Potrebbero piacerti anche

- Arlington Value 2006 Annual Shareholder LetterDocumento5 pagineArlington Value 2006 Annual Shareholder LetterSmitty WNessuna valutazione finora

- Stay Rich with a Balanced Portfolio: The Price You Pay for Peace of MindDa EverandStay Rich with a Balanced Portfolio: The Price You Pay for Peace of MindValutazione: 3 su 5 stelle3/5 (1)

- The Future of Common Stocks Benjamin Graham PDFDocumento8 pagineThe Future of Common Stocks Benjamin Graham PDFPrashant AgarwalNessuna valutazione finora

- Understanding the different levels of investing as a gameDocumento11 pagineUnderstanding the different levels of investing as a gamePradeep RaghunathanNessuna valutazione finora

- Anon - Housing Thesis 09 12 2011Documento22 pagineAnon - Housing Thesis 09 12 2011cnm3dNessuna valutazione finora

- Teledyne and Henry Singleton A CS of A Great Capital AllocatorDocumento34 pagineTeledyne and Henry Singleton A CS of A Great Capital Allocatorp_rishi_2000Nessuna valutazione finora

- Klarman WorryingDocumento2 pagineKlarman WorryingSudhanshuNessuna valutazione finora

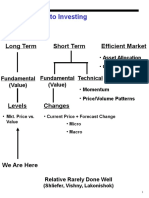

- Approaches To Investing: Long Term Short Term Efficient MarketDocumento71 pagineApproaches To Investing: Long Term Short Term Efficient MarketPeter WarmeNessuna valutazione finora

- Aquamarine - 2013Documento84 pagineAquamarine - 2013sb86Nessuna valutazione finora

- EV The Price of A BusinessDocumento11 pagineEV The Price of A BusinessseadwellerNessuna valutazione finora

- Investing Without PeopleDocumento18 pagineInvesting Without PeopleZerohedgeNessuna valutazione finora

- Tiananmen Square To Wall Street - ArticleDocumento3 pagineTiananmen Square To Wall Street - ArticleGabe FarajollahNessuna valutazione finora

- Buffett On Valuation PDFDocumento7 pagineBuffett On Valuation PDFvinaymathew100% (1)

- BerkshireHandout2012Final 0 PDFDocumento4 pagineBerkshireHandout2012Final 0 PDFHermes TristemegistusNessuna valutazione finora

- Ruane Cunniff Sequoia Fund Annual LetterDocumento29 pagineRuane Cunniff Sequoia Fund Annual Letterrwmortell3580Nessuna valutazione finora

- Spinoff Investing Checklist: - Greggory Miller, Author of Spinoff Investing Simplified Available OnDocumento2 pagineSpinoff Investing Checklist: - Greggory Miller, Author of Spinoff Investing Simplified Available OnmikiNessuna valutazione finora

- Profit Guru Bill NygrenDocumento5 pagineProfit Guru Bill NygrenekramcalNessuna valutazione finora

- The Art of Stock PickingDocumento13 pagineThe Art of Stock PickingRonald MirandaNessuna valutazione finora

- Acumen Phil Fisher 1.0Documento16 pagineAcumen Phil Fisher 1.0Vishwanath PuthranNessuna valutazione finora

- Great CEOs Compilation by @geordiejobDocumento218 pagineGreat CEOs Compilation by @geordiejobndzapakNessuna valutazione finora

- Creighton Value Investing PanelDocumento9 pagineCreighton Value Investing PanelbenclaremonNessuna valutazione finora

- Notes From A Seth Klarman MBA LectureDocumento5 pagineNotes From A Seth Klarman MBA LecturePIYUSH GOPALNessuna valutazione finora

- Sees Candy SchroederDocumento15 pagineSees Candy SchroederAAOI2Nessuna valutazione finora

- Coho Capital Letter Highlights Self-Reinforcing Business Models in TechDocumento13 pagineCoho Capital Letter Highlights Self-Reinforcing Business Models in TechraissakisNessuna valutazione finora

- Free Cash Flow Investing 04-18-11Documento6 pagineFree Cash Flow Investing 04-18-11lowbankNessuna valutazione finora

- The Nifty Fifty - Joe Kusnan's BlogDocumento2 pagineThe Nifty Fifty - Joe Kusnan's BlogPradeep RaghunathanNessuna valutazione finora

- Private Debt Investor Special ReportDocumento7 paginePrivate Debt Investor Special ReportB.C. MoonNessuna valutazione finora

- Mick McGuire Value Investing Congress Presentation Marcato Capital ManagementDocumento70 pagineMick McGuire Value Investing Congress Presentation Marcato Capital Managementmarketfolly.comNessuna valutazione finora

