Potrebbero piacerti anche

- Basic Accounting PrinciplesDocumento3 pagineBasic Accounting PrinciplesSonu JoiyaNessuna valutazione finora

- Bilateral InvestmentTreaties 1959-1999Documento142 pagineBilateral InvestmentTreaties 1959-1999Shaina SmallNessuna valutazione finora

- Direction: Read and Study The Following ConceptsDocumento25 pagineDirection: Read and Study The Following ConceptsChristopher Michael OnaNessuna valutazione finora

- Investor Protection Laws, Accounting and Auditing Around The WorldDocumento40 pagineInvestor Protection Laws, Accounting and Auditing Around The Worlddion qeyenNessuna valutazione finora

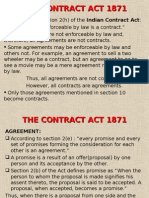

- The Contract Act 1871 (R)Documento55 pagineThe Contract Act 1871 (R)manishparipagar100% (2)

- Factors Shaping Ethics: Culture, Faith, Upbringing & LawsDocumento2 pagineFactors Shaping Ethics: Culture, Faith, Upbringing & LawsAnkit VyasNessuna valutazione finora

- Materiality AssessmentsDocumento14 pagineMateriality AssessmentsRizky Amaliah YahyaNessuna valutazione finora

- THE RIGHT TO BE FORGOTTEN Jeffrey RosenDocumento5 pagineTHE RIGHT TO BE FORGOTTEN Jeffrey RosenChiara de TefféNessuna valutazione finora

- Extenguishment of Obligation Group4Documento112 pagineExtenguishment of Obligation Group4Lheia Micah De CastroNessuna valutazione finora

- Mondragon CorpDocumento52 pagineMondragon CorpimelNessuna valutazione finora

- Disclosure in Financial Statements NotesDocumento25 pagineDisclosure in Financial Statements Noteseknath2000Nessuna valutazione finora

- Acf 465 International Trade Finance 2016Documento365 pagineAcf 465 International Trade Finance 2016John OmarNessuna valutazione finora

- Labour Relations ManualDocumento84 pagineLabour Relations ManualGeorge Baffour AwuahNessuna valutazione finora

- Introduction To Law On CooperativesDocumento4 pagineIntroduction To Law On CooperativesSembrana CampuedNessuna valutazione finora

- Forms of Business: Sole Proprietorship, Partnership, CorporationDocumento4 pagineForms of Business: Sole Proprietorship, Partnership, CorporationLaurever CaloniaNessuna valutazione finora

- Business Law - Chapter 3Documento5 pagineBusiness Law - Chapter 3jessiepitzNessuna valutazione finora

- IAM Constitution 2012Documento202 pagineIAM Constitution 2012LaborUnionNews.comNessuna valutazione finora

- Corporate Governance Definitions Objectives Issues History ChallengesDocumento29 pagineCorporate Governance Definitions Objectives Issues History ChallengesRewardMaturureNessuna valutazione finora

- BankruptcyDocumento18 pagineBankruptcySheila Mae MalesidoNessuna valutazione finora

- Evolution of Financial SystemDocumento12 pagineEvolution of Financial SystemGautam JayasuryaNessuna valutazione finora

- Driving Global Adoption of Procurement Technology, A Cargill ApproachDocumento27 pagineDriving Global Adoption of Procurement Technology, A Cargill ApproachZycusInc100% (2)

- PDR ActDocumento3 paginePDR ActMd Towhidul IslamNessuna valutazione finora

- Investment PolicyDocumento23 pagineInvestment Policyrj5307Nessuna valutazione finora

- Non Marketable Financial AssetsDocumento3 pagineNon Marketable Financial AssetsSnehal JoshiNessuna valutazione finora

- Remedies Lecture 2 - Limiting FactorsDocumento4 pagineRemedies Lecture 2 - Limiting FactorsAdam 'Fez' FerrisNessuna valutazione finora

- Generally Accepted AccountingDocumento23 pagineGenerally Accepted AccountingAbhishek MisraNessuna valutazione finora

- Acetates On Corporate Contract LawDocumento8 pagineAcetates On Corporate Contract LawCarlo EvangelistaNessuna valutazione finora

- Agency Theory Suggests That The Firm Can Be Viewed As A Nexus of ContractsDocumento5 pagineAgency Theory Suggests That The Firm Can Be Viewed As A Nexus of ContractsMilan RathodNessuna valutazione finora

- Financial Services.Documento127 pagineFinancial Services.srn@1234Nessuna valutazione finora

- Assignment Report (2) : Title-Corporate Social ResponsibilityDocumento17 pagineAssignment Report (2) : Title-Corporate Social ResponsibilitykanikaNessuna valutazione finora

