Potrebbero piacerti anche

- Wei 20150904 PDFDocumento18 pagineWei 20150904 PDFRandora LkNessuna valutazione finora

- Weekly Foreign Holding & Block Trade Update: Net Buying Net SellingDocumento4 pagineWeekly Foreign Holding & Block Trade Update: Net Buying Net SellingRandora LkNessuna valutazione finora

- Weekly Update 04.09.2015 PDFDocumento2 pagineWeekly Update 04.09.2015 PDFRandora LkNessuna valutazione finora

- Daily 01 09 2015 PDFDocumento4 pagineDaily 01 09 2015 PDFRandora LkNessuna valutazione finora

- 03 September 2015 PDFDocumento9 pagine03 September 2015 PDFRandora LkNessuna valutazione finora

- Global Market Update - 04 09 2015 PDFDocumento6 pagineGlobal Market Update - 04 09 2015 PDFRandora LkNessuna valutazione finora

- Global Market Update - 04 09 2015 PDFDocumento6 pagineGlobal Market Update - 04 09 2015 PDFRandora LkNessuna valutazione finora

- Sri0Lanka000Re0ounting0and0auditing PDFDocumento44 pagineSri0Lanka000Re0ounting0and0auditing PDFRandora LkNessuna valutazione finora

- Earnings Update March Quarter 2015 05 06 2015 PDFDocumento24 pagineEarnings Update March Quarter 2015 05 06 2015 PDFRandora LkNessuna valutazione finora

- Press 20150831ebDocumento2 paginePress 20150831ebRandora LkNessuna valutazione finora

- ICRA Lanka Assigns (SL) BBB-rating With Positive Outlook To Sanasa Development Bank PLCDocumento3 pagineICRA Lanka Assigns (SL) BBB-rating With Positive Outlook To Sanasa Development Bank PLCRandora LkNessuna valutazione finora

- Earnings & Market Returns Forecast - Jun 2015 PDFDocumento4 pagineEarnings & Market Returns Forecast - Jun 2015 PDFRandora LkNessuna valutazione finora

- Press 20150831ea PDFDocumento1 paginaPress 20150831ea PDFRandora LkNessuna valutazione finora

- CCPI - Press Release - August2015 PDFDocumento5 pagineCCPI - Press Release - August2015 PDFRandora LkNessuna valutazione finora

- Results Update Sector Summary - Jun 2015 PDFDocumento2 pagineResults Update Sector Summary - Jun 2015 PDFRandora LkNessuna valutazione finora

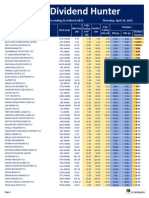

- Dividend Hunter - Mar 2015 PDFDocumento7 pagineDividend Hunter - Mar 2015 PDFRandora LkNessuna valutazione finora

- Results Update For All Companies - Jun 2015 PDFDocumento9 pagineResults Update For All Companies - Jun 2015 PDFRandora LkNessuna valutazione finora

- Dividend Hunter - Apr 2015 PDFDocumento7 pagineDividend Hunter - Apr 2015 PDFRandora LkNessuna valutazione finora

- BRS Monthly (March 2015 Edition) PDFDocumento8 pagineBRS Monthly (March 2015 Edition) PDFRandora LkNessuna valutazione finora

- Dividend Hunter - Mar 2015 PDFDocumento7 pagineDividend Hunter - Mar 2015 PDFRandora LkNessuna valutazione finora

- Daily - 23 04 2015 PDFDocumento4 pagineDaily - 23 04 2015 PDFRandora LkNessuna valutazione finora

- The Morality of Capitalism Sri LankiaDocumento32 pagineThe Morality of Capitalism Sri LankiaRandora LkNessuna valutazione finora

- N D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Documento5 pagineN D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Randora LkNessuna valutazione finora

- CRL Corporate Update - 22 04 2015 - Upgrade To A Strong BUY PDFDocumento12 pagineCRL Corporate Update - 22 04 2015 - Upgrade To A Strong BUY PDFRandora LkNessuna valutazione finora

- Janashakthi Insurance Company PLC - (JINS) - Q4 FY 14 - SELL PDFDocumento9 pagineJanashakthi Insurance Company PLC - (JINS) - Q4 FY 14 - SELL PDFRandora LkNessuna valutazione finora

- Chevron Lubricants Lanka PLC (LLUB) - Q4 FY 14 - SELL PDFDocumento9 pagineChevron Lubricants Lanka PLC (LLUB) - Q4 FY 14 - SELL PDFRandora LkNessuna valutazione finora

- Microfinance Regulatory Model PDFDocumento5 pagineMicrofinance Regulatory Model PDFRandora LkNessuna valutazione finora

- Daily Stock Watch 08.04.2015 PDFDocumento9 pagineDaily Stock Watch 08.04.2015 PDFRandora LkNessuna valutazione finora

