Potrebbero piacerti anche

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

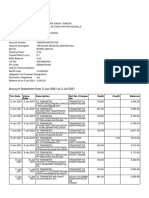

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento8 pagineAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurNessuna valutazione finora

- 2nd Mate OOW For Ratings STC UKDocumento5 pagine2nd Mate OOW For Ratings STC UKFabian MascarenhasNessuna valutazione finora

- OidhvohsDocumento10 pagineOidhvohsDeepak ShastriNessuna valutazione finora

- Bank Reconciliation StatementDocumento40 pagineBank Reconciliation StatementPrashant100% (1)

- 2017 Transpay Service GuideDocumento7 pagine2017 Transpay Service GuideBuddy KertunNessuna valutazione finora

- Visa Fee For AustraliaDocumento11 pagineVisa Fee For AustraliaShaifur RahmanNessuna valutazione finora

- Eft 101Documento12 pagineEft 101Khushbu KothariNessuna valutazione finora

- RBA APU PPT - OJK 16 April 2018 PDFDocumento46 pagineRBA APU PPT - OJK 16 April 2018 PDFBunnyNessuna valutazione finora

- Power of AttorneyDocumento5 paginePower of AttorneyAshokNessuna valutazione finora

- Blue Chip Stocks TipsDocumento16 pagineBlue Chip Stocks TipsPinal MehtaNessuna valutazione finora

- RaresDocumento2 pagineRaresLohanel RaresNessuna valutazione finora

- Current Issues in Istisna & Tijarah (Final)Documento12 pagineCurrent Issues in Istisna & Tijarah (Final)Hasan Irfan Siddiqui100% (1)

- Merger and Acquisition in Bank Sector in IndiaDocumento63 pagineMerger and Acquisition in Bank Sector in IndiaOmkar Chavan0% (1)

- 2551QDocumento3 pagine2551QJerry Bantilan JrNessuna valutazione finora

- Kfs Current AccountsDocumento10 pagineKfs Current Accountsritika sainiNessuna valutazione finora

- Account Activity Generated Through HBL MobileDocumento2 pagineAccount Activity Generated Through HBL MobileAðnan YasinNessuna valutazione finora

- 2.3 Audit AssuranceDocumento27 pagine2.3 Audit AssurancemohedNessuna valutazione finora

- AICPA - Develops Standards For Audits ofDocumento3 pagineAICPA - Develops Standards For Audits ofAngela PaduaNessuna valutazione finora

- Report On HBLDocumento81 pagineReport On HBLSafdar KhanNessuna valutazione finora

- Ross4ppt ch19Documento36 pagineRoss4ppt ch19씨나젬Nessuna valutazione finora

- Aml Kyc NotesDocumento12 pagineAml Kyc Notesabhi_33Nessuna valutazione finora

- Competitive Analysis of Stock Brokers ReligareDocumento92 pagineCompetitive Analysis of Stock Brokers ReligareJaved KhanNessuna valutazione finora

- FIN036 AssignmentDocumento25 pagineFIN036 AssignmentSandeep BholahNessuna valutazione finora

- Apni Shakhsiyat Ki Tameer Kaise Ki JaeDocumento99 pagineApni Shakhsiyat Ki Tameer Kaise Ki JaeMansoorNessuna valutazione finora

- Legendary Chef Makes A Triumphant Return: Pierre KoffmannDocumento36 pagineLegendary Chef Makes A Triumphant Return: Pierre KoffmannCity A.M.Nessuna valutazione finora

- Bank Audit Work PaperDocumento47 pagineBank Audit Work PaperKaushal JhaNessuna valutazione finora

- BANK ACT 1864 (Original) Common-Law RemedyDocumento4 pagineBANK ACT 1864 (Original) Common-Law Remedyin1or100% (1)

- Profile of CompleteBankData in The Pittsburgh Business TimesDocumento1 paginaProfile of CompleteBankData in The Pittsburgh Business TimesNate TobikNessuna valutazione finora

- App Aud - Prelim Exam (Key)Documento16 pagineApp Aud - Prelim Exam (Key)Shaina Kaye De GuzmanNessuna valutazione finora

- TciDocumento53 pagineTciarunzmr007Nessuna valutazione finora