Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Public Entertainer - TaxDocumento2 paginePublic Entertainer - TaxChong Sin LingNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- IMC Belch and Belch Chapter 1Documento20 pagineIMC Belch and Belch Chapter 1Sarah TaufiqueNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Redseer Consulting Report On Vernacular LanguagesDocumento36 pagineRedseer Consulting Report On Vernacular LanguagesMalavika SivagurunathanNessuna valutazione finora

- Dial v. Procter & Gamble - Purclean Trademark Complaint PDFDocumento38 pagineDial v. Procter & Gamble - Purclean Trademark Complaint PDFMark JaffeNessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Mass Media in Pakistan by Raja KamranDocumento22 pagineMass Media in Pakistan by Raja Kamranwaqasaliwasti100% (12)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Cambridge International Advanced Subsidiary and Advanced LevelDocumento4 pagineCambridge International Advanced Subsidiary and Advanced LevelAsad Aasim AliNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- DEA Production Assistance AgreementsDocumento184 pagineDEA Production Assistance AgreementsSpyCultureNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Satellite TelevisionDocumento2 pagineSatellite TelevisionDorin LunguNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Iptv Content DeliveryDocumento29 pagineIptv Content DeliveryangelpyNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Service Quality and Customer Satisfaction in The Pay TV Industry: A Case Study of Multichoice Zambia LimitedDocumento6 pagineService Quality and Customer Satisfaction in The Pay TV Industry: A Case Study of Multichoice Zambia LimitedNowshin FarhinNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- FTTH Business Guide 2012 V3.0 English PDFDocumento83 pagineFTTH Business Guide 2012 V3.0 English PDFAmr AwadElkairm Abdalla100% (1)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Inform-Entertain-Attract or Die!Documento3 pagineInform-Entertain-Attract or Die!neondawnNessuna valutazione finora

- Rules Arboretum English 2019 1 PDFDocumento4 pagineRules Arboretum English 2019 1 PDFalfNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Bootleg Film Festival Toronto Program 2012Documento32 pagineBootleg Film Festival Toronto Program 2012bootlegfilmfestivalNessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Executive ProducerDocumento3 pagineExecutive Producerapi-289624692Nessuna valutazione finora

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Rajput, Nitish - The Broken Pillars of Democracy (2022, Invincible Publishers) - Libgen - LiDocumento97 pagineRajput, Nitish - The Broken Pillars of Democracy (2022, Invincible Publishers) - Libgen - Libodev563290% (1)

- Introduction of Jio 4G (Data Grid)Documento2 pagineIntroduction of Jio 4G (Data Grid)Vipul GargNessuna valutazione finora

- Notice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsDocumento1 paginaNotice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsJustia.comNessuna valutazione finora

- Hypothesis ProblemsDocumento5 pagineHypothesis ProblemsshukpriNessuna valutazione finora

- PPM Top-Line Radio StatisticsDocumento1 paginaPPM Top-Line Radio StatisticsThe Vancouver SunNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- 6 Present and Future of Marketing Communication in Border RegionsDocumento16 pagine6 Present and Future of Marketing Communication in Border RegionsPtthoai PtthoaiNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Marketing Mix and 4 PS: Understanding How To Position Your Market OfferingDocumento8 pagineThe Marketing Mix and 4 PS: Understanding How To Position Your Market OfferingSabhaya ChiragNessuna valutazione finora

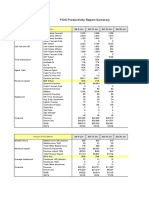

- Telvista Productivity Report - FIOS RollupDocumento28 pagineTelvista Productivity Report - FIOS RollupwabecerraoNessuna valutazione finora

- Service Marketing Unit - 4: Service Delivery and PromotionDocumento9 pagineService Marketing Unit - 4: Service Delivery and PromotionrajeeevaNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Netflix PresentationDocumento29 pagineNetflix PresentationQaziAbubakarNessuna valutazione finora

- The Office S03E01 Gay Witch HuntDocumento26 pagineThe Office S03E01 Gay Witch HuntCaesario TanumihardjaNessuna valutazione finora

- Englis EssayDocumento7 pagineEnglis Essayapi-305189614Nessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (120)

- Research TopicsDocumento50 pagineResearch TopicsDIKITSONessuna valutazione finora

- History of BRTVDocumento3 pagineHistory of BRTVAbdulmalik Grema100% (2)

- Building A Yagi Antenna For UHF - J-Tech Engineering, LTDDocumento15 pagineBuilding A Yagi Antenna For UHF - J-Tech Engineering, LTDRobert GalargaNessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)