Potrebbero piacerti anche

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Subjective Probability Criticisms, Reflections, and Problems - Henry Kyburg PDFDocumento24 pagineSubjective Probability Criticisms, Reflections, and Problems - Henry Kyburg PDFGu Si FangNessuna valutazione finora

- Pages de Alchemists of Loss - Devin DowdDocumento4 paginePages de Alchemists of Loss - Devin DowdGu Si FangNessuna valutazione finora

- Addictive Drugs The Cigarette Experience, Thomas Schelling (1992)Documento3 pagineAddictive Drugs The Cigarette Experience, Thomas Schelling (1992)Gu Si FangNessuna valutazione finora

- Economists Favour The Price System - Who Else DoesDocumento27 pagineEconomists Favour The Price System - Who Else DoesGu Si FangNessuna valutazione finora

- Canadian Currency and Exchange Under French RuleDocumento91 pagineCanadian Currency and Exchange Under French RuleGu Si FangNessuna valutazione finora

- The Shanxi BanksDocumento25 pagineThe Shanxi BanksGu Si FangNessuna valutazione finora

- 1902.01.04 Financial Prosperity Predicted (Imperial Press)Documento3 pagine1902.01.04 Financial Prosperity Predicted (Imperial Press)Gu Si FangNessuna valutazione finora

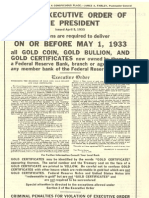

- 1933 Gold Confiscation OrderDocumento2 pagine1933 Gold Confiscation OrderJason ChanNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Core CompetenciesDocumento3 pagineCore CompetenciesS on the GoNessuna valutazione finora

- Comparison Between Limit Equilibrium and Finite Element Method For Slope Stability AnalysisDocumento7 pagineComparison Between Limit Equilibrium and Finite Element Method For Slope Stability AnalysisRed Orange100% (1)

- Netapp Powershell CommandsDocumento74 pagineNetapp Powershell CommandsravishankarNessuna valutazione finora

- A1603 WTDocumento9 pagineA1603 WTnanichowsNessuna valutazione finora

- Mayo Medical School: College of MedicineDocumento28 pagineMayo Medical School: College of MedicineDragomir IsabellaNessuna valutazione finora

- Using Keyframe SynfigDocumento1 paginaUsing Keyframe SynfigNdandungNessuna valutazione finora

- Laws of ReflectionDocumento3 pagineLaws of ReflectionwscienceNessuna valutazione finora

- Voyagers: Game of Flames (Book 2) by Robin WassermanDocumento35 pagineVoyagers: Game of Flames (Book 2) by Robin WassermanRandom House KidsNessuna valutazione finora

- Muscle Tone PhysiologyDocumento5 pagineMuscle Tone PhysiologyfatimaNessuna valutazione finora

- Science Investigatory Project PDFDocumento2 pagineScience Investigatory Project PDFNick john CaminadeNessuna valutazione finora

- Data Communications: ECE 583 LectureDocumento6 pagineData Communications: ECE 583 Lecturechloe005Nessuna valutazione finora

- International Baccalaureate ProgrammeDocumento5 pagineInternational Baccalaureate Programmeapi-280508830Nessuna valutazione finora

- Application Letter.Documento2 pagineApplication Letter.RinzuNessuna valutazione finora

- Power Point Exercise IDocumento6 paginePower Point Exercise IAze FerriolsNessuna valutazione finora

- Prizm Programming GuideDocumento168 paginePrizm Programming GuideBucur MateiNessuna valutazione finora

- CriminologyDocumento2 pagineCriminologydeliriummagic100% (1)

- 40agilemethodsin40minutes 141020221938 Conversion Gate01 PDFDocumento104 pagine40agilemethodsin40minutes 141020221938 Conversion Gate01 PDFpjsystemNessuna valutazione finora

- July 1Documento5 pagineJuly 1June RañolaNessuna valutazione finora

- Mevlana Jelaluddin RumiDocumento3 pagineMevlana Jelaluddin RumiMohammed Abdul Hafeez, B.Com., Hyderabad, IndiaNessuna valutazione finora

- Maths InterviewDocumento6 pagineMaths InterviewKeamogetse BoitshwareloNessuna valutazione finora

- Ims Kuk SullybusDocumento84 pagineIms Kuk SullybusJoginder ChhikaraNessuna valutazione finora

- General Biology 2 Midterms GRASPSDocumento2 pagineGeneral Biology 2 Midterms GRASPSAlbert RoseteNessuna valutazione finora

- Sample Codal ComplianceDocumento1 paginaSample Codal Complianceshangz1511Nessuna valutazione finora

- Chapter One 1.1. Background of The Study: Iloilo City's Heritage Tourist Destinations Are Worth Keeping ForDocumento2 pagineChapter One 1.1. Background of The Study: Iloilo City's Heritage Tourist Destinations Are Worth Keeping ForCrisNessuna valutazione finora

- Raj Yoga ReportDocumento17 pagineRaj Yoga ReportSweaty Sunny50% (2)

- Class 8 - CH 12 Exponents Powers - Ws 2Documento3 pagineClass 8 - CH 12 Exponents Powers - Ws 2Sparsh BhatnagarNessuna valutazione finora

- Autoliv LeanDocumento50 pagineAutoliv LeanRajasekaran Murugan100% (1)

- FIITJEE Class VIII Practice PaperDocumento8 pagineFIITJEE Class VIII Practice PaperD Samy100% (1)

- Magnesium Casting Technology For Structural ApplicationsDocumento21 pagineMagnesium Casting Technology For Structural ApplicationsJinsoo KimNessuna valutazione finora

- Gold Exp C1 U4 Lang Test BDocumento2 pagineGold Exp C1 U4 Lang Test Bmaituti1Nessuna valutazione finora