Potrebbero piacerti anche

- Sfo ShippersDocumento2 pagineSfo ShippersNishant ChandraNessuna valutazione finora

- Free Cash Flow: Seeing Through the Accounting Fog Machine to Find Great StocksDa EverandFree Cash Flow: Seeing Through the Accounting Fog Machine to Find Great StocksValutazione: 4 su 5 stelle4/5 (1)

- Chapter 3 Presentation of Financial StatementsDocumento24 pagineChapter 3 Presentation of Financial StatementsLEE WEI LONGNessuna valutazione finora

- Putting English Unit14Documento13 paginePutting English Unit14Dung LeNessuna valutazione finora

- FARAP-4516Documento10 pagineFARAP-4516Accounting StuffNessuna valutazione finora

- Accounting For Retained EarningsDocumento11 pagineAccounting For Retained EarningsSarah Johnson100% (1)

- Rufino Tan Vs Ramon Del RosarioDocumento1 paginaRufino Tan Vs Ramon Del RosarioJocelyn MagbanuaNessuna valutazione finora

- Best Practices in Hotel Financial ManagementDocumento3 pagineBest Practices in Hotel Financial ManagementDhruv BansalNessuna valutazione finora

- Logistics AccountingDocumento131 pagineLogistics AccountingCA Rekha Ashok PillaiNessuna valutazione finora

- Creative Cash Flow Reporting: Uncovering Sustainable Financial PerformanceDa EverandCreative Cash Flow Reporting: Uncovering Sustainable Financial PerformanceValutazione: 3.5 su 5 stelle3.5/5 (5)

- COA Circular 94-013 Dated Dec. 13, 1994Documento5 pagineCOA Circular 94-013 Dated Dec. 13, 1994Rej FranciscoNessuna valutazione finora

- Annex 101 - BB Nolco TaxDocumento3 pagineAnnex 101 - BB Nolco TaxJei Essa AlmiasNessuna valutazione finora

- Summary of Richard A. Lambert's Financial Literacy for ManagersDa EverandSummary of Richard A. Lambert's Financial Literacy for ManagersNessuna valutazione finora

- Air India - Balance Score CardDocumento6 pagineAir India - Balance Score Cardramyavenugopal100% (1)

- Spisak Parfema NEWDocumento1 paginaSpisak Parfema NEWDouglas CoxNessuna valutazione finora

- Salient Features of GNDocumento10 pagineSalient Features of GNChethan VenkateshNessuna valutazione finora

- Revised Schedule VIDocumento23 pagineRevised Schedule VIJitendra GahanduleNessuna valutazione finora

- Chap 004Documento39 pagineChap 004trinhbangNessuna valutazione finora

- Statements of Accounting Standards (AS 10) : Accounting For Fixed AssetsDocumento6 pagineStatements of Accounting Standards (AS 10) : Accounting For Fixed AssetsSantoshca1984Nessuna valutazione finora

- Chapter 9 Financial Instruments: Learning ObjectivesDocumento41 pagineChapter 9 Financial Instruments: Learning Objectivessamuel_dwumfourNessuna valutazione finora

- Cash Flow ReportingDocumento8 pagineCash Flow ReportingTosin YusufNessuna valutazione finora

- Chapter 19 Consolidated Statement of Financial Position With Consolidated AdjustmentsDocumento17 pagineChapter 19 Consolidated Statement of Financial Position With Consolidated Adjustmentssamuel_dwumfourNessuna valutazione finora

- The Effects of Changes in Foreign Exchange Rates: Indian Accounting Standard (Ind AS) 21Documento27 pagineThe Effects of Changes in Foreign Exchange Rates: Indian Accounting Standard (Ind AS) 21pg0utamNessuna valutazione finora

- Earnings Per Share: Accounting Standard (AS) 20Documento27 pagineEarnings Per Share: Accounting Standard (AS) 20Akshay JainNessuna valutazione finora

- International Financial Reporting StandardsDocumento20 pagineInternational Financial Reporting StandardsAK FleurNessuna valutazione finora

- Chapter 4Documento35 pagineChapter 4Anonymous 7CxwuBUJz3Nessuna valutazione finora

- Chap 007Documento39 pagineChap 007trinhbang100% (1)

- Guidance Manual FinalDocumento27 pagineGuidance Manual FinalrosdobNessuna valutazione finora

- CPAR Financial StatementsDocumento5 pagineCPAR Financial StatementsAnjo EllisNessuna valutazione finora

- Ch13 RevAnsDocumento16 pagineCh13 RevAnssamuel_dwumfourNessuna valutazione finora

