic,

and

the

result

is

that

only

moderate

retraced

is

seen

in

wave

2.

Last updated: 22.08.14 11:22 AM

Page 24 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Characteristics of Wave(s) 2:

Waves

2

act

so

as

to

interrupt

the

progress

and

the

directional

move

of

prices.

They

tend

to

heavily

retrace

(but

not

extend

beyond)

wave

1,

especially,

since

they

themselves

occur

mostly

during

the

periods

of

disbelief,

prior

to

the

market-up

phase.

More

often

than

not,

news

and

fundamentals

tend

to

be

worse

during

the

end

(bottom)

of

wave

2

when

compared

to

the

beginning

(bottom)

of

wave

1.

Systematically,

during

wave

2,

investors

are

convinced

that

the

bear

market

is

proceeding

once

more

following

the

termination

of

wave

1,

or

what

they

had

perceived

to

be

another

counter

trend

rally.

Waves

2

are

often

associated

with

downside

non-confirmations.

This

usually

takes

the

shape

of

a

weakening

downside

momentum

and

breadth.

Adding

to

this,

waves

2

are

often

accompanied

by

low

volume

and

volatility,

indicating

a

drying

up

of

selling

pressure.

It

is

not

uncommon

for

waves

2

to

take

more

time

in

formation

compared

to

their

preceding

waves

1.

Characteristics of Wave(s) 3:

Waves

3

are

strong

and

broad;

the

trend

at

this

point

is

unmistakable.

Waves

3

occur

and

are

confirmed

during

the

start

of

what

the

classic

approach

highlight

as

the

mark-up

phase.

Turnaround

fundamentals

stories

begin

to

flow

in

the

financial

arena,

causing

an

investor

confidence

re-build.

Waves

3

usually

generate

the

greatest

volume

and

price

movement,

as

they

most

often

extended

beyond

their

normal

limits,

with

respect

to

both

time

and

distance.

During

waves

3,

successful

classical

pattern-breakouts

are

commonly

observed;

multi-continuation

gaps,

volume

expansions,

exceptional

breadth

(since

almost

all

share

prices

and

market

sectors

participate),

as

well

as

major

Dow

Theory

trend

confirmations

and

runaway

price

movement,

which

create

large

gains

in

the

market,

depending

on

the

wave

degree.

Corrections

in

waves

3

are

usually

weak

and

short-lived

as

those

who

bet

on

buying

pull-backs

suffer

the

likelihood

of

missing

the

move.

Characteristics of Wave(s) 4:

In

principle,

the

occurrence

of

wave

4

implies

that

the

best

part

of

the

growth

phase

which

was

evident

in

wave

3

has

ended.

Last updated: 22.08.14 11:22 AM

Page 25 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

More

often

than

not,

waves

4

appear

as

a

form

of

a

sideways

interruption.

They

develop

as

part

of

the

building

of

a

base

for

the

final

fifth

wave

move.

In

part,

wave

4

is

seen

as

the

public

participation

phase

as

termed

by

the

classical

approach

(Dow

Theory).

Lagging

stocks

build

their

tops

and

begin

declining

during

this

wave,

since

only

the

strength

of

wave

3

is

thought

to

have

pulled

them

along

for

the

upside

participation.

This

initial

deterioration

in

the

market

sets

the

stage

for

breadth

divergences,

non-confirmations

and

subtle

signs

of

weakness

during

the

fifth

wave.

Characteristics of Wave(s) 5:

Specifically,

in

stocks,

waves

5

are

always

less

dynamic

than

waves

3

in

terms

of

breadth.

With

the

exception

of

fifth

wave

extensions

(which

will

be

discussed

in

part

three),

they

usually

display

a

weaker

momentum

as

well.

As

a

general

feature,

volumes

in

waves

5

tend

to

be

less

when

compared

to

wave

3

volumes.

During

advancing

waves

5,

optimism

runs

extremely

high

as

further

public

participation

emerges,

despite

a

narrowing

of

breadth.

