Potrebbero piacerti anche

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Mandatory Registration Information: TransactionDocumento2 pagineMandatory Registration Information: TransactionRalphNessuna valutazione finora

- LG Microwave BillDocumento1 paginaLG Microwave BillAman GuptaNessuna valutazione finora

- CLC Byo Treasurers ReportDocumento3 pagineCLC Byo Treasurers ReportAndrew May NcubeNessuna valutazione finora

- John T. Reed - The Biggest Mistakes Real Estate Investors MakeDocumento4 pagineJohn T. Reed - The Biggest Mistakes Real Estate Investors MakeDenis100% (1)

- Soyouwanttobean Economics Journalist?Documento357 pagineSoyouwanttobean Economics Journalist?l 0Nessuna valutazione finora

- Teller Job DescriptionDocumento8 pagineTeller Job DescriptionDianne Bernadeth Cos-agonNessuna valutazione finora

- UntitledDocumento1 paginaUntitledReplacement AccountNessuna valutazione finora

- Sport Odyssey AffiliateDocumento2 pagineSport Odyssey AffiliateKimberly Solomon JavierNessuna valutazione finora

- Notice Inviting Applications (NIA) 2021 - 1Documento174 pagineNotice Inviting Applications (NIA) 2021 - 1Abhishek GunawatNessuna valutazione finora

- Lebanon's Economy An Analysis and Some Recommendations: Esther Baroudy & Hady Farah 20 January 2020Documento17 pagineLebanon's Economy An Analysis and Some Recommendations: Esther Baroudy & Hady Farah 20 January 2020terryhadyNessuna valutazione finora

- Export Import NotesDocumento214 pagineExport Import NotesNikhil Kothavale100% (2)

- Parcel Tracking System For Courier CompaDocumento49 pagineParcel Tracking System For Courier CompaBashir IdrisNessuna valutazione finora

- Bba2 Eco2 Asg 2023 PDFDocumento6 pagineBba2 Eco2 Asg 2023 PDFIzelle Ross GreenNessuna valutazione finora

- Leveraging AI in Electronic CommerceDocumento4 pagineLeveraging AI in Electronic CommerceNaman JainNessuna valutazione finora

- Basic Financial Statement AnalysisDocumento34 pagineBasic Financial Statement AnalysisArpit SidhuNessuna valutazione finora

- ACT1202.Case Study No. 3 Answer SheetDocumento6 pagineACT1202.Case Study No. 3 Answer SheetDonise Ronadel SantosNessuna valutazione finora

- 5 10 pp.62 66Documento6 pagine5 10 pp.62 66timesave240Nessuna valutazione finora

- UnSigned TVSCS PL ApplicationDocumento13 pagineUnSigned TVSCS PL ApplicationArman TamboliNessuna valutazione finora

- Marketing Management Term PaperDocumento18 pagineMarketing Management Term PaperSamiraNessuna valutazione finora

- LIst of CA AgentDocumento12 pagineLIst of CA AgentParikshit SalvepatilNessuna valutazione finora

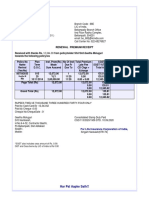

- Renewal Premium Receipt: Har Pal Aapke Sath!!Documento1 paginaRenewal Premium Receipt: Har Pal Aapke Sath!!krishna krishNessuna valutazione finora

- ContractDocumento20 pagineContractgur0% (1)

- Cbe Joining Instruction For Diploma 1 September Intake 2023-2024 Jif2Documento10 pagineCbe Joining Instruction For Diploma 1 September Intake 2023-2024 Jif2Daniel EudesNessuna valutazione finora

- Development in Legal Issues of Corporate Governance in Islamic Finance PDFDocumento25 pagineDevelopment in Legal Issues of Corporate Governance in Islamic Finance PDFDwiki ChyoNessuna valutazione finora

- Puntland Aid ReportDocumento23 paginePuntland Aid ReportkunciilNessuna valutazione finora

- Management Information SytemDocumento7 pagineManagement Information SytemHrishikesh Maheswaran100% (1)

- Characteristics of TQMDocumento5 pagineCharacteristics of TQMJasmin AsinasNessuna valutazione finora

- Sales Manager Sample - Everest GreenDocumento1 paginaSales Manager Sample - Everest GreenH ANessuna valutazione finora

- Lululemon Athletica Case AnalysisDocumento19 pagineLululemon Athletica Case Analysiskuntodarpito100% (2)

- SITXFIN003 Manage Finances and BudgetDocumento9 pagineSITXFIN003 Manage Finances and Budgetimtiaz Khan100% (1)