- Organizational Chart of LawDocumento5 pagineOrganizational Chart of LawThom Arvin Recardo100% (1)

- InternationalLaw DisposiitonOfSecuriteisDocumento79 pagineInternationalLaw DisposiitonOfSecuriteisravenmailmeNessuna valutazione finora

- MPID Memorandum Final-SDDocumento20 pagineMPID Memorandum Final-SDMoneylife FoundationNessuna valutazione finora

- Functions of Treaty BodiesDocumento10 pagineFunctions of Treaty BodiesSam Sy-HenaresNessuna valutazione finora

- The Law of Tort, Professional Liability and Consumer ProtectionDocumento42 pagineThe Law of Tort, Professional Liability and Consumer ProtectionShirdah AgisteNessuna valutazione finora

- MUTUAL FUNDS INVESTMENT GUIDEDocumento14 pagineMUTUAL FUNDS INVESTMENT GUIDEsonalsachdeva88Nessuna valutazione finora

- Accounting As An Information SystemDocumento14 pagineAccounting As An Information SystemAimee SagastumeNessuna valutazione finora

- Promotion & Formation of A CompanyDocumento41 paginePromotion & Formation of A Companya_mayani01100% (3)

- Company Law: Corporate PersonalityDocumento45 pagineCompany Law: Corporate PersonalityRavi shankarNessuna valutazione finora

- Corruption and Anti-Corruption in Policing-Philosophical and Ethical Issues (PDFDrive)Documento114 pagineCorruption and Anti-Corruption in Policing-Philosophical and Ethical Issues (PDFDrive)Esther WollerNessuna valutazione finora

- Acountancy 10Documento129 pagineAcountancy 10Erfan Bhat0% (1)

- 431Documento15 pagine431ChristieLynnNessuna valutazione finora

- Role of Green Economy in The Context of Indian EconomyDocumento5 pagineRole of Green Economy in The Context of Indian EconomyEditor IJTSRDNessuna valutazione finora

- Account Current Question BankDocumento2 pagineAccount Current Question BankQuestionscastle Friend0% (1)

- Environmental AccountingDocumento26 pagineEnvironmental AccountingAngie Marcela Marulanda Meneses100% (1)

- Africa Banking SurveyDocumento88 pagineAfrica Banking SurveyShailendra DwiwediNessuna valutazione finora

- Debt Instruments: Types, Features & AdvantagesDocumento14 pagineDebt Instruments: Types, Features & AdvantagesAnubhav GoelNessuna valutazione finora

- Objectives of Bank RegulationDocumento4 pagineObjectives of Bank Regulation123456amit100% (1)

- 202116111219989AMLCFTComplianceProgramGuidelines Accountants (Final)Documento106 pagine202116111219989AMLCFTComplianceProgramGuidelines Accountants (Final)Riz DeenNessuna valutazione finora

- Law 05 Company Law 04 Corporate Constitution Notes 20170314 ParabDocumento15 pagineLaw 05 Company Law 04 Corporate Constitution Notes 20170314 ParabarshiNessuna valutazione finora

- Trust Financial ManagementDocumento26 pagineTrust Financial ManagementCalvince Ouma100% (1)

- Thomas Donaldson and Lee Preston - The Stakeholder Theory of The Corporation - Concepts, Evidence, and ImplicationsDocumento27 pagineThomas Donaldson and Lee Preston - The Stakeholder Theory of The Corporation - Concepts, Evidence, and Implicationsrama100% (1)

- International Business and Trade ModuleDocumento19 pagineInternational Business and Trade ModulePrince Isaiah JacobNessuna valutazione finora

- Insurance AccountingDocumento16 pagineInsurance Accountingssp2000Nessuna valutazione finora

- Nyse Jmia 2019Documento81 pagineNyse Jmia 2019nada benraadNessuna valutazione finora

- Capital MaintenanceDocumento49 pagineCapital MaintenanceSamish DhakalNessuna valutazione finora

- Corporate GovernanceDocumento56 pagineCorporate GovernanceHimanshu Gupta100% (1)

- A Handbook on the Ecowas Treaty and Financial InstitutionsDa EverandA Handbook on the Ecowas Treaty and Financial InstitutionsNessuna valutazione finora

- Fiduciary Handbook for Understanding and Selecting Target Date Funds: It's All About the BeneficiariesDa EverandFiduciary Handbook for Understanding and Selecting Target Date Funds: It's All About the BeneficiariesNessuna valutazione finora

- Going for Broke: Insolvency Tools to Support Cross-Border Asset Recovery in Corruption CasesDa EverandGoing for Broke: Insolvency Tools to Support Cross-Border Asset Recovery in Corruption CasesNessuna valutazione finora

