Potrebbero piacerti anche

- Ten-Decimal Tables of the Logarithms of Complex Numbers and for the Transformation from Cartesian to Polar Coordinates: Volume 33 in Mathematical Tables SeriesDa EverandTen-Decimal Tables of the Logarithms of Complex Numbers and for the Transformation from Cartesian to Polar Coordinates: Volume 33 in Mathematical Tables SeriesNessuna valutazione finora

- Mathematical Formulas for Economics and Business: A Simple IntroductionDa EverandMathematical Formulas for Economics and Business: A Simple IntroductionValutazione: 4 su 5 stelle4/5 (4)

- The Ramsey-Cass-Koopmans Model: Romer (2001), Ch. 2, Part ADocumento8 pagineThe Ramsey-Cass-Koopmans Model: Romer (2001), Ch. 2, Part ATan AdelineNessuna valutazione finora

- Fall2019 MidtermDocumento10 pagineFall2019 MidtermHui LiNessuna valutazione finora

- Makro - Otázka 2Documento11 pagineMakro - Otázka 2Izvrsnost1Nessuna valutazione finora

- Solow Growth ModelDocumento30 pagineSolow Growth ModelNadeem RaoNessuna valutazione finora

- Solow Growth ModelDocumento11 pagineSolow Growth Modelsalehina974Nessuna valutazione finora

- Solow Growth ModelDocumento9 pagineSolow Growth ModelChni GalsNessuna valutazione finora

- Macro State ExamDocumento17 pagineMacro State ExamOguz AslayNessuna valutazione finora

- Romer Macroeconomics, 4ed Chapter 1 SolutionsDocumento18 pagineRomer Macroeconomics, 4ed Chapter 1 Solutionswandersean75% (4)

- Section 6Documento8 pagineSection 6Tango BrillanteNessuna valutazione finora

- Linear System Ramsey Phase GraphDocumento15 pagineLinear System Ramsey Phase Graphmarithzahh9416Nessuna valutazione finora

- Econ 101b Lecture NotesDocumento7 pagineEcon 101b Lecture NotesSmi AndleebNessuna valutazione finora

- Fall2017 MidtermDocumento12 pagineFall2017 MidtermHui LiNessuna valutazione finora

- Advanced Macroeconomics Tutorial #1: SolutionsDocumento3 pagineAdvanced Macroeconomics Tutorial #1: SolutionsJonathan Peña OstosNessuna valutazione finora

- 1 Ramsey RA ModelDocumento10 pagine1 Ramsey RA Modelfabianmauricio482Nessuna valutazione finora

- Optimization: 1 Replacement ModelDocumento7 pagineOptimization: 1 Replacement ModelL IneshNessuna valutazione finora

- Lecturenotes CH 2Documento40 pagineLecturenotes CH 2Frédéric BlaisNessuna valutazione finora

- Difference Between Social and Natural ScienceDocumento5 pagineDifference Between Social and Natural ScienceBilal Ahmad AliNessuna valutazione finora

- Solow Growth ModelDocumento17 pagineSolow Growth ModelHella Mae RambunayNessuna valutazione finora

- Solution To Homework 2 - Exogeneous Growth ModelsDocumento11 pagineSolution To Homework 2 - Exogeneous Growth ModelsÁlvaro RobérioNessuna valutazione finora

- ECA5102: Lecture Notes: Topic 02: Ramsey-Cass-Koopmans ModelDocumento48 pagineECA5102: Lecture Notes: Topic 02: Ramsey-Cass-Koopmans ModelJonathanChanNessuna valutazione finora

- Assignment Week 4 Geochemistry Due Date: Week 6 Lecturer: Dyah Nindita Sahdarani, S.Si, M.EnergyDocumento5 pagineAssignment Week 4 Geochemistry Due Date: Week 6 Lecturer: Dyah Nindita Sahdarani, S.Si, M.Energyfarhan syariNessuna valutazione finora

- Kernel-Based Portfolio Management ModelDocumento8 pagineKernel-Based Portfolio Management ModelvidmantoNessuna valutazione finora

- Growth HW1Documento4 pagineGrowth HW1Froso ErotokritouNessuna valutazione finora