Nevertheless,

market

action

does

improve

relative

to

prior

corrective

wave

rallies.

Commonly,

during

the

top

(end)

of

wave

5,

the

accompanied

news

is

positive,

implying

that

prosperity

and

peace

are

guaranteed

forever

as

arrogant

complacency

becomes

evident

in

the

financial

community

and

financial

news.

Characteristics of Wave(s) A:

During

"A"

waves

of

bear

markets;

the

investment

world

is

generally

convinced

that

this

reaction

is

just

a

pullback

pursuant

to

the

next

leg

of

advance.

The

public

surges

to

the

buy

side

despite

the

first

valid

technically

damaging

cracks

in

trend

patterns

of

individual

stocks.

The

"A"

waves

set

the

tone

for

the

waves

that

follow.

A

five-wave

A

indicates

a

start

of

a

directional

or

trending

mode,

while

a

three-wave

A

indicates

that

a

flat

or

sideways

mode

will

likely

follow.

Characteristics of Wave(s) B:

"B"

waves

are

phonies.

They

are

sucker

plays,

bull

traps,

speculators'

paradise,

orgies

of

oddlotter

mentality

or

expressions

of

dumb

institutional

complacency

(or

both).

They

are

often

accompanied

by

an

emotional

advance

of

narrow

list

of

stocks,

which

would

be

evident

through

non-confirming

signs

of

TA-breadth

and

momentum

indications.

Last updated: 22.08.14 11:22 AM

Page 26 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

B

waves

are

often

unconfirmed

by

all/broader

market

indices

and

are

almost

always

expected

to

be

completely

retraced

by

the

following

wave

C.

Characteristics of Wave(s) C:

"C"

waves

inherit

most

of

the

characteristics

and

properties

of

third

waves

in

the

sense

that

they

are

persistent

and

broad.

In

the

case

of

bearish

"C"

waves:

o They

are

usually

devastating

in

their

destruction.

o There

is

virtually

no

place

to

hide

except

cash.

o The

false

impression

that

the

bull

trend

is

back

on

track

which

was

held

throughout

its

preceding

waves

A

and

B

tend

to

fade

away,

as

fear

and

occasionally

multiple

panic

phases

take

over.

o Fundamentals

ultimately

collapse

in

response

of

the

market

action.

In

the

case

of

bullish

"C"

waves:

o They

are

constructive

and

often

render

sizable

gains

or

returns

in

waves

of

larger

degrees.

o They

usually

give

a

fake

indication

that

the

bull

trend

is

back

to

stay.

Last updated: 22.08.14 11:22 AM

Page 27 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Part Three: Aspects and structure of the Elliott Wave Principle

Figure 3: Modal (structure) map of the EWP

Last updated: 22.08.14 11:22 AM

Page 28 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

The EWP is comprised of three key aspects, namely; pattern, ratio and time.

Pattern:

The aspect of pattern (or structure) is regarded as the most important one of the three aspects. This aspect

describes and categorizes the various structures of the underlying waves, which ultimately add up to form a

larger hierarchy of structure.

Ratio:

The aspect of ratio describes the relationship between the lengths of the waves of same and/or different

degrees.

Time:

The aspect of time describes the relationship between the durations of the E-waves and E-cycles of same and/or

different degrees.

In this chapter, we will focus exclusively on the aspect of pattern (or structure).

Last updated: 22.08.14 11:22 AM

Page 29 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Wave Function (role)

According to the EWP, each wave has a role or function. This function is determined only by the relationship of

that wave to the wave of one larger degree. As such, when a wave is termed as actionary, this means that this

wave is responsible for the progression and development of the wave of one larger degree. Accordingly, this

wave moves in the same direction and helps in building the wave of one larger degree. Conversely, when a

wave is termed as reactionary, this means that this wave is responsible for the interruption and regression of

the wave of one larger degree. Accordingly, this wave moves in the opposite direction and partially tears down

the progress of the wave of one larger degree.

