Potrebbero piacerti anche

- 857compendium September 2017 PDFDocumento63 pagine857compendium September 2017 PDFJason DunlapNessuna valutazione finora

- Tax Sem VIIIDocumento27 pagineTax Sem VIIIJason DunlapNessuna valutazione finora

- Cls-Corporate Tax (Honours) SyllabusDocumento3 pagineCls-Corporate Tax (Honours) SyllabusSurabhi MaheshwariNessuna valutazione finora

- Concept of ResidenceDocumento4 pagineConcept of ResidenceJason DunlapNessuna valutazione finora

- Convencao de Viena de 1978 Sobre Sucessao de Estados em Materia de TratadosDocumento24 pagineConvencao de Viena de 1978 Sobre Sucessao de Estados em Materia de Tratadosnunomm25Nessuna valutazione finora

- Insurance Project FinalDocumento17 pagineInsurance Project Finalamitkmara0% (1)

- Indian Society Structure & Processes Course OverviewDocumento2 pagineIndian Society Structure & Processes Course OverviewJason DunlapNessuna valutazione finora

- Insurance Project FinalDocumento17 pagineInsurance Project Finalamitkmara0% (1)

- Moot CaseDocumento4 pagineMoot CaseJason DunlapNessuna valutazione finora

- Government of India Law Commission of IndiaDocumento1 paginaGovernment of India Law Commission of IndiaJason DunlapNessuna valutazione finora

- Moot CaseDocumento4 pagineMoot CaseJason DunlapNessuna valutazione finora

- Moot CaseDocumento4 pagineMoot CaseJason DunlapNessuna valutazione finora

- SociologyDocumento2 pagineSociologyJason DunlapNessuna valutazione finora

- Concept of ResidenceDocumento4 pagineConcept of ResidenceJason DunlapNessuna valutazione finora

- PUBLIC POLICY PROCESSDocumento4 paginePUBLIC POLICY PROCESSJason DunlapNessuna valutazione finora

- CRPC 164: Section 164 of The Criminal Procedure Code: Recording of Confessions and StatementsDocumento2 pagineCRPC 164: Section 164 of The Criminal Procedure Code: Recording of Confessions and StatementsJason DunlapNessuna valutazione finora

- Coa Ition PoliticsDocumento25 pagineCoa Ition PoliticsJason DunlapNessuna valutazione finora

- Indian Political System: Centre-State RelationDocumento18 pagineIndian Political System: Centre-State RelationJason DunlapNessuna valutazione finora

- Family Law II SyllabusDocumento5 pagineFamily Law II SyllabusJason DunlapNessuna valutazione finora

- Arbitration Independent ClauseDocumento4 pagineArbitration Independent ClauseJason DunlapNessuna valutazione finora

- Ancient IndiaDocumento7 pagineAncient IndiayogshastriNessuna valutazione finora

- Indian Political System-SyllabusDocumento2 pagineIndian Political System-SyllabusJason DunlapNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5783)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- 2.01 Signatours Corporation V All Seasons Vacation Rentals LLC ComplaintDocumento6 pagine2.01 Signatours Corporation V All Seasons Vacation Rentals LLC ComplaintCopyright Anti-Bullying Act (CABA Law)Nessuna valutazione finora

- The American Pageant - Chapter 23 Review SheetDocumento3 pagineThe American Pageant - Chapter 23 Review SheetJoesterNessuna valutazione finora

- Legal English doublets and tripletsDocumento3 pagineLegal English doublets and tripletsMaria Do Mar Carmo CordeiroNessuna valutazione finora

- Minutes SEFDocumento3 pagineMinutes SEFMary Mae Villaruel BantilloNessuna valutazione finora

- Ispl 2Documento28 pagineIspl 2Chakradhar GunjanNessuna valutazione finora

- 02 Perena v. ZarateDocumento8 pagine02 Perena v. ZaratePaolo Enrino PascualNessuna valutazione finora

- Terms and Definitions in ObliconDocumento3 pagineTerms and Definitions in Obliconmaccy adalidNessuna valutazione finora

