Potrebbero piacerti anche

- AC - H1 Math 2014Documento8 pagineAC - H1 Math 2014ofji4oNessuna valutazione finora

- AJC H2Maths 2012prelim P1 SolutionDocumento6 pagineAJC H2Maths 2012prelim P1 SolutionMelinda BowmanNessuna valutazione finora

- AJC H2Maths 2012prelim P2 QuestionDocumento6 pagineAJC H2Maths 2012prelim P2 Questionofji4oNessuna valutazione finora

- Biology 9648/01: Anderson Junior College Higher 2Documento29 pagineBiology 9648/01: Anderson Junior College Higher 2ofji4oNessuna valutazione finora

- AJC H2Maths 2012prelim P1 QuestionDocumento5 pagineAJC H2Maths 2012prelim P1 Questionofji4oNessuna valutazione finora

- ACJC JC 2 H2 Maths 2012 Year End Exam Question Paper 2Documento6 pagineACJC JC 2 H2 Maths 2012 Year End Exam Question Paper 2ofji4oNessuna valutazione finora

- ACJC JC2 H2 Maths 2012 Year End Exam Solutions Paper 1Documento10 pagineACJC JC2 H2 Maths 2012 Year End Exam Solutions Paper 1ofji4oNessuna valutazione finora

- 2008 CJC H2 Economics Prelim ExamDocumento2 pagine2008 CJC H2 Economics Prelim Examofji4oNessuna valutazione finora

- 2008 HCI H2 Economics Prelim ExamDocumento2 pagine2008 HCI H2 Economics Prelim Examofji4oNessuna valutazione finora

- ACJC JC 2 H2 Maths 2012 Year End Exam Question Paper 1Documento5 pagineACJC JC 2 H2 Maths 2012 Year End Exam Question Paper 1ofji4oNessuna valutazione finora

- AJC Prelim 09 - H2 Paper 1 - AnswersDocumento7 pagineAJC Prelim 09 - H2 Paper 1 - Answersofji4oNessuna valutazione finora

- 2009 ACJC H2 Prelim Essay Q1Documento3 pagine2009 ACJC H2 Prelim Essay Q1ofji4oNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Assignment 1Documento6 pagineAssignment 1Haider Chelsea KhanNessuna valutazione finora

- Period End ClosingDocumento4 paginePeriod End ClosingJose Luis Becerril BurgosNessuna valutazione finora

- Notes To The Financial StatementsDocumento4 pagineNotes To The Financial StatementsROB101512Nessuna valutazione finora

- RyanAir CaseDocumento10 pagineRyanAir Casedian ratnasari100% (13)

- Zahra Et Al. (2003)Documento18 pagineZahra Et Al. (2003)Guilherme MarksNessuna valutazione finora

- Cash and Receivables: ObjectivesDocumento25 pagineCash and Receivables: ObjectivesAlex OuedraogoNessuna valutazione finora

- CFR 1 Quiz 1Documento7 pagineCFR 1 Quiz 1Ahmed SamadNessuna valutazione finora

- UntitledDocumento22 pagineUntitledKajal SahooNessuna valutazione finora

- Cadbury ReportDocumento22 pagineCadbury ReportVania MalikNessuna valutazione finora

- PT ESS1217 - Mapping Report Break LinkDocumento392 paginePT ESS1217 - Mapping Report Break Linkricho naiborhuNessuna valutazione finora

- Profile On Wood Carving For TourismDocumento17 pagineProfile On Wood Carving For Tourismbig johnNessuna valutazione finora

- Afar Exercise 5 PDF FreeDocumento8 pagineAfar Exercise 5 PDF FreeRialeeNessuna valutazione finora

- National Bank of PakistanDocumento44 pagineNational Bank of Pakistanmadnansajid8765Nessuna valutazione finora

- Privatization: "The Transfer of Public Assets, Operations or Activities To Private Enterprise"Documento22 paginePrivatization: "The Transfer of Public Assets, Operations or Activities To Private Enterprise"HebaNessuna valutazione finora

- Đề thi thử THPT Quốc gia năm 2020 môn Anh trường THPT Ngô Quyền, Thành Phố Hải Phòng lần 1 mã đề 242Documento5 pagineĐề thi thử THPT Quốc gia năm 2020 môn Anh trường THPT Ngô Quyền, Thành Phố Hải Phòng lần 1 mã đề 242Nguyễn TrinhNessuna valutazione finora

- Dell Working CapitalDocumento6 pagineDell Working CapitalNavi Spl50% (2)

- The Manipulationof Retail Tradersby Market MakersDocumento8 pagineThe Manipulationof Retail Tradersby Market MakersEmma SulleNessuna valutazione finora

- The Black-Scholes Option Pricing Model (BSOPM) This Teaching Note Supplements Textbook Chapter 16Documento18 pagineThe Black-Scholes Option Pricing Model (BSOPM) This Teaching Note Supplements Textbook Chapter 16kenNessuna valutazione finora

- Fintech - Did Someone Cancel The Revolution?Documento16 pagineFintech - Did Someone Cancel The Revolution?Dominic PaolinoNessuna valutazione finora

- Project On SharekhanDocumento55 pagineProject On SharekhanjatinNessuna valutazione finora

- Assignment - UK GiltsDocumento3 pagineAssignment - UK GiltsAryan AnandNessuna valutazione finora

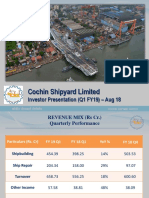

- CSL Investor Presentation Aug 18Documento21 pagineCSL Investor Presentation Aug 18gopalptkssNessuna valutazione finora

- Details of Jivan Arogya PlanDocumento4 pagineDetails of Jivan Arogya PlanbhaveshbhoiNessuna valutazione finora

- Airthread Connections Work Sheet SelfDocumento65 pagineAirthread Connections Work Sheet SelfkjhathiNessuna valutazione finora

- International Flow of FundsDocumento6 pagineInternational Flow of FundsSazedul EkabNessuna valutazione finora

- Corporate Finance Chapter10Documento55 pagineCorporate Finance Chapter10James ManningNessuna valutazione finora

- Working Capital Management of NTCDocumento49 pagineWorking Capital Management of NTCSovit Subedi67% (3)

- Financial Performance of Textile CompanyDocumento62 pagineFinancial Performance of Textile CompanySelva Kumar0% (1)

- ValueDocumento27 pagineValueTauhid Ahmed BappyNessuna valutazione finora

- Drill 1 - MidtermDocumento3 pagineDrill 1 - MidtermcpacpacpaNessuna valutazione finora