- Solving Dynare Eui2014 PDFDocumento84 pagineSolving Dynare Eui2014 PDFduc anhNessuna valutazione finora

- CH 8 - Lagrange MultipliersDocumento6 pagineCH 8 - Lagrange MultipliersHicham ElmirNessuna valutazione finora

- 2.4 The Chain RuleDocumento2 pagine2.4 The Chain Rulemasyuki1979Nessuna valutazione finora

- E1 251 Linear and Nonlinear Op2miza2onDocumento24 pagineE1 251 Linear and Nonlinear Op2miza2ondata scienceNessuna valutazione finora

- MATH 115: Lecture IX NotesDocumento2 pagineMATH 115: Lecture IX NotesDylan C. BeckNessuna valutazione finora

- Solution To Homework Assignment 4Documento6 pagineSolution To Homework Assignment 4cavanzasNessuna valutazione finora

- 1 Lecture Notes: The Solow ModelDocumento5 pagine1 Lecture Notes: The Solow Modelmrs dosadoNessuna valutazione finora

- ECON1003 Tut03 2023s2Documento33 pagineECON1003 Tut03 2023s2guohaolan0804Nessuna valutazione finora

- M M Sec: WaterDocumento8 pagineM M Sec: WaterPHƯƠNG HỒ ĐỖ UYÊNNessuna valutazione finora

- Lucas Tree PDFDocumento11 pagineLucas Tree PDFJohn Nash100% (1)

- 2.1 The Basic Structure: 8 Chapter 2: The Solow-Swan ModelDocumento27 pagine2.1 The Basic Structure: 8 Chapter 2: The Solow-Swan ModelAayush PandeyNessuna valutazione finora

- Homework 2 SolutionDocumento5 pagineHomework 2 Solutiondjoseph_1Nessuna valutazione finora

- Fourier Analysis On Ti-89Documento6 pagineFourier Analysis On Ti-89Jack KennedyNessuna valutazione finora

- Application of Differential CalculusDocumento21 pagineApplication of Differential CalculusTareq Islam100% (1)

- The Brock-Mirman Stochastic Growth ModelDocumento5 pagineThe Brock-Mirman Stochastic Growth ModelJhon Ortega GarciaNessuna valutazione finora

- EC744 Lecture Note 1: Prof. Jianjun MiaoDocumento18 pagineEC744 Lecture Note 1: Prof. Jianjun MiaobinicleNessuna valutazione finora

- Controllers - by Kenil JaganiDocumento24 pagineControllers - by Kenil Jaganikeniljagani513Nessuna valutazione finora

- Local Volatility, Stochastic Volatility and Jump-Diffusion ModelsDocumento21 pagineLocal Volatility, Stochastic Volatility and Jump-Diffusion ModelsHarshit GuptaNessuna valutazione finora

- Problem Set 2 Sample AnswersDocumento10 pagineProblem Set 2 Sample Answersjc224Nessuna valutazione finora

- Chapter 7 Solutions: WorkbookDocumento7 pagineChapter 7 Solutions: WorkbookNicolas BaroneNessuna valutazione finora

- Class ExercisesDocumento10 pagineClass ExercisesnibblesNessuna valutazione finora

- Assignment 1: Students: Esteban Morales & Rodrigo ReyesDocumento9 pagineAssignment 1: Students: Esteban Morales & Rodrigo ReyesPablo Moreno OlivaNessuna valutazione finora

- Problem Set 1 "Working With The Solow Model"Documento26 pagineProblem Set 1 "Working With The Solow Model"keyyongparkNessuna valutazione finora

- OCDM2223 Tutorial7solvedDocumento5 pagineOCDM2223 Tutorial7solvedqq727783Nessuna valutazione finora

- Control Systems Formula SheetDocumento12 pagineControl Systems Formula SheetliamhrNessuna valutazione finora

- Mathematics For Microeconomics: 6y y U, 8x X UDocumento8 pagineMathematics For Microeconomics: 6y y U, 8x X UAsia ButtNessuna valutazione finora

- 13 Corporate FinancingDocumento25 pagine13 Corporate FinancingKanika AggarwalNessuna valutazione finora

- VCREME K30-31 March-2019 MacroeconomicsDocumento2 pagineVCREME K30-31 March-2019 MacroeconomicsThe HoangNessuna valutazione finora

