Potrebbero piacerti anche

- Summary Notes IPCC Auditing 2Documento11 pagineSummary Notes IPCC Auditing 2Nishant Singh78% (9)

- PPTDocumento5 paginePPTStarNessuna valutazione finora

- Types of AuditDocumento58 pagineTypes of Auditvinay sainiNessuna valutazione finora

- Alan Fernandes (AUDIT EVIDENCE TO AUDIT REPORTING)Documento28 pagineAlan Fernandes (AUDIT EVIDENCE TO AUDIT REPORTING)Alan FernandesNessuna valutazione finora

- M2-Acceptance and Risk AssessmentDocumento10 pagineM2-Acceptance and Risk AssessmentSanjay PradhanNessuna valutazione finora

- Acca - F 8 - L2Documento14 pagineAcca - F 8 - L2shazyasgharNessuna valutazione finora

- Audit NotesDocumento67 pagineAudit NotesGaganBabel100% (1)

- Auditing Question Bank - StudentsDocumento25 pagineAuditing Question Bank - StudentsAashna JainNessuna valutazione finora

- Module 1 BASIC CONCEPTS OF FINANCIAL STATEMENT AUDIT PDFDocumento8 pagineModule 1 BASIC CONCEPTS OF FINANCIAL STATEMENT AUDIT PDFNiño Mendoza Mabato100% (1)

- Ch1 AuditObjectivesDocumento7 pagineCh1 AuditObjectivesHarris LuiNessuna valutazione finora

- Audit 1Documento25 pagineAudit 1Mohammad Saadman100% (1)

- CA Inter Audit Question BankDocumento315 pagineCA Inter Audit Question BankKhushi SoniNessuna valutazione finora

- Introduction To Financial Statement AuditDocumento28 pagineIntroduction To Financial Statement AuditJnn CycNessuna valutazione finora

- Concepts and Need for AssuranceDocumento14 pagineConcepts and Need for Assurancetusher pepolNessuna valutazione finora

- Standards On AuditingDocumento59 pagineStandards On AuditingCa Siddhi GuptaNessuna valutazione finora

- Unit A: Overview of Audit ProcessDocumento18 pagineUnit A: Overview of Audit Processchloebaby19Nessuna valutazione finora

- POA 1 (Prepared)Documento22 paginePOA 1 (Prepared)Mohit ShahNessuna valutazione finora

- Aud Theo - 3Documento5 pagineAud Theo - 3Cyra EllaineNessuna valutazione finora

- F8 Auditing & AssuranceDocumento291 pagineF8 Auditing & AssuranceSharon Sara SunilNessuna valutazione finora

- AT-03 (Introduction To Auditing)Documento4 pagineAT-03 (Introduction To Auditing)Soremn PotatoheadNessuna valutazione finora

- Chapter-6: in An Effective Manner. Planning Consists of A Number of Elements. However, They Could Be Summarized AsDocumento10 pagineChapter-6: in An Effective Manner. Planning Consists of A Number of Elements. However, They Could Be Summarized AsNasir RifatNessuna valutazione finora

- Audit Notes - CompressedDocumento214 pagineAudit Notes - CompressedAlexis ParrisNessuna valutazione finora

- Acca F8 LecturesDocumento143 pagineAcca F8 LecturesANASNessuna valutazione finora

- Stages of An AuditDocumento4 pagineStages of An AuditDerrick KimaniNessuna valutazione finora

- Audit & Assurance Individual Assignment: A Report by by Mr. G.L.S Anuradha Sab/Bsc/2020A/We-044Documento9 pagineAudit & Assurance Individual Assignment: A Report by by Mr. G.L.S Anuradha Sab/Bsc/2020A/We-044Shehan AnuradaNessuna valutazione finora

- Unit - 3: 1.preparation Before The Commencement of AuditDocumento12 pagineUnit - 3: 1.preparation Before The Commencement of AuditNaga Raju DudalaNessuna valutazione finora

- Auditors' Reports ChapterDocumento11 pagineAuditors' Reports Chapterdejen mengstieNessuna valutazione finora

- Philippine Accountancy Act and Auditing StandardsDocumento35 paginePhilippine Accountancy Act and Auditing StandardsKezNessuna valutazione finora

- Chapter 2 Basic Concepts in Auditing PM PDFDocumento25 pagineChapter 2 Basic Concepts in Auditing PM PDFViene CanlasNessuna valutazione finora

- Reading Notes and MC answersDocumento7 pagineReading Notes and MC answersDe Nev OelNessuna valutazione finora

- Acca F8 Lectures PDFDocumento143 pagineAcca F8 Lectures PDFBin SaadunNessuna valutazione finora

