Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- At Reviewer Part II - (May 2015 Batch)Documento22 pagineAt Reviewer Part II - (May 2015 Batch)Jake BundokNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- AP 5904 InvestmentsDocumento9 pagineAP 5904 InvestmentsJake BundokNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Mandarin V3Documento18 pagineMandarin V3Jake BundokNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Calendar - 2015 02 01 - 2015 03 01 PDFDocumento1 paginaCalendar - 2015 02 01 - 2015 03 01 PDFJake BundokNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Maple Leaf Study EDocumento4 pagineMaple Leaf Study EFaraz HaqNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- AP 5904 InvestmentsDocumento9 pagineAP 5904 InvestmentsJake BundokNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Jan 2015 (Manila) ,: Holidays in PhilippinesDocumento1 paginaJan 2015 (Manila) ,: Holidays in PhilippinesJake BundokNessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Gmat Handbook PDFDocumento20 pagineGmat Handbook PDFVishal GolchaNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Advanced Accounting-Volume 2Documento4 pagineAdvanced Accounting-Volume 2ronnelson pascual25% (16)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- REVIEW QUESTIONS Investment in Debt SecuritiesDocumento1 paginaREVIEW QUESTIONS Investment in Debt SecuritiesJake BundokNessuna valutazione finora

- Debt Securities: BondsDocumento9 pagineDebt Securities: BondsCorinne GohocNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- AP 5904 InvestmentsDocumento9 pagineAP 5904 InvestmentsJake BundokNessuna valutazione finora

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- GuideDocumento4 pagineGuideJake BundokNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Dlsu Thesis Paper LetterheadDocumento1 paginaDlsu Thesis Paper LetterheadJake BundokNessuna valutazione finora

- X Deal FoodDocumento1 paginaX Deal FoodJake BundokNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Elimination Round BreakthroughDocumento16 pagineElimination Round BreakthroughJake BundokNessuna valutazione finora

- Seitani (2013) Toolkit For DSGEDocumento27 pagineSeitani (2013) Toolkit For DSGEJake BundokNessuna valutazione finora

- SOX On ISDocumento5 pagineSOX On ISJake BundokNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Park JMP PDFDocumento56 paginePark JMP PDFJake BundokNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Child Labor Data 2011 - 2013 (Jan)Documento2 pagineChild Labor Data 2011 - 2013 (Jan)Jake BundokNessuna valutazione finora

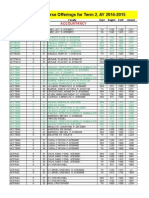

- RVR-COB Course Offerings Term 2Documento19 pagineRVR-COB Course Offerings Term 2sweetjar22Nessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Tips DefenseDocumento35 pagineTips DefenseJake BundokNessuna valutazione finora

- SSRN Id975135Documento44 pagineSSRN Id975135Jake BundokNessuna valutazione finora

- Modeling With Exp & Power FunctionsDocumento27 pagineModeling With Exp & Power FunctionsJake BundokNessuna valutazione finora

- Cpi 1997Documento17 pagineCpi 1997Jake BundokNessuna valutazione finora

- CPAR Auditing TheoryDocumento62 pagineCPAR Auditing TheoryKeannu Lewis Vidallo96% (46)

- New Zealand Best, Indonesia Worst in World Poll of International CorruptionDocumento10 pagineNew Zealand Best, Indonesia Worst in World Poll of International CorruptionNasir JamalNessuna valutazione finora

- Cpi 1996Documento9 pagineCpi 1996Jake BundokNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- SOX On ISDocumento5 pagineSOX On ISJake BundokNessuna valutazione finora

- GuideDocumento4 pagineGuideJake BundokNessuna valutazione finora

- The Positive and Negative Sides of Incessant Asuu Strikes in Nigeria: An Exploratory Study Based On Academic Staff PerceptionsDocumento11 pagineThe Positive and Negative Sides of Incessant Asuu Strikes in Nigeria: An Exploratory Study Based On Academic Staff PerceptionspetrolumideNessuna valutazione finora

- A Study On Dealers Perception Towards Asbestos Cement Sheets Mba ProjectDocumento86 pagineA Study On Dealers Perception Towards Asbestos Cement Sheets Mba ProjectPrarthana Srinivasan40% (5)