- Bangko Sentral NG Pilipinas Coins and Notes - Commemorative CurrencDocumento4 pagineBangko Sentral NG Pilipinas Coins and Notes - Commemorative Currencrafael oviedoNessuna valutazione finora

- Test Transfer IPV To InventoryDocumento17 pagineTest Transfer IPV To Inventorykallol_panda1Nessuna valutazione finora

- Co Act On Loans Accepted & GivenDocumento43 pagineCo Act On Loans Accepted & GivendkdineshNessuna valutazione finora

- CA Final Old Syllabus PDFDocumento114 pagineCA Final Old Syllabus PDFKovvuri Bharadwaj ReddyNessuna valutazione finora

- Currency Wars: Impact On IndiaDocumento7 pagineCurrency Wars: Impact On IndiaAbhishek TalujaNessuna valutazione finora

- BWN JC 110112 (Init)Documento28 pagineBWN JC 110112 (Init)Ana WesselNessuna valutazione finora

- CASFLOWDocumento133 pagineCASFLOWalenNessuna valutazione finora

- Bank Nizwa Summary Prospectus (English)Documento13 pagineBank Nizwa Summary Prospectus (English)Mwangu KibikeNessuna valutazione finora

- Global Currency Reset - Revaluation of Currencies - Historical OverviewDocumento20 pagineGlobal Currency Reset - Revaluation of Currencies - Historical Overviewenerchi111196% (28)

- 12 Swedish Match Philippines Inc. vs. The Treasurer of The City of ManilaDocumento2 pagine12 Swedish Match Philippines Inc. vs. The Treasurer of The City of ManilaIrene Mae GomosNessuna valutazione finora

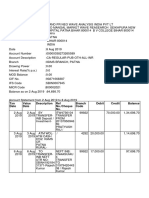

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocumento3 pagineTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaNessuna valutazione finora

- Jaffar and Musa (2013) PDFDocumento10 pagineJaffar and Musa (2013) PDFMohamed FAKHFEKHNessuna valutazione finora

- 2Documento3 pagine2Ruth TenajerosNessuna valutazione finora

- Natural Gas Market of EuropeDocumento124 pagineNatural Gas Market of EuropeSuvam PatelNessuna valutazione finora

- 1.4 Partnership Liquidation - 1Documento4 pagine1.4 Partnership Liquidation - 1Leane Marcoleta100% (2)

- Khet Khet Mein - REALITY SHOWDocumento17 pagineKhet Khet Mein - REALITY SHOWintesharmemonNessuna valutazione finora

- LMGTRAN Negotiable InstrumentsDocumento36 pagineLMGTRAN Negotiable InstrumentsNastassja Marie DelaCruzNessuna valutazione finora

- Aeropostale Checkout ConfirmationDocumento3 pagineAeropostale Checkout ConfirmationBladimilPujOlsChalasNessuna valutazione finora

- M.B.a - Retail ManagementDocumento22 pagineM.B.a - Retail ManagementaarthiNessuna valutazione finora

- DerivativesDocumento344 pagineDerivativesAnonymous j6xVyah1RJ100% (4)

- Republic of Kenya: Kenya Gazette Supplement No. 107 (Acts No.11)Documento26 pagineRepublic of Kenya: Kenya Gazette Supplement No. 107 (Acts No.11)Benard OderoNessuna valutazione finora

- Full FM Module Final Draft 222Documento157 pagineFull FM Module Final Draft 222bikilahussenNessuna valutazione finora

- Asset Liability Management in BanksDocumento8 pagineAsset Liability Management in Bankskpved92Nessuna valutazione finora

- Final Order - Case No 38 of 2014Documento148 pagineFinal Order - Case No 38 of 2014sachinoilNessuna valutazione finora

- Notes and Solutions of The Math of Financial Derivatives Wilmott PDFDocumento224 pagineNotes and Solutions of The Math of Financial Derivatives Wilmott PDFKiers100% (1)

- Assignment (Graded) # 3: InstructionsDocumento4 pagineAssignment (Graded) # 3: Instructionsatifatanvir1758Nessuna valutazione finora

- Accounting Principles Question Paper, Answers and Examiners CommentsDocumento24 pagineAccounting Principles Question Paper, Answers and Examiners CommentsRyanNessuna valutazione finora

- Accounting For Lawyers Notes, 2022Documento114 pagineAccounting For Lawyers Notes, 2022Nelson burchard100% (1)

- Diminishing MusharakahDocumento45 pagineDiminishing MusharakahIbn Bashir Ar-Raisi0% (1)