Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (894)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- MGNT 3430 Homework Answers for Operations ManagementDocumento4 pagineMGNT 3430 Homework Answers for Operations ManagementKeron TzulNessuna valutazione finora

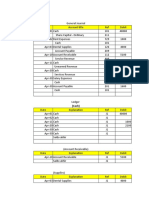

- Post-Closing Trial BalanceDocumento5 paginePost-Closing Trial BalanceIsaac RiñaNessuna valutazione finora

- CH 1 Introduction To StatisticsDocumento14 pagineCH 1 Introduction To Statisticsসাঈদ আহমদNessuna valutazione finora

- Stat NU Question 190-208Documento19 pagineStat NU Question 190-208সাঈদ আহমদNessuna valutazione finora

- CH 11 Leve+CS 22Documento1 paginaCH 11 Leve+CS 22সাঈদ আহমদNessuna valutazione finora

- National University: SyllabusDocumento9 pagineNational University: Syllabusসাঈদ আহমদNessuna valutazione finora

- CH 9 Competetion Act Final 582-603Documento23 pagineCH 9 Competetion Act Final 582-603সাঈদ আহমদNessuna valutazione finora

- Principles of AccountingDocumento1 paginaPrinciples of Accountingসাঈদ আহমদNessuna valutazione finora

- Mikvwi Av KK Gvngy' K JR, Rvgvjcyi - : Wkÿke 'I Z - WeeiyxDocumento2 pagineMikvwi Av KK Gvngy' K JR, Rvgvjcyi - : Wkÿke 'I Z - Weeiyxসাঈদ আহমদNessuna valutazione finora

- Bba Prof 2010Documento2 pagineBba Prof 2010সাঈদ আহমদNessuna valutazione finora

- CH 3.3 Errors - SDocumento10 pagineCH 3.3 Errors - Sসাঈদ আহমদ0% (1)

- CH 3.1 Tabular Analysis - SDocumento14 pagineCH 3.1 Tabular Analysis - Sসাঈদ আহমদ100% (2)

- Correlation Correlation Correlation Correlation: Karl Pearson's MethodDocumento2 pagineCorrelation Correlation Correlation Correlation: Karl Pearson's Methodসাঈদ আহমদNessuna valutazione finora

- History of MathsDocumento10 pagineHistory of Mathsসাঈদ আহমদNessuna valutazione finora

- Logarithms Formulas: Jmvwi'GtDocumento2 pagineLogarithms Formulas: Jmvwi'Gtসাঈদ আহমদNessuna valutazione finora

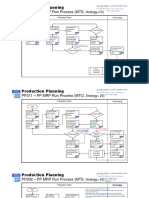

- Production Planning MRP Run ProcessesDocumento6 pagineProduction Planning MRP Run Processesdnsptra_580883023Nessuna valutazione finora

- Financial Authorisations OverviewDocumento1.707 pagineFinancial Authorisations OverviewbathinisridharNessuna valutazione finora

- Tipo S Movimento SapDocumento3 pagineTipo S Movimento Sapruiforever0% (1)

- Bank Reconciliation Statement for August 2011Documento29 pagineBank Reconciliation Statement for August 2011CRITICAL GAMERNessuna valutazione finora

- Pasir Putih 1 31/03/22Documento18 paginePasir Putih 1 31/03/22Evonne L YKNessuna valutazione finora

- Chapter 14 Supply Chain ManagementDocumento46 pagineChapter 14 Supply Chain ManagementAmna KhanNessuna valutazione finora

- GWS - PH - PL - WHT Report v2 PDFDocumento328 pagineGWS - PH - PL - WHT Report v2 PDFBRYAN SUMOOKNessuna valutazione finora

- Maybank Islamic account statement summaryDocumento18 pagineMaybank Islamic account statement summaryAdeela fazlinNessuna valutazione finora

- Brand ManagementDocumento8 pagineBrand Managementanon-132404Nessuna valutazione finora

- General Journal Entries for Purchases and PaymentsDocumento17 pagineGeneral Journal Entries for Purchases and PaymentsZULFA SYAMNessuna valutazione finora

- Variable Costing ConceptsDocumento10 pagineVariable Costing Conceptsrodell pabloNessuna valutazione finora

- The Impact of ERP On Supply Chain Management - Exploratory Findings From A European Delphi Study PDFDocumento18 pagineThe Impact of ERP On Supply Chain Management - Exploratory Findings From A European Delphi Study PDFshipra177Nessuna valutazione finora

- Cim B ClicksDocumento8 pagineCim B ClicksSuguna MYSDNessuna valutazione finora

- Soal Praktek Myob Perusahaan JasaDocumento4 pagineSoal Praktek Myob Perusahaan Jasahani ramadiyantiNessuna valutazione finora

- Chapter 7 Review AnswersDocumento3 pagineChapter 7 Review AnswersShane Khezia BaclayonNessuna valutazione finora

- S Alyssa 2021Documento6 pagineS Alyssa 2021aamir hayatNessuna valutazione finora

- Introduction to Logistics Management and Supply ChainDocumento115 pagineIntroduction to Logistics Management and Supply ChainSachin PatilNessuna valutazione finora

- Business StrategiesDocumento24 pagineBusiness StrategiesJohn Patrick Lazaro AndresNessuna valutazione finora

- Acquisition and Payment CycleDocumento19 pagineAcquisition and Payment CycleE-kel Anico Jaurigue67% (3)

- Introduction For Scs Supplier Collaboration SystemDocumento16 pagineIntroduction For Scs Supplier Collaboration SystemAwojobi Alexander Habeeb OloladeNessuna valutazione finora

- Cost Accounting - Chapter - 5Documento5 pagineCost Accounting - Chapter - 5xxxxxxxxxNessuna valutazione finora

- Demo of CamDocumento39 pagineDemo of CamMahima ChaudharyNessuna valutazione finora

- Supply ChainDocumento38 pagineSupply ChainMk YapNessuna valutazione finora

- Chapter-20 Inventory ManagementDocumento20 pagineChapter-20 Inventory ManagementPooja SheoranNessuna valutazione finora

- Strategic EntrepreneurshipDocumento16 pagineStrategic Entrepreneurshipnasuha50% (2)

- R13.17D Financial OTBI Index ColumnsDocumento224 pagineR13.17D Financial OTBI Index ColumnsNabeel RashidNessuna valutazione finora

- AIKEZ Retail Store General Journal For The Month of January 2021 Date Particulars F Debit CreditDocumento20 pagineAIKEZ Retail Store General Journal For The Month of January 2021 Date Particulars F Debit CreditHasanah AmerilNessuna valutazione finora

- Pembahasan Contoh Soal Matrikulasi Day 2Documento5 paginePembahasan Contoh Soal Matrikulasi Day 2valdaNessuna valutazione finora