- 0 GSIS Finals QuestionsDocumento11 pagine0 GSIS Finals QuestionsClauds GadzzNessuna valutazione finora

- Shareholders & StakehodersDocumento9 pagineShareholders & StakehodersresharofifahutoroNessuna valutazione finora

- Final Report On SME and Micro Credit and Micro FinanceDocumento65 pagineFinal Report On SME and Micro Credit and Micro FinanceMohammad SumonNessuna valutazione finora

- Memo To SupervisorDocumento2 pagineMemo To SupervisorArem Capuli100% (2)

- HRM ScriptDocumento4 pagineHRM ScriptRachel Ann RazonableNessuna valutazione finora

- Effects of Wage DiscriminationDocumento15 pagineEffects of Wage DiscriminationJorge Reyes ManzanoNessuna valutazione finora

- HR Practices in Construction IndustryDocumento9 pagineHR Practices in Construction IndustryVijay Baskar S0% (1)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- HCM US Balance Adjustments White PaperDocumento184 pagineHCM US Balance Adjustments White Paperajay kumarNessuna valutazione finora

- Nebosh 1 2 Moral Social and EconomicDocumento28 pagineNebosh 1 2 Moral Social and EconomicMuhammadObaidullahNessuna valutazione finora

- Philippine AirlinesDocumento6 paginePhilippine AirlinesammeNessuna valutazione finora

- Salman BDADocumento7 pagineSalman BDAATIF HASANNessuna valutazione finora

- SRS FormDocumento2 pagineSRS FormJerz PortNessuna valutazione finora

- J21 1RSDocumento169 pagineJ21 1RSferdinandventNessuna valutazione finora

- Eobi Act 1976Documento43 pagineEobi Act 1976shahidtoor175% (4)

- Caste & Class in Bihar-Anand ChakravartyDocumento15 pagineCaste & Class in Bihar-Anand Chakravartyletterstomukesh0% (1)

- Agrarian Law and Social Legislation NotesDocumento18 pagineAgrarian Law and Social Legislation Notesmcris101Nessuna valutazione finora

- Assignment ComtempoararyDocumento17 pagineAssignment Comtempoararyhoney balolongNessuna valutazione finora

- PIDE, Internship Report FormatDocumento7 paginePIDE, Internship Report FormatMalik YasirNessuna valutazione finora

- Manalo V TNSDocumento14 pagineManalo V TNSyousirneighmNessuna valutazione finora

- Pepsi CoDocumento10 paginePepsi CoTainosavageNessuna valutazione finora

- LABREL Full Text - 1st HWDocumento104 pagineLABREL Full Text - 1st HWIanBiagtanNessuna valutazione finora

- NSDC Scheme For Market LED Fee Based Program 18052022Documento13 pagineNSDC Scheme For Market LED Fee Based Program 18052022Niranjan KaushikNessuna valutazione finora

- Multiple Choice: Employee Training and DevelopmentDocumento12 pagineMultiple Choice: Employee Training and DevelopmentSadaf WaheedNessuna valutazione finora

- Campus Recruitment TrainingDocumento4 pagineCampus Recruitment TrainingSagar Paul'gNessuna valutazione finora

- Competency MappingDocumento31 pagineCompetency MappingKirti Sangwan100% (1)

- Technical English 3 Homework 3 2023Documento3 pagineTechnical English 3 Homework 3 2023Efrain De GraciaNessuna valutazione finora

- Princeton, New JerseyDocumento16 paginePrinceton, New JerseyJiabin LiNessuna valutazione finora

- Paid Family LeaveDocumento5 paginePaid Family LeaveDimitri SpanosNessuna valutazione finora

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisDa EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisValutazione: 5 su 5 stelle5/5 (6)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successDa EverandReady, Set, Growth hack:: A beginners guide to growth hacking successValutazione: 4.5 su 5 stelle4.5/5 (93)

- Finance Basics (HBR 20-Minute Manager Series)Da EverandFinance Basics (HBR 20-Minute Manager Series)Valutazione: 4.5 su 5 stelle4.5/5 (32)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNDa Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNValutazione: 4.5 su 5 stelle4.5/5 (3)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDa EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaValutazione: 4.5 su 5 stelle4.5/5 (14)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetDa EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetValutazione: 5 su 5 stelle5/5 (2)