Figure 4: Wave function

Wave Mode (structure)

In

addition

to

the

wave

function,

R.N.

Elliott

identified

and

differentiated

between

two

fundamental

types

of

waves

with

respect

to

their

shape

or

structure,

which

he

referred

to

as

the

mode.

With

respect

to

wave

structure

or

mode,

R.N.

Elliott

categorized

the

waves

into

motive

waves

and

corrective

waves.

It

is

the

fundamental

distinction

between

those

two

that

shapes

the

back

bone

of

the

EWP.

Motive

waves

Definition:

Motive

waves

are

responsible

for

the

progress

and

development

of

the

overriding

trend.

They

must

always

exist

as

a

five-wave

structure

and

adhere

to

the

following

rules:

1. Wave

2

does

not

extend

beyond

the

start

of

wave

1.

2. Wave

4

does

not

extend

beyond

the

start

of

wave

3.

3. Wave

3

always

travels

beyond

wave

1.

4. Wave

3

is

never

the

shortest

of

the

motive

waves

1,

3

and

5.

Last

updated:

22.08.14

11:22

AM

Page 30 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

5. Waves 2 and 4 must be corrective in structure.

These rules define the structure of the motive waves and ensure its purpose--that is the progress and

development of the overriding trend.

It is understood from the EWP that any structure failing to adhere to any one of the above rules is automatically

identified (in mode) as a corrective structure, even if it takes the form of a five-wave structure.

Types and characteristics of motive waves:

There are two different types of motive waves, namely; Impulses (or Impulse waves) and Diagonals (or

Diagonal waves).

Impulses

Impulses are types of motive waves that always exist as a five-wave structure. These five-wave structures must

adhere to the primal rules of the motive waves. In addition to that, the following extra rules are exclusive to

Impulses:

1. End of wave 4 does not overlap with end of wave 1.

2. Waves 1, 3 and 5 of an impulse wave must be motive in structure.

3. Extensions (to be discussed shortly) can never exist in all three waves; 1, 3 and 5 at once.

It is worth noting that waves 3 can only exist as Impulses.

Structural or modal characteristics of impulses:

Extension:

Extensions are defined as--and are primarily the cause of an extra stretch or elongation of the impulse waves

(with respect to time, length or both). Naturally, as a result of this stretch, subdivisions exist in abundance.

Extensions are a very common modal characteristic of impulse waves and generally occur during one of the

three actionary waves (1, 3, and 5) as they develop.

Last updated: 22.08.14 11:22 AM

Page 31 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Figure

5:

Types

of

extensions

in

impulse

waves

of

bull

and

bear

markets

Truncation:

Truncation

is

another

characteristic

of

impulses

in

which

wave

5

fails

to

exceed

the

end

of

wave

3.

In

that

sense,

truncations

only

occur

in

impulse

waves

5,

and

are

generally

perceived

as

a

sign

of

weakness

in

the

market.

Truncations

imply

that

although

the

market

was

able

to

develop

into

a

5-wave

structure,

this

development

was

not

associated

with

enough

momentum

to

drive

the

market

beyond

the

end

of

its

preceding

wave

3.

Moreover,

a

truncation

generally

implies

a

sharp

wave

to

follow

in

the

opposite

direction.

Last updated: 22.08.14 11:22 AM

Page 32 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Figure 6: Bull and Bear market impulse truncations

Diagonals

Diagonals

are

types

of

motive

waves

that

always

form

as

a

five-wave

structure.

Diagonals

must

adhere

to

the

primal

(overriding)

rules

of

the

motive

waves.

However,

these

motive

waves

can

never

exist

as

middle

motive

waves

i.e.

motive

wave

3.

Moreover,

unlike

impulses,

an

overlap

between

waves

1

and

4

is

accepted

and

is

considered

as

a

characteristic

of

such

types

of

motive

waves.