- Elements de Correction TD4 Microeconmie 1Documento7 pagineElements de Correction TD4 Microeconmie 1Ornel DJEUDJI NGASSAMNessuna valutazione finora

- CSE 5311 Homework 1 Solution: Problem 2.2-1Documento8 pagineCSE 5311 Homework 1 Solution: Problem 2.2-1tilahun0% (1)

- Midterm Exam - Econ 4020 v1 19 March 2018 Department of Economics York UniversityDocumento12 pagineMidterm Exam - Econ 4020 v1 19 March 2018 Department of Economics York University910220Nessuna valutazione finora

- Schap 22Documento16 pagineSchap 22Aljebre MohmedNessuna valutazione finora

- Romer 5e Solutions Manual 09Documento23 pagineRomer 5e Solutions Manual 09MatthewNessuna valutazione finora

- Mechatronics Lab ME 140L Introduction To Control Systems: I. Lecture 2: Transfer Functions, EigenvaluesDocumento13 pagineMechatronics Lab ME 140L Introduction To Control Systems: I. Lecture 2: Transfer Functions, EigenvaluesGrant GeorgiaNessuna valutazione finora

- Symmetric Root Locus LQR Design State Estimation: Selection of 'Optimal' Poles For SISO Pole Placement Design: SRLDocumento22 pagineSymmetric Root Locus LQR Design State Estimation: Selection of 'Optimal' Poles For SISO Pole Placement Design: SRLP_leeNessuna valutazione finora

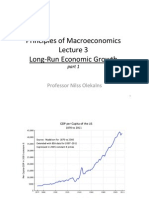

- Principles of Macroeconomics Lecture 3 Long - Run Economic GrowthDocumento4 paginePrinciples of Macroeconomics Lecture 3 Long - Run Economic GrowthTeh Kim SinNessuna valutazione finora

- Principles of Macroeconomics Lecture 3 Long - Run Economic GrowthDocumento10 paginePrinciples of Macroeconomics Lecture 3 Long - Run Economic GrowthTeh Kim SinNessuna valutazione finora

- Datastream Installation Guide PDFDocumento4 pagineDatastream Installation Guide PDFTeh Kim SinNessuna valutazione finora

- Principles of Macroeconomics Lecture 3 Long - Run Economic GrowthDocumento2 paginePrinciples of Macroeconomics Lecture 3 Long - Run Economic GrowthTeh Kim SinNessuna valutazione finora

- Lecture Slides Lecture 2 Part 2Documento7 pagineLecture Slides Lecture 2 Part 2Teh Kim SinNessuna valutazione finora

- Lecture Slides Lecture 2 Part 1Documento4 pagineLecture Slides Lecture 2 Part 1Teh Kim SinNessuna valutazione finora

- Lecture Slides Lecture 1 Part 1Documento5 pagineLecture Slides Lecture 1 Part 1Teh Kim SinNessuna valutazione finora

- Popitz LawDocumento2 paginePopitz LawTeh Kim SinNessuna valutazione finora

- Grabbing Hand and Market Preserving FederalismDocumento1 paginaGrabbing Hand and Market Preserving FederalismTeh Kim SinNessuna valutazione finora

- 15.1 A) The Monthly Growth Rate in IP Expressed in Percentage Points, Ip - Growth 100 Log (Ip/ip (-1) )Documento4 pagine15.1 A) The Monthly Growth Rate in IP Expressed in Percentage Points, Ip - Growth 100 Log (Ip/ip (-1) )Teh Kim SinNessuna valutazione finora

- HTTP 1Documento1 paginaHTTP 1Teh Kim SinNessuna valutazione finora

- 5d814c4d6437b300fd0e227a - Scorch Product Sheet 512GB PDFDocumento1 pagina5d814c4d6437b300fd0e227a - Scorch Product Sheet 512GB PDFBobby B. BrownNessuna valutazione finora

- Surveillance of Healthcare-Associated Infections in Indonesian HospitalsDocumento12 pagineSurveillance of Healthcare-Associated Infections in Indonesian HospitalsRidha MardiyaniNessuna valutazione finora

