Potrebbero piacerti anche

- AGU POT Agrium Potash Merger Presentation Sept 2016Documento23 pagineAGU POT Agrium Potash Merger Presentation Sept 2016Ala BasterNessuna valutazione finora

- Guide to Contract Pricing: Cost and Price Analysis for Contractors, Subcontractors, and Government AgenciesDa EverandGuide to Contract Pricing: Cost and Price Analysis for Contractors, Subcontractors, and Government AgenciesNessuna valutazione finora

- Merger and AcquisitionDocumento19 pagineMerger and AcquisitionPaul Anthony AspuriaNessuna valutazione finora

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveDa EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNessuna valutazione finora

- Presentation Merger Siemens GamesaDocumento16 paginePresentation Merger Siemens GamesaRishab KothariNessuna valutazione finora

- Petroplus Overview (1.26.12)Documento15 paginePetroplus Overview (1.26.12)Chris BrunkNessuna valutazione finora

- DeGolyer & MacNaughton Reserve Report For Polvo FieldDocumento47 pagineDeGolyer & MacNaughton Reserve Report For Polvo FieldStan HollandNessuna valutazione finora

- Top Ten Natural Gas Producing Fields in AfricaDocumento6 pagineTop Ten Natural Gas Producing Fields in AfricaSalah ElbakkoushNessuna valutazione finora

- Joint Venture Agreement LPG TerminalDocumento5 pagineJoint Venture Agreement LPG TerminalMunir HussainNessuna valutazione finora

- Minimizing Operational Risk in Oil Gas IndustryDocumento12 pagineMinimizing Operational Risk in Oil Gas IndustryLogan JulienNessuna valutazione finora

- Terminologies in Petroleum IndustryDocumento7 pagineTerminologies in Petroleum Industryarvind_dwivedi100% (1)

- Key Credit Risks of Project FinanceDocumento12 pagineKey Credit Risks of Project FinanceDavid FreundNessuna valutazione finora

- Valuation of Aggregate Operations For Banking PurposesDocumento18 pagineValuation of Aggregate Operations For Banking PurposesRodrigo DavidNessuna valutazione finora

- Accounting For Differences in Oil and Gas AccountingDocumento6 pagineAccounting For Differences in Oil and Gas Accountingsharanabasappa baliger100% (1)

- Evaluating Developing New Prospects PTDI 0114 1Documento12 pagineEvaluating Developing New Prospects PTDI 0114 1Rajesh KumarNessuna valutazione finora

- Oil&Gas ReservesDocumento3 pagineOil&Gas ReservesCHANFLENessuna valutazione finora

- Valuing Using Industry MultiplesDocumento11 pagineValuing Using Industry MultiplesSabina BuzoiNessuna valutazione finora

- Oil and Gas Economic EvaluationDocumento4 pagineOil and Gas Economic EvaluationTemitope BelloNessuna valutazione finora

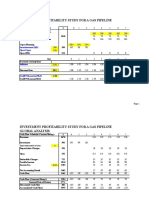

- Investment Profitability Study For A Gas Pipeline Global AnalysisDocumento6 pagineInvestment Profitability Study For A Gas Pipeline Global AnalysiskienlvNessuna valutazione finora

- Citigroup Alternative Investments Iapd BrochureDocumento91 pagineCitigroup Alternative Investments Iapd Brochureavers135Nessuna valutazione finora

- Hostess Disclosure StatementDocumento184 pagineHostess Disclosure StatementChapter 11 DocketsNessuna valutazione finora

- Banpu Analytical Disclosure Workshop Jun 2012Documento45 pagineBanpu Analytical Disclosure Workshop Jun 2012Vishan SharmaNessuna valutazione finora

- 2019-10-29 - Rhino Oil and Gas 350 ER - Scoping Report - Public Review-Executive SummaryDocumento13 pagine2019-10-29 - Rhino Oil and Gas 350 ER - Scoping Report - Public Review-Executive SummarySherebanu KajeeNessuna valutazione finora

- Manual For Discounting Oil and Gas IncomeDocumento9 pagineManual For Discounting Oil and Gas IncomeCarlota BellésNessuna valutazione finora

- Tethys Petroleum: Central Asia-Focused PlayerDocumento20 pagineTethys Petroleum: Central Asia-Focused PlayerRobin MillsNessuna valutazione finora

- Spe 59458 MSDocumento9 pagineSpe 59458 MSvaishnav2Nessuna valutazione finora

- Exxon Mobil Merger DetailsDocumento20 pagineExxon Mobil Merger DetailsPranay Chauhan100% (2)

- Qhse Prequalification QuestionnaireDocumento3 pagineQhse Prequalification QuestionnaireaymenmoatazNessuna valutazione finora

- July 2014Documento56 pagineJuly 2014Gas, Oil & Mining Contractor MagazineNessuna valutazione finora