- Scion 2006 4q Rmbs Cds Primer and FaqDocumento8 pagineScion 2006 4q Rmbs Cds Primer and FaqsabishiiNessuna valutazione finora

- Distressed Debt InvestingDocumento5 pagineDistressed Debt Investingjt322Nessuna valutazione finora

- Focus InvestorDocumento5 pagineFocus Investora65b66inc7288Nessuna valutazione finora

- VALUEx Vail 2014 - Visa PresentationDocumento19 pagineVALUEx Vail 2014 - Visa PresentationVitaliyKatsenelson100% (1)

- Print Article on Value Investor Seth KlarmanDocumento2 paginePrint Article on Value Investor Seth KlarmanBolsheviceNessuna valutazione finora

- Marcato Capital 4Q14 Letter To InvestorsDocumento38 pagineMarcato Capital 4Q14 Letter To InvestorsValueWalk100% (1)

- Reading List J Montier 2008-06-16Documento12 pagineReading List J Montier 2008-06-16rodmorley100% (2)

- Summary New Venture ManagementDocumento57 pagineSummary New Venture Managementbetter.bambooNessuna valutazione finora

- 9 - Case Shopping MallDocumento11 pagine9 - Case Shopping MallRdx ProNessuna valutazione finora

- Schloss 1995Documento2 pagineSchloss 1995Logic Gate Capital100% (3)

- Charlie Rose Warren Buffett InterviewDocumento20 pagineCharlie Rose Warren Buffett InterviewkayeskowsikNessuna valutazione finora

- RV Capital June 2015 LetterDocumento8 pagineRV Capital June 2015 LetterCanadianValueNessuna valutazione finora

- Value Investing Opportunities in Korea (Presentation by Petra)Documento49 pagineValue Investing Opportunities in Korea (Presentation by Petra)Mike ChangNessuna valutazione finora

- The Beekeepers' Guide to Investing: Focusing on Business Fundamentals Over Emotions in Volatile MarketsDocumento13 pagineThe Beekeepers' Guide to Investing: Focusing on Business Fundamentals Over Emotions in Volatile Marketscrees25Nessuna valutazione finora

- Nick Train The King of Buy and Hold PDFDocumento13 pagineNick Train The King of Buy and Hold PDFJohn Hadriano Mellon FundNessuna valutazione finora

- Words From The Wise Charles Ellis On Confronting Investing ChallengesDocumento23 pagineWords From The Wise Charles Ellis On Confronting Investing ChallengesFrederico DimarzioNessuna valutazione finora

- Interviews Value Investing Guru Roger Montgomery About ValueableDocumento3 pagineInterviews Value Investing Guru Roger Montgomery About Valueableqwerqwer123100% (1)

- East Coast Asset Management (Q4 2009) Investor LetterDocumento10 pagineEast Coast Asset Management (Q4 2009) Investor Lettermarketfolly.comNessuna valutazione finora

- Who Is On The Other Side?: Antti IlmanenDocumento65 pagineWho Is On The Other Side?: Antti IlmanenaptenodyteNessuna valutazione finora

- 1976 Buffett Letter About Geico - FutureBlindDocumento4 pagine1976 Buffett Letter About Geico - FutureBlindPradeep RaghunathanNessuna valutazione finora

- Small CapsDocumento4 pagineSmall CapscdietzrNessuna valutazione finora

- Ruane, Cunniff Investor Day 2016Documento25 pagineRuane, Cunniff Investor Day 2016superinvestorbulletiNessuna valutazione finora

- Notes John Burbank, Passport at University of Texas, UTIMCODocumento2 pagineNotes John Burbank, Passport at University of Texas, UTIMCOHedge Fund ConversationsNessuna valutazione finora

- 10 "The Rediscovered Benjamin Graham"Documento6 pagine10 "The Rediscovered Benjamin Graham"X.r. GeNessuna valutazione finora

- Ben Stein - Leg Up On The MarketDocumento8 pagineBen Stein - Leg Up On The MarketMarc F. DemshockNessuna valutazione finora

- Investing in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketDa EverandInvesting in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketNessuna valutazione finora

- Financial Fine Print: Uncovering a Company's True ValueDa EverandFinancial Fine Print: Uncovering a Company's True ValueValutazione: 3 su 5 stelle3/5 (3)

- Raising the Bar: Integrity and Passion in Life and Business: The Story of Clif Bar Inc.Da EverandRaising the Bar: Integrity and Passion in Life and Business: The Story of Clif Bar Inc.Valutazione: 3.5 su 5 stelle3.5/5 (15)

- Strategic and Tactical Asset Allocation: An Integrated ApproachDa EverandStrategic and Tactical Asset Allocation: An Integrated ApproachNessuna valutazione finora