- GIH Capital Monthly - Mar 2015 PDFDocumento11 pagineGIH Capital Monthly - Mar 2015 PDFRandora LkNessuna valutazione finora

- Weekly Foreign Holding & Block Trade Update - 02 04 2015 PDFDocumento4 pagineWeekly Foreign Holding & Block Trade Update - 02 04 2015 PDFRandora LkNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Solar TimeDocumento28 pagineSolar TimeArdi KotoNessuna valutazione finora

- Bus Bar Sizing Calculation For SubstatioDocumento11 pagineBus Bar Sizing Calculation For SubstatioMuhammad AdeelNessuna valutazione finora

- Technial Date SheetDocumento1 paginaTechnial Date SheetYeco MachineryNessuna valutazione finora

- Ho-SolarToday-April13 - v2Documento4 pagineHo-SolarToday-April13 - v2Danny Sánchez YánezNessuna valutazione finora

- John Dirk Walecka - Introduction To Classical Mechanics-WSPC (2020)Documento184 pagineJohn Dirk Walecka - Introduction To Classical Mechanics-WSPC (2020)Saiyad AliNessuna valutazione finora

- RCC RESO 20 06 - (Central - Scheduling) PDFDocumento57 pagineRCC RESO 20 06 - (Central - Scheduling) PDFSherwin SabandoNessuna valutazione finora

- InstrumentationDocumento7 pagineInstrumentationEmmanuel Enriquez0% (1)

- EASAQUESTIONPAPERS BLOGSPOT PART 66 MODULE 7 PART 3Documento15 pagineEASAQUESTIONPAPERS BLOGSPOT PART 66 MODULE 7 PART 3Ye Min OoNessuna valutazione finora

- اسئلة بيئة ةعمارة ت1 ك2-signedDocumento1 paginaاسئلة بيئة ةعمارة ت1 ك2-signedAli AlibrahimiNessuna valutazione finora

- Rock Eval 6Documento24 pagineRock Eval 6Mukul GoyalNessuna valutazione finora

- Specifying Windows and Doors Using Performance StandardsDocumento78 pagineSpecifying Windows and Doors Using Performance StandardsghadasaudiNessuna valutazione finora

- CSP Team 2 (1) Modify PDFDocumento29 pagineCSP Team 2 (1) Modify PDFPranay ChalumuriNessuna valutazione finora

- Acura TSX 2004 Electronic Throttle Control SystemDocumento89 pagineAcura TSX 2004 Electronic Throttle Control Systemjorge antonio guillen100% (1)

- Practice Problems On Air Conditioning SystemDocumento1 paginaPractice Problems On Air Conditioning Systemsushil.vgiNessuna valutazione finora

- Moving Coil GalvanometerDocumento5 pagineMoving Coil GalvanometerGauri Sakaria100% (2)

- ReportFileDocumento31 pagineReportFileRohan MehtaNessuna valutazione finora

- Role of Acoustics in Curtain Wall DesignDocumento77 pagineRole of Acoustics in Curtain Wall DesignbatteekhNessuna valutazione finora

- METHER1 - Machine Problems 2 PDFDocumento2 pagineMETHER1 - Machine Problems 2 PDFJhon Lhoyd CorpuzNessuna valutazione finora

- UC3842 Inside SchematicsDocumento17 pagineUC3842 Inside Schematicsp.c100% (1)

- Low Cost Housing: Ar. Yatra SharmaDocumento28 pagineLow Cost Housing: Ar. Yatra SharmaSaurav ShresthaNessuna valutazione finora

- Condair Gea Cairplus Gaisa Apstrades Iekartas Tehn Kat enDocumento36 pagineCondair Gea Cairplus Gaisa Apstrades Iekartas Tehn Kat enpolNessuna valutazione finora

- Building Code PDFDocumento227 pagineBuilding Code PDFBgee Lee100% (2)

- Essential Oils From Conventional To Green ExtractionDocumento13 pagineEssential Oils From Conventional To Green ExtractionNajihah RamliNessuna valutazione finora

- Manual Usuario Regal Raptot Daytona 350Documento48 pagineManual Usuario Regal Raptot Daytona 350cain985100% (1)

- Camphor BallsDocumento8 pagineCamphor BallsGurunath EpiliNessuna valutazione finora

- Sentra Aircon PDFDocumento98 pagineSentra Aircon PDFMed KevlarNessuna valutazione finora

- G Series 2-Cylinder Power PackageDocumento8 pagineG Series 2-Cylinder Power PackageIAN.SEMUT100% (1)

- 4368 PDFDocumento153 pagine4368 PDFAhmed AmirNessuna valutazione finora

- SA GuascorDocumento52 pagineSA GuascorcihanNessuna valutazione finora

- M3013-E Micropack 15 User ManuelDocumento54 pagineM3013-E Micropack 15 User ManuelhaizammNessuna valutazione finora