- Surname 1: Why Attend To WMO? Who Would Not Trust The Brand That Their Friends Strongly Recommend? It IsDocumento4 pagineSurname 1: Why Attend To WMO? Who Would Not Trust The Brand That Their Friends Strongly Recommend? It IsNikka GadazaNessuna valutazione finora

- 2018 Za (Q + Ma) Ac1025Documento95 pagine2018 Za (Q + Ma) Ac1025전민건Nessuna valutazione finora

- Template For Public BiddingDocumento3 pagineTemplate For Public BiddingFederico DomingoNessuna valutazione finora

- 29!541 Transient Aspects of Unloading Oil and Gas Wells With Coiled TubingDocumento6 pagine29!541 Transient Aspects of Unloading Oil and Gas Wells With Coiled TubingWaode GabriellaNessuna valutazione finora

- 6.T24 Common Variables-R14Documento29 pagine6.T24 Common Variables-R14Med Mehdi LaazizNessuna valutazione finora

- Case Study: Meera P NairDocumento9 pagineCase Study: Meera P Nairnanditha menonNessuna valutazione finora

- Dell PowerEdge M1000e Spec SheetDocumento2 pagineDell PowerEdge M1000e Spec SheetRochdi BouzaienNessuna valutazione finora

- LCD Television Service Manual: Chassis MTK8222 Product TypeDocumento46 pagineLCD Television Service Manual: Chassis MTK8222 Product TypetvdenNessuna valutazione finora

- Controllogix EthernetDocumento136 pagineControllogix Ethernetcnp0705Nessuna valutazione finora

- ProposalDocumento8 pagineProposalapi-295634125Nessuna valutazione finora

- 001-026 Labor RevDocumento64 pagine001-026 Labor RevDexter GasconNessuna valutazione finora

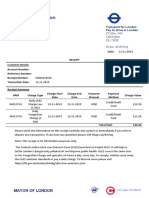

- Transport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDocumento1 paginaTransport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDanyy MaciucNessuna valutazione finora

- Geography Cba PowerpointDocumento10 pagineGeography Cba Powerpointapi-489088076Nessuna valutazione finora

- PRU03Documento4 paginePRU03Paul MathewNessuna valutazione finora

- Workbook, Exercises-Unit 8Documento6 pagineWorkbook, Exercises-Unit 8Melanie ValdezNessuna valutazione finora

- Thesis-Android-Based Health-Care Management System: July 2016Documento66 pagineThesis-Android-Based Health-Care Management System: July 2016Noor Md GolamNessuna valutazione finora

- For Visual Studio User'S Manual: Motoplus SDKDocumento85 pagineFor Visual Studio User'S Manual: Motoplus SDKMihail AvramovNessuna valutazione finora

- Openness and The Market Friendly ApproachDocumento27 pagineOpenness and The Market Friendly Approachmirzatouseefahmed100% (2)

- Tire Size ComparisonDocumento1 paginaTire Size ComparisonBudi DarmawanNessuna valutazione finora

- IA1 - Mock AssessmentDocumento3 pagineIA1 - Mock AssessmentMohammad Mokhtarul HaqueNessuna valutazione finora

- Microeconomics Theory and Applications 12th Edition Browning Solutions ManualDocumento5 pagineMicroeconomics Theory and Applications 12th Edition Browning Solutions Manualhauesperanzad0ybz100% (26)

- IT Quiz QuestionsDocumento10 pagineIT Quiz QuestionsbrittosabuNessuna valutazione finora

- Pocket Pod PresetsDocumento13 paginePocket Pod PresetsmarcusolivusNessuna valutazione finora

- Aircraft Materials and Hardware: (Nuts, Studs, Screws)Documento25 pagineAircraft Materials and Hardware: (Nuts, Studs, Screws)PakistaniTalent cover songsNessuna valutazione finora

- Case Study On DominoDocumento7 pagineCase Study On Dominodisha_pandey_4Nessuna valutazione finora

- Stirling Bio Power GeneratorDocumento5 pagineStirling Bio Power GeneratorAvram Stefan100% (2)

- WSM - Ziale - Commercial Law NotesDocumento36 pagineWSM - Ziale - Commercial Law NotesElizabeth Chilufya100% (1)

- PlayAGS, Inc.Documento309 paginePlayAGS, Inc.vicr100Nessuna valutazione finora