- Are You Smarter Than A 7th Grader (Notes)Documento37 pagineAre You Smarter Than A 7th Grader (Notes)Broyhill Asset ManagementNessuna valutazione finora

- The Grave Dancer Sam ZellDocumento5 pagineThe Grave Dancer Sam ZellValueWalk100% (2)

- Lumber Liquidators Presentation-Whitney Tilson-11!22!13Documento27 pagineLumber Liquidators Presentation-Whitney Tilson-11!22!13CanadianValueNessuna valutazione finora

- Broyhill Letter (Q2-08)Documento3 pagineBroyhill Letter (Q2-08)Broyhill Asset ManagementNessuna valutazione finora

- Solid As An OAKDocumento32 pagineSolid As An OAKBroyhill Asset ManagementNessuna valutazione finora

- Rational Investing in Irrational MarketsDocumento70 pagineRational Investing in Irrational MarketsBroyhill Asset ManagementNessuna valutazione finora

- HSP Thesis (May-13)Documento17 pagineHSP Thesis (May-13)Broyhill Asset ManagementNessuna valutazione finora

- The Broyhill Letter: Executive SummaryDocumento3 pagineThe Broyhill Letter: Executive SummaryBroyhill Asset ManagementNessuna valutazione finora

- Put Me in Coach!!Documento22 paginePut Me in Coach!!Broyhill Asset ManagementNessuna valutazione finora

- The Broyhill Letter: Executive SummaryDocumento4 pagineThe Broyhill Letter: Executive SummaryBroyhill Asset ManagementNessuna valutazione finora

- CCH Thesis (Dec-12)Documento16 pagineCCH Thesis (Dec-12)Broyhill Asset ManagementNessuna valutazione finora

- Broyhill Letter (Q2-08)Documento3 pagineBroyhill Letter (Q2-08)Broyhill Asset ManagementNessuna valutazione finora

- The Broyhill Letter - Part Duex (Q2-11)Documento5 pagineThe Broyhill Letter - Part Duex (Q2-11)Broyhill Asset ManagementNessuna valutazione finora

- Broyhill Letter (Aug-12)Documento8 pagineBroyhill Letter (Aug-12)Broyhill Asset ManagementNessuna valutazione finora

- A Brief Update On Portfolio Strategy (Nov-12)Documento8 pagineA Brief Update On Portfolio Strategy (Nov-12)Broyhill Asset ManagementNessuna valutazione finora

- The Broyhill Letter (Q4-10)Documento7 pagineThe Broyhill Letter (Q4-10)Broyhill Asset ManagementNessuna valutazione finora

- Broyhill Letter (Oct-12)Documento8 pagineBroyhill Letter (Oct-12)Broyhill Asset ManagementNessuna valutazione finora

- Bienville US Housing (May 2012)Documento23 pagineBienville US Housing (May 2012)Broyhill Asset ManagementNessuna valutazione finora

- Dept of Commerce Preliminary Finding of CVDDocumento9 pagineDept of Commerce Preliminary Finding of CVDBroyhill Asset ManagementNessuna valutazione finora

- Easy Money (Nov-11)Documento37 pagineEasy Money (Nov-11)Broyhill Asset ManagementNessuna valutazione finora

- The Broyhill Letter (Q2-11)Documento6 pagineThe Broyhill Letter (Q2-11)Broyhill Asset ManagementNessuna valutazione finora

- The Broyhill Letter (Q3-11)Documento7 pagineThe Broyhill Letter (Q3-11)Broyhill Asset ManagementNessuna valutazione finora

- Investing Between Crises (Jun-11)Documento53 pagineInvesting Between Crises (Jun-11)Broyhill Asset ManagementNessuna valutazione finora

- Shorting Congress - Commentary & Strategy (January 2011)Documento6 pagineShorting Congress - Commentary & Strategy (January 2011)Broyhill Asset ManagementNessuna valutazione finora

- The Broyhill Letter (Q1-11)Documento7 pagineThe Broyhill Letter (Q1-11)Broyhill Asset ManagementNessuna valutazione finora

- Tis Mir 01.05.10Documento3 pagineTis Mir 01.05.10Broyhill Asset ManagementNessuna valutazione finora

- Broyhill Portfolio Strategy (Apr-11)Documento42 pagineBroyhill Portfolio Strategy (Apr-11)Broyhill Asset ManagementNessuna valutazione finora

- The Great 'Flation Debate (Nov-10)Documento33 pagineThe Great 'Flation Debate (Nov-10)Broyhill Asset ManagementNessuna valutazione finora

- LL - Mama Said Knock You OutDocumento17 pagineLL - Mama Said Knock You OutBroyhill Asset ManagementNessuna valutazione finora

