Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- What Is Reverse ChargeDocumento6 pagineWhat Is Reverse Chargevai8havNessuna valutazione finora

- The Payment of Wages ActDocumento2 pagineThe Payment of Wages Actvai8havNessuna valutazione finora

- Wages For ESICDocumento10 pagineWages For ESICvai8havNessuna valutazione finora

- The Payment of Wages ActDocumento2 pagineThe Payment of Wages Actvai8havNessuna valutazione finora

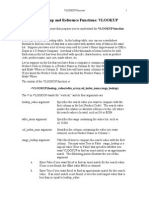

- Vlookup ExerciseDocumento3 pagineVlookup Exercisevai8havNessuna valutazione finora

- Understanding Vlookup.: Refer Attached Sheet For ExplanationDocumento1 paginaUnderstanding Vlookup.: Refer Attached Sheet For Explanationvai8havNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Composite ContractsDocumento27 pagineComposite ContractsAmita SinwarNessuna valutazione finora

- HTTP://WWW - Ascgroup.in/mag/asc Times Jun 18th Jun 23rd PDFDocumento16 pagineHTTP://WWW - Ascgroup.in/mag/asc Times Jun 18th Jun 23rd PDFDigital marketerNessuna valutazione finora

- Indirect Tax Laws NewDocumento895 pagineIndirect Tax Laws NewAndal ParthibanNessuna valutazione finora

- Name: MJR Invest: Your Current A/C StatusDocumento5 pagineName: MJR Invest: Your Current A/C Statusmaakabhawan26Nessuna valutazione finora

- Cfa Tariff 25042013 PDFDocumento26 pagineCfa Tariff 25042013 PDFBasavaraju K NNessuna valutazione finora

- FASTag - Statement1032014763720200501124625793 - OW PDFDocumento4 pagineFASTag - Statement1032014763720200501124625793 - OW PDFNarasimha SandakaNessuna valutazione finora

- TaxationDocumento742 pagineTaxationSrinivasa Rao Bandlamudi83% (6)

- Supply and Its TypesDocumento30 pagineSupply and Its TypesAmit GuptaNessuna valutazione finora

- Notification No. 52/2011-Service Tax: ProvidedDocumento12 pagineNotification No. 52/2011-Service Tax: Providedsatish kumarNessuna valutazione finora

- Unpriced BidDocumento169 pagineUnpriced BidbalangceNessuna valutazione finora

- India GST For Beginners by Jayaram Hiregange, Deepak RaoDocumento108 pagineIndia GST For Beginners by Jayaram Hiregange, Deepak Raonarasimma8313Nessuna valutazione finora

- Chiripal Industries LTD For CASEDocumento21 pagineChiripal Industries LTD For CASEAbhishek Mehta100% (1)

- Nitin PDFDocumento2 pagineNitin PDFAnonymous uHXjXqhvoL100% (1)

- Paper 11 NEW GST PDFDocumento399 paginePaper 11 NEW GST PDFsomaanvithaNessuna valutazione finora

- KLTPS 1310 W620 Tech 150610Documento26 pagineKLTPS 1310 W620 Tech 150610kinner3Nessuna valutazione finora

- Taxation-Income From House PropertyDocumento17 pagineTaxation-Income From House PropertyYang DeyNessuna valutazione finora

- Registering An E-Commerce Business in India Sole Proprietorship 101 Zepo The ECommerce Blog For Indian Online SellersDocumento125 pagineRegistering An E-Commerce Business in India Sole Proprietorship 101 Zepo The ECommerce Blog For Indian Online SellersTito FernandezNessuna valutazione finora

- Complete CMF Form Jan2014Documento4 pagineComplete CMF Form Jan2014Mukul SoniNessuna valutazione finora

- Last Updated On 1-10-2022Documento115 pagineLast Updated On 1-10-2022Pranav SharmaNessuna valutazione finora

- Indian Insitute of Job-Oriented Training Tally Assignment: Company CreationDocumento42 pagineIndian Insitute of Job-Oriented Training Tally Assignment: Company CreationAAC aacNessuna valutazione finora

- Mediclaim ReceiptDocumento1 paginaMediclaim ReceiptAditya Kumar G.VNessuna valutazione finora

- Fixedline and Broadband ServicesDocumento6 pagineFixedline and Broadband ServicesAkhil MenonNessuna valutazione finora

- Duties and Taxes For Govt Purchase ProposalsDocumento45 pagineDuties and Taxes For Govt Purchase Proposalsdate_milindNessuna valutazione finora

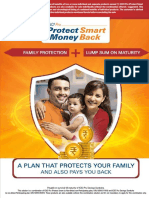

- ICICIPru IProtectSmart MoneyBackDocumento4 pagineICICIPru IProtectSmart MoneyBacksaurabh sumanNessuna valutazione finora

- Car RelianceDocumento5 pagineCar RelianceAnupam AwasthiNessuna valutazione finora

- TASMA Annual Report For 2017-18Documento222 pagineTASMA Annual Report For 2017-18Senthil KumarNessuna valutazione finora

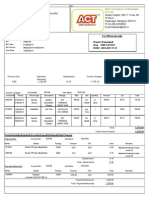

- Your Renewal Premium Receipt: Receipt Number: 0366160700008 Date: 12 Nov 2019Documento1 paginaYour Renewal Premium Receipt: Receipt Number: 0366160700008 Date: 12 Nov 2019Nag PallaNessuna valutazione finora

- Expression of Interest GMADADocumento30 pagineExpression of Interest GMADAchithiraNessuna valutazione finora

- Soa 620749 032014Documento2 pagineSoa 620749 032014vickyvarathNessuna valutazione finora

- Vision Ias PT 365 Economy 2020Documento85 pagineVision Ias PT 365 Economy 2020Ekta RahulNessuna valutazione finora