Diagonals

are

identified

as

two

rising

(or

falling)

semi

converging

lines,

or

in

less

common

cases

diverging

lines.

Thus,

it

is

important

not

to

assume

that

this

EW

pattern

will

always

resemble

a

classical

wedge

formation.

Despite

sharing

almost

similar

psychology,

their

structures

are

not

always

identical.

There

are

two

types

of

diagonals,

namely;

Leading

and

Ending

Diagonals.

Leading

Diagonals

As

the

name

implies,

Leading

Diagonals

appear

as

motive

waves

that

initiate

the

build

and

development

of

a

new

trend

(a

larger

degree

wave).

They

can

appear

only

as

wave

1

of

a

five-wave

motive

structure,

or

appear

as

wave

A

of

an

ABC

Zigzag

corrective

development.

Leading

Diagonals

are

five-wave

structures

whereby

waves

1,

3

and

5

are

subdivided

into

five

motive

waves,

while

waves

2

and

4

are

corrective

in

structure.

Last updated: 22.08.14 11:22 AM

Page 33 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Figure 7: Converging and diverging Leading Diagonals

Ending

Diagonals

As

the

name

implies,

Ending

Diagonals

appear

as

motive

waves

that

terminate

the

build

and

development

of

an

existing

trend

(a

larger

degree

wave).

An

Ending

Diagonal

can

appear

only

as

motive

wave

5

or

appear

as

wave

C

of

an

ABC

corrective

development.

Being

a

member

of

the

motive

structures

(or

modes),

the

five

waves

of

the

Ending

Diagonals

strictly

adhere

to

the

primal

(overriding)

rules

of

the

motive

waves.

However,

the

subdivisions

of

some

of

these

five

waves

are

somewhat

different

from

the

subdivisions

of

all

other

types

of

motive

structures.

Each

wave

of

the

five

Ending

Diagonal

waves

is

subdivided

into

three

waves

(i.e.

including

waves

1,

3

and

5).

In

other

words,

all

its

subdivisions

are

corrective

in

structure.

It

is

worth

noting

that

waves

1,

3

and

5

in

Ending

Diagonals

are

corrective

in

structure

and

actionary

in

function

(or

role).

Meanwhile,

waves

2

and

4

are

both

corrective

in

structure

and

reactionary

in

function

(or

role).

Last

updated:

22.08.14

11:22

AM

Page 34 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Figure 8: Converging and diverging Ending Diagonals

Corrective waves

Definition:

Last updated: 22.08.14 11:22 AM

Page 35 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Corrective waves appear in--and are exclusively responsible for all counter trend interruptions. In that sense,

corrective structures primarily function as reactionary waves. However, they may also exist (in special cases) as

actionary waves (for example: during waves 1, 3 and 5 of an ending diagonal). Corrective waves are

primarily structured in the form of three waves or a more complex variation thereof. The fundamental

difference between motive and corrective waves is that the latter will always break one or more of the cardinal

rules of the motive wave. Thus, any five-wave structure that breaks any of the motive wave rules is corrective.

The reason as to why they are called corrective is that being the sole driver for all counter trend interruptions

corrective waves accomplish only a partial retracement, or "correction," of the progress achieved by any

preceding motive wave. As for why corrective waves tend to cause only partial retracement, is that movements

against trends of one larger degree appear as a struggle. This is primarily caused due to the overriding force of

the larger degree trend which prevents counter trend movements to fully develop as motive structures. A

byproduct of this situation is that corrective structures tend to be less identifiable and more varied than their

motive counterparts.

Types and characteristics of corrective waves:

Corrective structures appear in two types, sharp and sideways. Sharp corrective structures are manifested

through Zigzags, while, sideways structures are represented through Flats and Triangles.

Sharp corrective structures:

Zigzags

Zigzags represent the most common form of the EW corrective pattern. They exist as a three-wave structure.

The three waves are denoted by the letters A, B and C respectively. Wave B will never terminate

beyond the start of wave A and wave C will travel beyond the end of wave A.