- 2020-08-31 - Best Practices For Electrifying Rural Health Facilities - FinalDocumento54 pagine2020-08-31 - Best Practices For Electrifying Rural Health Facilities - FinalAdedimeji FredNessuna valutazione finora

- Statement of Account: Locked Bag 980 Milsons Point NSW 1565Documento9 pagineStatement of Account: Locked Bag 980 Milsons Point NSW 1565Tyler LindsayNessuna valutazione finora

- Track monthly expenses and income in a budget spreadsheetDocumento4 pagineTrack monthly expenses and income in a budget spreadsheetTa Tran100% (1)

- (2013 Pattern) PDFDocumento77 pagine(2013 Pattern) PDFamNessuna valutazione finora

- Proposal of HBLDocumento52 pagineProposal of HBLashuuu143100% (1)

- Revenue Regulations No. 02-40Documento46 pagineRevenue Regulations No. 02-40zelayneNessuna valutazione finora

- PDF - Unpacking LRC and LIC Calculations For PC InsurersDocumento14 paginePDF - Unpacking LRC and LIC Calculations For PC Insurersnod32_1206Nessuna valutazione finora

- Focus4 2E Unit Test Vocabulary Grammar UoE Unit4 GroupA B ANSWERSDocumento1 paginaFocus4 2E Unit Test Vocabulary Grammar UoE Unit4 GroupA B ANSWERSHalil B67% (3)

- Semester 1 of The 2019-2020 Academic Session (September 2019)Documento3 pagineSemester 1 of The 2019-2020 Academic Session (September 2019)Ct HajarNessuna valutazione finora

- Sashaevdakov 5cents On Life1Documento142 pagineSashaevdakov 5cents On Life1abcdNessuna valutazione finora

- Anglais 1Documento3 pagineAnglais 1idilmiNessuna valutazione finora

- Protect Against Rising Rates With CapsDocumento13 pagineProtect Against Rising Rates With Capsz_k_j_vNessuna valutazione finora

- Dividend Discount Model - Commercial Bank Valuation (FIG)Documento2 pagineDividend Discount Model - Commercial Bank Valuation (FIG)Sanjay RathiNessuna valutazione finora

- Meet Your Strawman: Let's Have A Little QuizDocumento50 pagineMeet Your Strawman: Let's Have A Little Quizwereld2all100% (3)

- PBD Cluster 27Documento48 paginePBD Cluster 27Datu Puwa MamalacNessuna valutazione finora

- Costco Connection 201301Documento129 pagineCostco Connection 201301kexxuNessuna valutazione finora

- Ann Reyes General LedgersDocumento4 pagineAnn Reyes General LedgersDianeNessuna valutazione finora

- Ministry of Finance and Financiel Services Joint Communiqué On Mauritius LeaksDocumento4 pagineMinistry of Finance and Financiel Services Joint Communiqué On Mauritius LeaksION NewsNessuna valutazione finora

- Organizational Study at Sunshare InvestmentsDocumento48 pagineOrganizational Study at Sunshare Investmentsguddi kumari0% (1)

- Truth in Lending Act (Ayn Ruth Notes)Documento3 pagineTruth in Lending Act (Ayn Ruth Notes)Ayn Ruth Zambrano TolentinoNessuna valutazione finora

- RMC No. 18-2021Documento2 pagineRMC No. 18-2021Marvin Coming MoldeNessuna valutazione finora

- 1 STND Cost Calculation CK11N and CK24 - PPC1 & ZPC2Documento15 pagine1 STND Cost Calculation CK11N and CK24 - PPC1 & ZPC2Mohammad Aarif100% (1)

- Statement 20140508Documento2 pagineStatement 20140508franraizerNessuna valutazione finora

- Enron Scandal - Wikipedia, The Free EncyclopediaDocumento31 pagineEnron Scandal - Wikipedia, The Free Encyclopediazhyldyz_88Nessuna valutazione finora

- Tugas Pajak InternasionalDocumento3 pagineTugas Pajak Internasionalthapin RfNessuna valutazione finora

- CFO VP Finance Project Controls Engineer in Morristown NJ Resume Matthew GentileDocumento2 pagineCFO VP Finance Project Controls Engineer in Morristown NJ Resume Matthew GentileMatthewGentileNessuna valutazione finora

- Chinese Silver Standard EconomyDocumento24 pagineChinese Silver Standard Economyage0925Nessuna valutazione finora

- AC1025 Mock Exam Comm 2017Documento17 pagineAC1025 Mock Exam Comm 2017Nghia Tuan NghiaNessuna valutazione finora

- Trading Account PDFDocumento9 pagineTrading Account PDFVijayaraj Jeyabalan100% (1)

- Case Studies On HR Best PracticesDocumento50 pagineCase Studies On HR Best PracticesAnkur SharmaNessuna valutazione finora