- Basic Concepts in AuditingDocumento29 pagineBasic Concepts in Auditinganon_672065362100% (1)

- Assignment - 1 - AuditDocumento9 pagineAssignment - 1 - AuditMuskan singh RajputNessuna valutazione finora

- AuditingDocumento47 pagineAuditingImran Alam ChowdhuryNessuna valutazione finora

- Standards On AuditingDocumento37 pagineStandards On AuditingAryan ShaikhNessuna valutazione finora

- Lecture One - Assurance & Auditing - An Overview and Structure of The ProfessionDocumento20 pagineLecture One - Assurance & Auditing - An Overview and Structure of The ProfessionPranto KarmokarNessuna valutazione finora

- Auditing Quiz + NotesDocumento16 pagineAuditing Quiz + NoteswamahibawiNessuna valutazione finora

- 07 FS Audit Process - Audit PlanningDocumento6 pagine07 FS Audit Process - Audit Planningrandomlungs121223Nessuna valutazione finora

- Planning and Conducting AuditaDocumento12 paginePlanning and Conducting AuditaJc QuismundoNessuna valutazione finora

- Chapter - 1 (Short Notes)Documento7 pagineChapter - 1 (Short Notes)Aakansha SinghNessuna valutazione finora

- Auditing Assurance Test 1 CH 1 Unscheduled Solution 1670225228Documento8 pagineAuditing Assurance Test 1 CH 1 Unscheduled Solution 1670225228Vinayak PoddarNessuna valutazione finora

- 1498721945audit JoinerDocumento70 pagine1498721945audit JoinerRockNessuna valutazione finora

- The Overview of AuditingDocumento4 pagineThe Overview of AuditingJelyn RuazolNessuna valutazione finora

- Auditing Techniques and Audit ProgramDocumento20 pagineAuditing Techniques and Audit Programgemixon120Nessuna valutazione finora

- Internal Audit, Management and Operational Audit GuideDocumento14 pagineInternal Audit, Management and Operational Audit GuideNeetu gargNessuna valutazione finora

- Preengagement and PlanningDocumento4 paginePreengagement and PlanningAllyssa MababangloobNessuna valutazione finora

- (Midterm) Aap - Module 4 Psa-200 - 210 - 240Documento7 pagine(Midterm) Aap - Module 4 Psa-200 - 210 - 24025 CUNTAPAY, FRENCHIE VENICE B.Nessuna valutazione finora

- IAR Auditing ConclusionDocumento23 pagineIAR Auditing Conclusionmarlout.sarita100% (1)

- Audit Icai FullDocumento720 pagineAudit Icai Fullnsaiakshaya16Nessuna valutazione finora

- Nature, Objective and Scope of Audit: Learning OutcomesDocumento46 pagineNature, Objective and Scope of Audit: Learning OutcomesAniketNessuna valutazione finora

- 02 Introduction To AuditingDocumento3 pagine02 Introduction To Auditingrandomlungs121223Nessuna valutazione finora

- Audit Planning Analytical Procedures GuideDocumento9 pagineAudit Planning Analytical Procedures GuideDahlia BloomsNessuna valutazione finora

- BA4 - CONTROLS - LMS - BOOK - 03 External Audit - Part 01Documento11 pagineBA4 - CONTROLS - LMS - BOOK - 03 External Audit - Part 01Sanjeev JayaratnaNessuna valutazione finora

- Steps in Audit Engagement CDocumento5 pagineSteps in Audit Engagement CReland CastroNessuna valutazione finora

- Chapter 3 General Types of Audit - PPT 123915218Documento32 pagineChapter 3 General Types of Audit - PPT 123915218Clar Aaron Bautista100% (2)

- HO2-A - Risk-Based Audit of Financial Statements Part 1 (Overview) - RevisedDocumento8 pagineHO2-A - Risk-Based Audit of Financial Statements Part 1 (Overview) - RevisedJaynalyn MonasterialNessuna valutazione finora

- Audit Planning & Documentation - Taxguru - inDocumento8 pagineAudit Planning & Documentation - Taxguru - inNino NakanoNessuna valutazione finora

- Midterms Quiz 1 GdocsDocumento41 pagineMidterms Quiz 1 GdocsIris FenelleNessuna valutazione finora

- Audit Risk Alert: General Accounting and Auditing Developments 2018/19Da EverandAudit Risk Alert: General Accounting and Auditing Developments 2018/19Nessuna valutazione finora

- Audit Risk Alert: Employee Benefit Plans Industry Developments, 2018Da EverandAudit Risk Alert: Employee Benefit Plans Industry Developments, 2018Nessuna valutazione finora

- Audit Standards ChalisaDocumento19 pagineAudit Standards ChalisaSri PavanNessuna valutazione finora