In zigzags, the function of wave A is actionary because it helps build the wave of one larger degree (either

wave 2 or 4). Meanwhile its structure is motive (can either an impulse or a leading diagonal), thus it is

subdivided into five waves and adheres to the motive wave rules. Wave, B on the other hand acts as a

reactionary wave, since it interrupts the progress of the wave of one larger degree (either wave 2 or 4),

while its structure is corrective. Finally, wave C is actionary because it helps build the wave of one larger

degree (either wave 2 or 4). Meanwhile its structure is motive (can either an impulse or an ending

diagonal), thus it is subdivided into five waves and adheres to the motive wave rules. As such, Zigzags are

commonly known by EW practitioners as 5-3-5s.

Last updated: 22.08.14 11:22 AM

Page 36 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Figure 9: Bull and bear market Zigzags

Sideways

corrective

structures:

In

general,

sideways

corrective

structures

generally

occur

due

to

a

stronger

trend

of

one

larger

degree

as

well

as

a

lack

of

countertrend

pressure,

relative

to

Zigzags.

There

are

two

types

of

sideways

corrective

structures,

namely;

Flats

and

Triangles.

Flats

Flats

represent

another

form

of

the

EW

corrective

pattern,

where

as

the

name

implies

they

represent

a

sideways

transition

to

the

overriding

direction

(unlike

Zigzags).

Similar

to

Zigzags,

they

also

exist

as

a

three-

wave

structure,

where

each

wave

is

labeled

by

the

letters

A,

B

and

C

respectively.

However,

Flats

offers

a

variation

from

Zigzags

in

that

wave

A

does

not

hold

enough

momentum

to

develop

as

a

five

wave

structure

as

does

wave

A

of

a

Zigzag.

Instead,

wave

A

of

a

flat

structure

develops

into

three

waves.

As

a

result,

wave

B

of

a

Flat

structure

does

not

suffer

the

same

pressure

which

causes

it

to

partially

retrace

wave

A

as

does

wave

B

of

a

Zigzag.

Its

worth

noting

that

wave

A

of

a

Flat

structure

is

both

actionary

and

corrective,

wave

B

is

both

reactionary

and

corrective,

and

wave

C

is

actionary

and

motive.

As

such,

Flats

are

commonly

known

as

3-3-5s.

Last updated: 22.08.14 11:22 AM

Page 37 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Types and characteristics of Flats:

Regular Flats

In regular Flats, wave B terminates at or near the start of its preceding wave A, while, wave C terminates

at, near or faintly beyond wave B.

Expanded Flats

Expanded Flats are regarded as the most commonly recurring type of Flat formation. In this type, wave B

terminates beyond the start of its preceding wave A, while, wave C terminates beyond the start of wave

B (i.e. the end of wave A).

Running Flats

Running Flats are rare when compared to the former two Flat types already discussed. In this running Flat,

wave B terminates beyond the start of its preceding wave A (similar to expanded flats). However, wave

C fails to match the length of wave B. It is implied by this formation that the momentum of overriding

trend is significantly strong to the extent that it forces the corrective pattern to tilt in its direction.

Last updated: 22.08.14 11:22 AM

Page 38 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Figure 10: Bull and bear market Flat types

Last updated: 22.08.14 11:22 AM

Page 39 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Triangles

EW Triangles are yet another type of sideways corrective structures. They are similar to EW Flat corrections, in

the sense that they reflect a form of temporary balance of forces (buyers and sellers). This is also synonymous

to the interpretations of the classical approach of sideway corrections. However, unlike the Triangles in the

classical approach, EW Triangles always act as continuation patterns (or wave degrees) to the larger degree

trend or wave.

EW Triangles consist of 5 overlapping waves, in which each wave subdivides into three waves (five threes).

Since they are corrective, they are labeled in letters as follows: (A, B, C, D, and E) respectively.