- FiDocumento9 pagineFitahaalkibsiNessuna valutazione finora

- BP Investment AnalysisDocumento12 pagineBP Investment AnalysisAkinola WinfulNessuna valutazione finora

- Break Even For Oil & GasDocumento6 pagineBreak Even For Oil & GassultanthakurNessuna valutazione finora

- Key Ratios For Analyzing Oil and Gas Stocks: Measuring Performance - InvestopediaDocumento3 pagineKey Ratios For Analyzing Oil and Gas Stocks: Measuring Performance - Investopediapolobook3782Nessuna valutazione finora

- Ghana Petrol Tax Guide 2011Documento24 pagineGhana Petrol Tax Guide 2011William PyneNessuna valutazione finora

- SFR 20020831 LNGDocumento7 pagineSFR 20020831 LNGVidhu PrabhakarNessuna valutazione finora

- Developing Nigeria Oil and Gas Pipeline Using Multi-Criteria Decision Analysis (McdaDocumento8 pagineDeveloping Nigeria Oil and Gas Pipeline Using Multi-Criteria Decision Analysis (McdaRowland Adewumi100% (8)

- Fasb 69 Oil and Gas DisclosuresDocumento44 pagineFasb 69 Oil and Gas DisclosureslmccandlesNessuna valutazione finora

- CPR Crown Energy-July 7 2016 PDFDocumento42 pagineCPR Crown Energy-July 7 2016 PDFSky walkingNessuna valutazione finora

- Lbo Model Short FormDocumento4 pagineLbo Model Short FormAkash PrasadNessuna valutazione finora

- Oil and Gas Midstream Week 11-1 21.06.2022Documento18 pagineOil and Gas Midstream Week 11-1 21.06.2022MOHAMMAD ADAM ZAKARIANessuna valutazione finora

- Global - LNG - New - Pricing - Ahead - Ernst & YoungDocumento20 pagineGlobal - LNG - New - Pricing - Ahead - Ernst & YoungUJJWALNessuna valutazione finora

- FSMed ProjectManagementPlan (ComplexProject) 101Documento19 pagineFSMed ProjectManagementPlan (ComplexProject) 101AttaShah100% (1)

- GICS MapbookDocumento52 pagineGICS MapbookVivek AryaNessuna valutazione finora

- Analysis Report For Petroleum IndustryDocumento41 pagineAnalysis Report For Petroleum IndustryMohsin AliNessuna valutazione finora

- Proposed Acquisition of MerlonDocumento8 pagineProposed Acquisition of MerlonboringestNessuna valutazione finora

- M&As (Class4)Documento51 pagineM&As (Class4)Salman SalluNessuna valutazione finora

- Guidelines For CybersecurityDocumento6 pagineGuidelines For CybersecurityMaria Giselle AgustinNessuna valutazione finora

- Oil and Gas Valuation ConsiderationDocumento34 pagineOil and Gas Valuation ConsiderationBagus Deddy AndriNessuna valutazione finora

- Houtan Afkhami Jeremy Brown Patrick Bydume James WalshDocumento49 pagineHoutan Afkhami Jeremy Brown Patrick Bydume James WalshAdio FosterNessuna valutazione finora

- Mega-Field Developments Require Special Tatics, Risk Management PDFDocumento3 pagineMega-Field Developments Require Special Tatics, Risk Management PDFGILBERTO YOSHIDANessuna valutazione finora

- Oil&Gas Sector AnalysisDocumento7 pagineOil&Gas Sector AnalysisAMEY PATALENessuna valutazione finora

- Board of DirectorsDocumento57 pagineBoard of DirectorsAbdul Basit KirmaniNessuna valutazione finora

- Guggenheim LLC v. Birnbaum: Second Circuit Brief of Appellant-Defendant David Birnbaum - Filed Jun 18 2012Documento29 pagineGuggenheim LLC v. Birnbaum: Second Circuit Brief of Appellant-Defendant David Birnbaum - Filed Jun 18 2012Ron ColemanNessuna valutazione finora

- Bakrie Sumatra Plantation: Perplexing End To A Confusing YearDocumento5 pagineBakrie Sumatra Plantation: Perplexing End To A Confusing YearerlanggaherpNessuna valutazione finora

- TWNK Hostess CAGNY 2017Documento43 pagineTWNK Hostess CAGNY 2017Ala BasterNessuna valutazione finora

- Fcffsimpleginzu 2014Documento54 pagineFcffsimpleginzu 2014Pro Resources100% (1)

- Company Analysis and ValuationDocumento13 pagineCompany Analysis and ValuationAsif Abdullah KhanNessuna valutazione finora

- The IB Business of EquitiesDocumento79 pagineThe IB Business of EquitiesNgọc Phan Thị BíchNessuna valutazione finora