- INTOSAI Principles for External Audit of International InstitutionsDocumento18 pagineINTOSAI Principles for External Audit of International InstitutionsMuhammed Haj HasnNessuna valutazione finora

- Applied Auditing Module 2Documento6 pagineApplied Auditing Module 2Sherri BonquinNessuna valutazione finora

- 3audit ReportsDocumento67 pagine3audit ReportsmuinbossNessuna valutazione finora

- Ireneo Answer Key 2017Documento29 pagineIreneo Answer Key 2017Elisabeth HenangerNessuna valutazione finora

- Convergence of Public Sector Audit StandardsDocumento36 pagineConvergence of Public Sector Audit StandardsInternational Consortium on Governmental Financial ManagementNessuna valutazione finora

- TralseDocumento15 pagineTralseGLORY MALIGANGNessuna valutazione finora

- Timeline IIADocumento1 paginaTimeline IIAMiljane PerdizoNessuna valutazione finora

- Quiz 2 Audtheo PDFDocumento4 pagineQuiz 2 Audtheo PDFCharlen Relos GermanNessuna valutazione finora

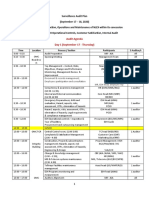

- Surveillance Audit PlanDocumento3 pagineSurveillance Audit PlanJessa VillanuevaNessuna valutazione finora

- Test Bank With Answers of Accounting Information System by Turner Chapter 07Documento28 pagineTest Bank With Answers of Accounting Information System by Turner Chapter 07Ebook free100% (3)

- Audit Reports: ©2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley 3 - 1Documento45 pagineAudit Reports: ©2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley 3 - 1Setia NurulNessuna valutazione finora

- Chapter 10 Completing The AuditDocumento8 pagineChapter 10 Completing The AuditKayla Sophia PatioNessuna valutazione finora

- Test Bank For Auditing A Risk Based Approach To Conducting A Quality Audit 9th Edition by Johnstone PDFDocumento15 pagineTest Bank For Auditing A Risk Based Approach To Conducting A Quality Audit 9th Edition by Johnstone PDFa878091955Nessuna valutazione finora

- Aud Theory Comprehensive Self Review Quizzer MC PDFDocumento20 pagineAud Theory Comprehensive Self Review Quizzer MC PDFZi VillarNessuna valutazione finora

- Practice QUIZ - SEC and PCAOBDocumento4 paginePractice QUIZ - SEC and PCAOBAaditya ManojNessuna valutazione finora

- PC 22 - Practice Set 1Documento14 paginePC 22 - Practice Set 1Shadab RashidNessuna valutazione finora

- Test Bank Auditing Theory Proprofs - Quiz PDFDocumento2 pagineTest Bank Auditing Theory Proprofs - Quiz PDFEmellaine Arazo de GuzmanNessuna valutazione finora

- Analisis Perkembangan Return On Assets (Roa) Dan KeuanganDocumento12 pagineAnalisis Perkembangan Return On Assets (Roa) Dan KeuanganMuhammad DylanNessuna valutazione finora

- Audit and Auditor in EthiopiaHistorical DevelopmeDocumento1 paginaAudit and Auditor in EthiopiaHistorical DevelopmeHabtamu Fiyssa100% (1)

- GTAG3 Audit KontinyuDocumento37 pagineGTAG3 Audit KontinyujonisupriadiNessuna valutazione finora

- Data San Jawaban-Soal-Chapter-15-SebagianDocumento10 pagineData San Jawaban-Soal-Chapter-15-Sebagiansan_tbaiplgNessuna valutazione finora

- TTTDocumento6 pagineTTTAngelika BalmeoNessuna valutazione finora

- ICEPhilwaniAUD679 Lesson Plan (Okt 2020)Documento5 pagineICEPhilwaniAUD679 Lesson Plan (Okt 2020)Nur Dina AbsbNessuna valutazione finora

- 9 CTA JusticesDocumento9 pagine9 CTA JusticesJomar TenezaNessuna valutazione finora

- Sim # Topics Research?Documento2 pagineSim # Topics Research?Arnel RemorinNessuna valutazione finora

- Audit CommitteeDocumento4 pagineAudit CommitteeAnkit SharmaNessuna valutazione finora

- 17 Modification To The Auditor's ReportDocumento5 pagine17 Modification To The Auditor's Reportrandomlungs121223Nessuna valutazione finora

- Chapter 13 - QuestionsDocumento10 pagineChapter 13 - QuestionsMinh AnhNessuna valutazione finora

- Independent Auditors ReportDocumento2 pagineIndependent Auditors ReportKaren May LusungNessuna valutazione finora