- Kunci Jawaban Analisis Laporan Keuangan Bab 7Documento50 pagineKunci Jawaban Analisis Laporan Keuangan Bab 7dwi milyantiNessuna valutazione finora

- Chap 005Documento30 pagineChap 005trinhbang100% (1)

- Management Representation Letter: If Required Add "On Behalf of The Board of Directors (Or Similar Body) ."Documento1 paginaManagement Representation Letter: If Required Add "On Behalf of The Board of Directors (Or Similar Body) ."LaraNessuna valutazione finora

- Financial Statements and Financial AnalysisDocumento23 pagineFinancial Statements and Financial AnalysisShadab AshfaqNessuna valutazione finora

- Chap001 Test BankDocumento107 pagineChap001 Test BankJames Stallins Jr.Nessuna valutazione finora

- 2.3.1 Financial Statement PresentationDocumento10 pagine2.3.1 Financial Statement PresentationRichard Jr RjNessuna valutazione finora

- Porter SM Ch. 06 - 2ppDocumento17 paginePorter SM Ch. 06 - 2ppmfawzi010Nessuna valutazione finora

- Chapter 08Documento18 pagineChapter 08Tam NguyenNessuna valutazione finora

- Introduction To Balance Sheet: Assets Liabilities Owner's (Stockholders') EquityDocumento7 pagineIntroduction To Balance Sheet: Assets Liabilities Owner's (Stockholders') EquityChanti KumarNessuna valutazione finora

- Chapter 10-Statement of Cash Flows: Multiple ChoiceDocumento26 pagineChapter 10-Statement of Cash Flows: Multiple ChoiceAsma JamshaidNessuna valutazione finora

- Title Ii Tax On Income: Chapter I - Definitions SEC. 22. Definitions - When Used in This TitleDocumento3 pagineTitle Ii Tax On Income: Chapter I - Definitions SEC. 22. Definitions - When Used in This TitleEdward Kenneth KungNessuna valutazione finora

- Audit Programe For Statutory AuditDocumento20 pagineAudit Programe For Statutory AuditTekumani Naveen KumarNessuna valutazione finora

- FMM Acct For Business Ch1Documento99 pagineFMM Acct For Business Ch1Rubi JangraNessuna valutazione finora

- Chapter 12 Structuring The Deal Tax and AccountingDocumento10 pagineChapter 12 Structuring The Deal Tax and Accountingvineet_bmNessuna valutazione finora

- IFRS 5 Non-Current Assets Held For Sale and Discontinued Operations - UpdDocumento24 pagineIFRS 5 Non-Current Assets Held For Sale and Discontinued Operations - UpdnikkibausaNessuna valutazione finora

- Accounts - Module 6 Provisions of The Companies Act 1956Documento15 pagineAccounts - Module 6 Provisions of The Companies Act 19569986212378Nessuna valutazione finora

- IAS-Cash Flow StatementDocumento24 pagineIAS-Cash Flow Statementpks009Nessuna valutazione finora

- Distinguish Between Capital Expenditure and Revenue ExpenditureDocumento11 pagineDistinguish Between Capital Expenditure and Revenue ExpenditureGopika GopalakrishnanNessuna valutazione finora

- Leach TB Chap09 Ed3Documento8 pagineLeach TB Chap09 Ed3bia070386Nessuna valutazione finora

- Chapter 3 FARDocumento4 pagineChapter 3 FARZee DrakeNessuna valutazione finora

- Less: Agreed Value of Less: MV of Total Liab. XXX Merger: Amount Paid To EquityDocumento4 pagineLess: Agreed Value of Less: MV of Total Liab. XXX Merger: Amount Paid To Equityshanky631Nessuna valutazione finora

- Net Profit or Loss For The Period, Prior Period Items and Changes in Accounting PoliciesDocumento6 pagineNet Profit or Loss For The Period, Prior Period Items and Changes in Accounting Policiessanyu1208Nessuna valutazione finora

- Accounting Standard 16: Borrowing CostsDocumento33 pagineAccounting Standard 16: Borrowing CostsP VenkatesanNessuna valutazione finora

- IAS 39 Detailed SummaryDocumento18 pagineIAS 39 Detailed Summarywesternwound82Nessuna valutazione finora

- Corporate Law AssignmentDocumento9 pagineCorporate Law AssignmentKushagra KhannaNessuna valutazione finora

- Canadian Gaap - Ifrs Comparison Series: Issue 15: IAS 1 Presentation of Financial StatementsDocumento6 pagineCanadian Gaap - Ifrs Comparison Series: Issue 15: IAS 1 Presentation of Financial StatementsBooky7Nessuna valutazione finora

