Potrebbero piacerti anche

- Filling Station GuidelinesDocumento8 pagineFilling Station GuidelinesOladipupo Mayowa PaulNessuna valutazione finora

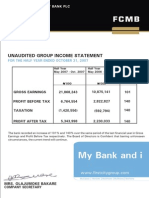

- 2007 Q2resultsDocumento1 pagina2007 Q2resultsOladipupo Mayowa PaulNessuna valutazione finora

- 9854 Goldlink Insurance Audited 2013 Financial Statements May 2015Documento3 pagine9854 Goldlink Insurance Audited 2013 Financial Statements May 2015Oladipupo Mayowa PaulNessuna valutazione finora

- 9M 2013 Unaudited ResultsDocumento2 pagine9M 2013 Unaudited ResultsOladipupo Mayowa PaulNessuna valutazione finora

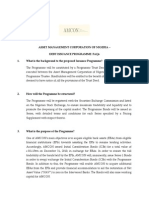

- Amcon Bonds FaqDocumento4 pagineAmcon Bonds FaqOladipupo Mayowa PaulNessuna valutazione finora

- Dec09 Inv Presentation GAAPDocumento23 pagineDec09 Inv Presentation GAAPOladipupo Mayowa PaulNessuna valutazione finora

- 2007 Q1resultsDocumento1 pagina2007 Q1resultsOladipupo Mayowa PaulNessuna valutazione finora

- First City Monument Bank PLC.: Investor/Analyst Presentation Review of H1 2008/9 ResultsDocumento31 pagineFirst City Monument Bank PLC.: Investor/Analyst Presentation Review of H1 2008/9 ResultsOladipupo Mayowa PaulNessuna valutazione finora

- FCMB Group PLC 3Q13 (IFRS) Group Results Investors & Analysts PresentationDocumento32 pagineFCMB Group PLC 3Q13 (IFRS) Group Results Investors & Analysts PresentationOladipupo Mayowa PaulNessuna valutazione finora

- Unaudited Half Year Result As at June 30 2011Documento5 pagineUnaudited Half Year Result As at June 30 2011Oladipupo Mayowa PaulNessuna valutazione finora

- Margin Requirement Examples For Sample Options-Based PositionsDocumento2 pagineMargin Requirement Examples For Sample Options-Based PositionsOladipupo Mayowa PaulNessuna valutazione finora

- Fs 2011 GtbankDocumento17 pagineFs 2011 GtbankOladipupo Mayowa PaulNessuna valutazione finora

- June 2011 Results PresentationDocumento17 pagineJune 2011 Results PresentationOladipupo Mayowa PaulNessuna valutazione finora

- Full Year 2011 Results Presentation 2Documento16 pagineFull Year 2011 Results Presentation 2Oladipupo Mayowa PaulNessuna valutazione finora

- 2012 Year End Results Press ReleaseDocumento3 pagine2012 Year End Results Press ReleaseOladipupo Mayowa PaulNessuna valutazione finora

- June 2012 Investor PresentationDocumento17 pagineJune 2012 Investor PresentationOladipupo Mayowa PaulNessuna valutazione finora

- 2011 Half Year Result StatementDocumento3 pagine2011 Half Year Result StatementOladipupo Mayowa PaulNessuna valutazione finora

- 2013 Year End Results Press Release - Final WebDocumento3 pagine2013 Year End Results Press Release - Final WebOladipupo Mayowa PaulNessuna valutazione finora

- Val Project 6Documento17 pagineVal Project 6Oladipupo Mayowa PaulNessuna valutazione finora

- Ratio Back SpreadsDocumento20 pagineRatio Back SpreadsOladipupo Mayowa PaulNessuna valutazione finora

- Marriott ValuationDocumento16 pagineMarriott ValuationOladipupo Mayowa PaulNessuna valutazione finora

- International Hotel Appraisers4Documento5 pagineInternational Hotel Appraisers4Oladipupo Mayowa PaulNessuna valutazione finora

- Banking Finance Sectorial OverviewDocumento15 pagineBanking Finance Sectorial OverviewOladipupo Mayowa PaulNessuna valutazione finora

- Hotels and Motels - Industry Data and AnalysisDocumento8 pagineHotels and Motels - Industry Data and AnalysisOladipupo Mayowa PaulNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- FINN 100-Principles of Finance-Mohammad Basharullah-Arslan Shahid Butt-Humza GhaffarDocumento7 pagineFINN 100-Principles of Finance-Mohammad Basharullah-Arslan Shahid Butt-Humza GhaffarHaris AliNessuna valutazione finora