EW Triangles can be categorized into; Contracting and Expanding Triangles. There are three types of

Contracting Triangles; Symmetrical, Ascending and Descending, while there is only one type of Expanding

Triangles. Expanding Triangles are also referred to as Reverse Symmetrical Triangles. In general, they are

corrective patterns that tend to precede the final move in the direction of the major trend.

Contracting Triangles

In Contracting Triangles:

1.

2.

3.

Wave C never moves beyond the end of wave A.

Wave D never moves beyond the end of wave B.

Wave E never moves beyond the end of wave C.

Expanding

Triangles

In

Expanding

Triangles:

1.

2.

3.

Wave C always move beyond the end of wave A.

Wave D always move beyond the end of wave B.

Wave E always move beyond the end of wave C.

Last updated: 22.08.14 11:22 AM

Page 40 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Figure 11: Bull and bear market EW Triangle types

Last updated: 22.08.14 11:22 AM

Page 41 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Running Triangles:

Running Triangles are a very common case in contracting EW Triangles in which wave B exceeds the start of

wave A.

Figure

11:

Bull

and

bear

market

EW

Running

Triangle

types

Last

updated:

22.08.14

11:22

AM

Page 42 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

One final point with regards to the subject of wave function and wave mode: It is implied from the EWP that

motive structures are always actionary. Whereas, corrective structures are mostly reactionary, but can also be

actionary in role or function.

Part Four: Comparing the EWP to the Dow principle and the classical approach

(relationships and similarities)

According to the Dow Theorys tenants, there are three main trend-frames; the major (primary), the

intermediate and the minor trends. The Dow Theory focuses more specifically on the primary trends. The

theory states that waves or trends have three phases. They are termed as the accumulation phase, the public

participation phase and the distribution phase. The EWP elaborated and expanded on this concept by initially

introducing nine various trend (wave) degrees, each with a specified range of durations as previously presented

in part I.

Followers of the Dow Theory whom were later accredited for developing the classical approach managed to

affirm, complement and expand Dows three phases of the market trend. Some suggested that an idealized

form of a complete bull/bear succession will likely involve six phases. Three of which constitute the bull tranche

of the succession, and are recognized as the accumulation the mark-up and the public participation

phases respectively. In addition, three phases would make up the bear tranche of the succession and are

termed as the distribution, the panic and the discouraged selling phases respectively. Advocates of the

classic approach added that the discouraged selling and accumulation phases (which constitute market

bottoms) occur during a period of disbelief in which the irrational crowd psychology is caught on the wrong

side of the market. Meanwhile, the mark-up and fear driven-major panic phases occur during a period of

belief in which the irrational crowd psychology is caught on the right side of the market. And finally, the

public participation and distribution phases (which constitute market tops) occur during a period of euphoria

and extreme optimism in which the irrational crowd psychology is again caught on the wrong side of the

market.

When trying to relate the concepts offered through the Dow and classic approach to the EWP, we find that the

classic approachs three bull market phases and three bear market phases seems quite compatible to the EWPs

idea of a five wave bull market advance followed by a three wave bear market decline.

Finally, both the Dow Theory and the EWP made reference to volume, breadth and indices confirmations

through their tenants and guidelines respectively. The Dow Theory tenants explained that volume and breadth

act as a confirmation to the sustainability of the overriding trend. While the EWP further emphasized on this

matter and explained the importance of volume, breadth and indices confirmations during advancing motive

waves. While, characterizing corrective and ending waves to be more likely associated with divergences and

non-confirmations from volume, breadth and other market indices.

As such there is little doubt that the EWP was largely influenced by Dow Theory and can be regarded as some

form of extension to the Dow Theory, in which the EWP validates much of Dow Theory and may be regarded as

an extension thereof.

Last updated: 22.08.14 11:22 AM

Page 43 of 124

Certified Financial Technician (CFTe) I & II Syllabus & Reading Material

(For exams taken from 1 October, 2014 onward)

Figure