- Mock Cpa Board Exams Rfjpia R 12 W AnsDocumento17 pagineMock Cpa Board Exams Rfjpia R 12 W AnsRheneir MoraNessuna valutazione finora

- Accounting Standard (AS) 9 (Issued 1985) : Revenue RecognitionDocumento9 pagineAccounting Standard (AS) 9 (Issued 1985) : Revenue Recognitionsanyu1208Nessuna valutazione finora

- Corporate Law Assignment ONDocumento9 pagineCorporate Law Assignment ONnikunjbansal909Nessuna valutazione finora

- Inventory Accounting Entries:: SAP Account PostingDocumento11 pagineInventory Accounting Entries:: SAP Account Postingsomu_suresh5362Nessuna valutazione finora

- Form 3CD NewDocumento16 pagineForm 3CD NewRikta KariaNessuna valutazione finora

- Income Tax (File - 1)Documento5 pagineIncome Tax (File - 1)Nazim KhanNessuna valutazione finora

- Statement of Cash Flow: A Teaching NoteDocumento6 pagineStatement of Cash Flow: A Teaching NotesnowgirlshuweiNessuna valutazione finora

- Chapter 5 - The Income State and The Statement of Cash FlowDocumento101 pagineChapter 5 - The Income State and The Statement of Cash FlowJoey LessardNessuna valutazione finora

- Case Studies in Not-for-Profit Accounting and AuditingDa EverandCase Studies in Not-for-Profit Accounting and AuditingNessuna valutazione finora

- Form 990: Exploring the Form's Complex SchedulesDa EverandForm 990: Exploring the Form's Complex SchedulesNessuna valutazione finora

- Woolf Prompt WritingDocumento1 paginaWoolf Prompt Writingapi-2089824930% (1)

- Accounting For NotesDocumento3 pagineAccounting For NotesRaffay MaqboolNessuna valutazione finora

- Aarti Brochure 2009Documento4 pagineAarti Brochure 2009Sabari MarketingNessuna valutazione finora

- Bradford Snell The Street Car ConspiracyDocumento4 pagineBradford Snell The Street Car ConspiracyDaniel DavarNessuna valutazione finora

- CH 12 HWDocumento45 pagineCH 12 HWHannah Fuller100% (1)

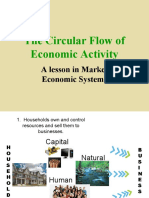

- Circular FlowDocumento21 pagineCircular FlowSheryl BorromeoNessuna valutazione finora

- Market Share AnalysisDocumento3 pagineMarket Share AnalysisLawal Musibaudeem ObafemiNessuna valutazione finora

- PricelistDocumento3 paginePricelist4 fruit companyNessuna valutazione finora

- MudraDocumento19 pagineMudraManoj MawaleNessuna valutazione finora

- Tourism PolicyDocumento6 pagineTourism Policylanoox0% (1)

- Chief Executive Officer CPG in West Palm Beach FL Resume James MercerDocumento2 pagineChief Executive Officer CPG in West Palm Beach FL Resume James MercerJames MercerNessuna valutazione finora

- International Marketing - ChinaDocumento10 pagineInternational Marketing - ChinaNaijalegendNessuna valutazione finora

- Donner Company 2Documento6 pagineDonner Company 2Nuno Saraiva0% (1)

- Masan Group CorporationDocumento31 pagineMasan Group Corporationhồ nam longNessuna valutazione finora

- SOLAS - Verified Gross Mass (VGM)Documento2 pagineSOLAS - Verified Gross Mass (VGM)Mary Joy Dela MasaNessuna valutazione finora

- Capital StructureDocumento44 pagineCapital Structure26155152Nessuna valutazione finora

- Closure in Valuation: Estimating Terminal Value: Problem 1Documento3 pagineClosure in Valuation: Estimating Terminal Value: Problem 1Silviu TrebuianNessuna valutazione finora

- Walt Disney Company PDFDocumento20 pagineWalt Disney Company PDFGabriella VenturinaNessuna valutazione finora

- RWJ 08Documento38 pagineRWJ 08Kunal PuriNessuna valutazione finora

- Indifference CurveDocumento16 pagineIndifference Curveএস. এম. তানজিলুল ইসলামNessuna valutazione finora

- Agriculture Subsidies and DevelopmentDocumento2 pagineAgriculture Subsidies and Developmentbluerockwalla100% (2)

- FM 8th Edition Chapter 12 - Risk and ReturnDocumento20 pagineFM 8th Edition Chapter 12 - Risk and ReturnKa Io ChaoNessuna valutazione finora

- StartUp India - Case AnalysisDocumento3 pagineStartUp India - Case AnalysisIrshad AzeezNessuna valutazione finora