- Property Transactions OutlineDocumento63 pagineProperty Transactions OutlineslcsandraNessuna valutazione finora

- Report On DisclosureDocumento15 pagineReport On Disclosuredeath_heavenNessuna valutazione finora

- Agrarian Law (Landbank vs. Alsua)Documento4 pagineAgrarian Law (Landbank vs. Alsua)Maestro LazaroNessuna valutazione finora

- SAS New Syllabus From 2024 Exam FinalDocumento23 pagineSAS New Syllabus From 2024 Exam FinalManjit ThakueNessuna valutazione finora

- BondssDocumento7 pagineBondssDyenNessuna valutazione finora

- Project Based On MergerDocumento24 pagineProject Based On MergerPrince RattanNessuna valutazione finora

- The Law On Taxability of Gifts Under The IncomeDocumento26 pagineThe Law On Taxability of Gifts Under The IncomeVipul ShahNessuna valutazione finora

- UFS - Circular Dated 30 Jan 2015 P4 PDFDocumento267 pagineUFS - Circular Dated 30 Jan 2015 P4 PDFsyahrir83Nessuna valutazione finora

- Cfasmc 3040Documento13 pagineCfasmc 3040Ahmadnur JulNessuna valutazione finora

- Lundolm & Sloan. Equity Valuation and Analysis With Eval. 3rd Edition CHP 01Documento5 pagineLundolm & Sloan. Equity Valuation and Analysis With Eval. 3rd Edition CHP 01Peter Pa N0% (1)

- Material Ledgers - Actual CostingDocumento17 pagineMaterial Ledgers - Actual CostingAbp PbaNessuna valutazione finora

- Analyst/Associate Investment Banking Interview Questions: Checklist For InterviewerDocumento6 pagineAnalyst/Associate Investment Banking Interview Questions: Checklist For Interviewermanish mishraNessuna valutazione finora

- Calvares VineyardsDocumento16 pagineCalvares Vineyardsigulati23100% (6)

- Intrinsic Value of Aurobindo PharmaDocumento6 pagineIntrinsic Value of Aurobindo PharmaTirth ThakkarNessuna valutazione finora

- Value Investing With Legends (Santos, Greenwald, Eveillard) SP2015Documento6 pagineValue Investing With Legends (Santos, Greenwald, Eveillard) SP2015ascentcommerce100% (1)

- Advanced Accounting Part 1 Dayag 2015 Chapter 11Documento31 pagineAdvanced Accounting Part 1 Dayag 2015 Chapter 11Girlie Regilme Balingbing50% (2)

- Course Outline M. Com Part 1 BZU, MultanDocumento5 pagineCourse Outline M. Com Part 1 BZU, MultanabidnaeemkhokherNessuna valutazione finora

- Corporate Valuation & Financial Modelling - 2020: A Co. B CoDocumento3 pagineCorporate Valuation & Financial Modelling - 2020: A Co. B CoRakshith PsNessuna valutazione finora

- Act 201 Course OutlineDocumento4 pagineAct 201 Course Outlineapi-538665209Nessuna valutazione finora

- Stock Market - A Complete Guide BookDocumento43 pagineStock Market - A Complete Guide BookParag Saxena100% (1)

- Price Action SetupsDocumento1 paginaPrice Action Setupsgato444100% (1)

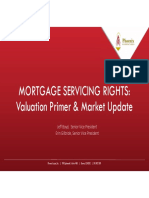

- MSR Valuation and Market Update May12 TMC WebinarDocumento45 pagineMSR Valuation and Market Update May12 TMC WebinarsinhaaNessuna valutazione finora

- Week III NVCA Valuation GuidelinesDocumento5 pagineWeek III NVCA Valuation GuidelinesIgor MinyukhinNessuna valutazione finora

- Multiple Choice Questions: Top of FormDocumento96 pagineMultiple Choice Questions: Top of Formchanfa3851Nessuna valutazione finora

- Partnership 3Documento38 paginePartnership 3kakaoNessuna valutazione finora

- 2014 Global Salary SurveyDocumento499 pagine2014 Global Salary SurveyMiguel Comino LópezNessuna valutazione finora

- Ichimoku Trading System PDFDocumento15 pagineIchimoku Trading System PDFMrugenNessuna valutazione finora

- ROI, EVA and MVA IntroductionDocumento4 pagineROI, EVA and MVA IntroductionkeyurNessuna valutazione finora