- Municipal Corporation of Delhi Vs Subhagwanti & Others (With ..Documento6 pagineMunicipal Corporation of Delhi Vs Subhagwanti & Others (With ..Harman Saini100% (1)

- SCH k-1 of 1120s Case StudyDocumento1 paginaSCH k-1 of 1120s Case StudyHimani SachdevNessuna valutazione finora

- Gliceria Marella Vs ReyesDocumento1 paginaGliceria Marella Vs ReyesLinus ReyesNessuna valutazione finora

- 4 Allado Vs DioknoDocumento12 pagine4 Allado Vs DioknoBryne BoishNessuna valutazione finora

- 4 PP v. EvaristoDocumento4 pagine4 PP v. EvaristoryanmeinNessuna valutazione finora

- Pemberontakkan Komunis Di Selatan Thailand 1965Documento9 paginePemberontakkan Komunis Di Selatan Thailand 1965Nur Husna RemiNessuna valutazione finora

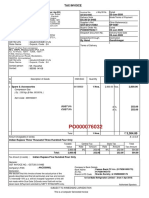

- Tax Invoice: Ice Make Refrigeration Limited - (From 1-Apr-2019)Documento1 paginaTax Invoice: Ice Make Refrigeration Limited - (From 1-Apr-2019)Sunil PatelNessuna valutazione finora

- COLDPLAY - A Head Full of Dreams Tour - 1 PDFDocumento3 pagineCOLDPLAY - A Head Full of Dreams Tour - 1 PDFVicky WardhanaNessuna valutazione finora

- Service Contract Agreement TemplateDocumento3 pagineService Contract Agreement Templateanon_84814261675% (4)

- DMLCIIDocumento2 pagineDMLCIIVu Tung LinhNessuna valutazione finora

- Lake County Sex Offender StatementDocumento1 paginaLake County Sex Offender StatementNewsNation DigitalNessuna valutazione finora

- KWASEKO CBO ConstitutionDocumento7 pagineKWASEKO CBO ConstitutionSharon Amondi50% (2)

- People v. Sayo y Reyes, G.R. No. 227704, (April 10, 2019)Documento25 paginePeople v. Sayo y Reyes, G.R. No. 227704, (April 10, 2019)Olga Pleños ManingoNessuna valutazione finora

- Ben GuetDocumento25 pagineBen GuetMalibog AkoNessuna valutazione finora

- Escritura PublicaDocumento4 pagineEscritura PublicaluisaNessuna valutazione finora

- Philippines Supreme Court Rules Against Lumber Company's Claim to Offset Reforestation Charges Against Forest Charges OwedDocumento4 paginePhilippines Supreme Court Rules Against Lumber Company's Claim to Offset Reforestation Charges Against Forest Charges OwedElle BaylonNessuna valutazione finora

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocumento11 pagineBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledMaya TolentinoNessuna valutazione finora

- Persons and Family Law NotesDocumento10 paginePersons and Family Law NotesMaria Dana BrillantesNessuna valutazione finora

- BBA Vs Union of India 2011 PDFDocumento22 pagineBBA Vs Union of India 2011 PDFPrashant SharmaNessuna valutazione finora

- Warren H. Wheeler, an Infant, and J. H. Wheeler, His Father and Next Friend, and C. C. Spaulding, Iii, an Infant, and C. C. Spaulding, Jr., His Father and Next Friend v. Durham City Board of Education, a Body Politic in Durham County, North Carolina, 309 F.2d 630, 4th Cir. (1962)Documento5 pagineWarren H. Wheeler, an Infant, and J. H. Wheeler, His Father and Next Friend, and C. C. Spaulding, Iii, an Infant, and C. C. Spaulding, Jr., His Father and Next Friend v. Durham City Board of Education, a Body Politic in Durham County, North Carolina, 309 F.2d 630, 4th Cir. (1962)Scribd Government DocsNessuna valutazione finora

- Joint UltimoDocumento32 pagineJoint UltimoNoemi Livia VaraNessuna valutazione finora

- Child Abuse LawDocumento3 pagineChild Abuse LawbaimonaNessuna valutazione finora