- Petrobras PresentationDocumento23 paginePetrobras PresentationwegrNessuna valutazione finora

- Sampath l2 WPDocumento16 pagineSampath l2 WPShiva RamaNessuna valutazione finora

- Entrepreneurship Challenges & Way ForwardDocumento17 pagineEntrepreneurship Challenges & Way ForwardDr Pranjal Kumar PhukanNessuna valutazione finora

- Quotation of Nile MiningDocumento7 pagineQuotation of Nile MiningOscarNessuna valutazione finora

- MOB Unit 2 Past PapersDocumento17 pagineMOB Unit 2 Past Paperspearlbarr91% (44)

- Simple Revocable Transfer On Death (Tod) DeedDocumento4 pagineSimple Revocable Transfer On Death (Tod) DeedJohn LessardNessuna valutazione finora

- Oracle Cloud Fusion Tax 12092016 V1.0Documento44 pagineOracle Cloud Fusion Tax 12092016 V1.0prasadv19806273100% (1)

- GANN SQ 9Documento38 pagineGANN SQ 9Pragnesh Shah100% (2)

- Seen Presents - Alcohol Trends ReportDocumento25 pagineSeen Presents - Alcohol Trends ReportAnonymous rjJZ8sSijNessuna valutazione finora

- K2.Inc Is Now BruvitiDocumento2 pagineK2.Inc Is Now BruvitiPR.comNessuna valutazione finora

- Hiller's Layoff NoticesDocumento6 pagineHiller's Layoff NoticesClickon DetroitNessuna valutazione finora

- Kotak Mahindra Life Insurance Company LTD Lta Claim FormDocumento2 pagineKotak Mahindra Life Insurance Company LTD Lta Claim FormCricket KheloNessuna valutazione finora

- Ques 1Documento2 pagineQues 1Renuka SharmaNessuna valutazione finora

- Marketing Project On Dabur HajmolaDocumento35 pagineMarketing Project On Dabur HajmolaAnuranjanSinha0% (1)

- Order Management: Microsoft Great Plains Solomon IV 5.0Documento506 pagineOrder Management: Microsoft Great Plains Solomon IV 5.0vanloi88Nessuna valutazione finora

- Market Beats PPT 18.11.11Documento49 pagineMarket Beats PPT 18.11.11Sheetal ShelkeNessuna valutazione finora

- Cambridge O Level: ACCOUNTING 7707/22Documento20 pagineCambridge O Level: ACCOUNTING 7707/22shujaitbukhariNessuna valutazione finora

- Supply and Demand Power Gap - Case Study of GujaratDocumento55 pagineSupply and Demand Power Gap - Case Study of GujaratSparshy SaxenaNessuna valutazione finora

- FRM Part 1 Study Plan May 2017Documento3 pagineFRM Part 1 Study Plan May 2017msreya100% (1)

- Terms and Conditions: Pre-Employment RequirementsDocumento5 pagineTerms and Conditions: Pre-Employment RequirementsKarl D AntonioNessuna valutazione finora

- KasusDocumento4 pagineKasusTry DharsanaNessuna valutazione finora

- Case: Valdes vs. RTC, G.R. No. 122749. July 31, 1996facts:: Carino V. CarinoDocumento10 pagineCase: Valdes vs. RTC, G.R. No. 122749. July 31, 1996facts:: Carino V. CarinoArgel Joseph CosmeNessuna valutazione finora

- DaburDocumento6 pagineDabursneh pimpalkarNessuna valutazione finora

- Culture AuditDocumento12 pagineCulture AuditBharath MenonNessuna valutazione finora

- Jigless Welding Case StudyDocumento11 pagineJigless Welding Case StudyakshaytomarNessuna valutazione finora

- Audit and Assurance June 2011 Marks PlanDocumento15 pagineAudit and Assurance June 2011 Marks Planjakariauzzal100% (1)

- Customer Advisory - OnE THC Announcement With Effect From 1 April 2023Documento4 pagineCustomer Advisory - OnE THC Announcement With Effect From 1 April 2023K58 TRUONG THI LAN ANHNessuna valutazione finora

- Market Survey To Ascertain Mayur's Position Rajasthan Spinning and Weaving Mills Ltd. (Marketing)Documento87 pagineMarket Survey To Ascertain Mayur's Position Rajasthan Spinning and Weaving Mills Ltd. (Marketing)Mustafa S TajaniNessuna valutazione finora

- KRosner Gazprom and The Russian State 2006Documento75 pagineKRosner Gazprom and The Russian State 2006Voicu TudorNessuna valutazione finora

- Pa em TendenciaDocumento21 paginePa em Tendenciasander10100% (1)

- Relevant Cost NotesDocumento69 pagineRelevant Cost NotesXena NatividadNessuna valutazione finora