Potrebbero piacerti anche

- Retail Market Year End Snapshot 2013 PDFDocumento7 pagineRetail Market Year End Snapshot 2013 PDFAuthor LesNessuna valutazione finora

- Belgrade Retail Market Report Q2 2013Documento3 pagineBelgrade Retail Market Report Q2 2013Author LesNessuna valutazione finora

- PKS EnglishDocumento2 paginePKS EnglishAuthor LesNessuna valutazione finora

- Retail Market Overview 1H 2012Documento2 pagineRetail Market Overview 1H 2012Author LesNessuna valutazione finora

- Belgrade Retail Market Report Q1 2013Documento3 pagineBelgrade Retail Market Report Q1 2013Author LesNessuna valutazione finora

- Bosnia Real EstateDocumento64 pagineBosnia Real EstateAuthor LesNessuna valutazione finora

- Anti Bribery Policy enDocumento7 pagineAnti Bribery Policy enAuthor LesNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (120)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Manta Aji Coroko Sungsang ASLIDocumento1 paginaManta Aji Coroko Sungsang ASLIFarhan HumamNessuna valutazione finora

- Small Scale Industries in IndiaDocumento18 pagineSmall Scale Industries in IndiaTEJA SINGHNessuna valutazione finora

- Collection of Direct Taxes - OLTASDocumento36 pagineCollection of Direct Taxes - OLTASnalluriimpNessuna valutazione finora

- Notice 11120 02 Apr 2024Documento669 pagineNotice 11120 02 Apr 2024bhattacharya.devangana2Nessuna valutazione finora

- Game Theory (2) - Mechanism Design With TransfersDocumento60 pagineGame Theory (2) - Mechanism Design With Transfersjm15yNessuna valutazione finora

- Indias Top 50 Best ItDocumento14 pagineIndias Top 50 Best ItAnonymous Nl41INVNessuna valutazione finora

- 6 Zimbabwean DollarDocumento32 pagine6 Zimbabwean DollarArjun Nayak100% (1)

- Exam 20210209Documento2 pagineExam 20210209Luca CastellaniNessuna valutazione finora

- Business Economics - Neil Harris - Summary Chapter 3Documento2 pagineBusiness Economics - Neil Harris - Summary Chapter 3Nabila HuwaidaNessuna valutazione finora

- Soft Offer Canned Food-June10Documento3 pagineSoft Offer Canned Food-June10davidarcosfuentesNessuna valutazione finora

- Strategic Planning ModuleDocumento78 pagineStrategic Planning ModuleQueenElaineTulbeNessuna valutazione finora

- Li & Fung LimitedDocumento2 pagineLi & Fung Limitedeguno12Nessuna valutazione finora

- Report of The Third South Asian People's SummitDocumento220 pagineReport of The Third South Asian People's SummitMustafa Nazir Ahmad100% (1)

- Baggage Provisions 7242128393292Documento2 pagineBaggage Provisions 7242128393292alexpepe1234345Nessuna valutazione finora

- Proposal Project AyamDocumento14 pagineProposal Project AyamIrvan PamungkasNessuna valutazione finora

- Yong Le: Beijing Huaxia Yongleadhesive Tape Co., LTDDocumento9 pagineYong Le: Beijing Huaxia Yongleadhesive Tape Co., LTDColors Little ParkNessuna valutazione finora

- Company Profile - Herman Zemel enDocumento17 pagineCompany Profile - Herman Zemel enAlhussein Banuson100% (1)

- Unit 7: Account Current: Learning OutcomesDocumento14 pagineUnit 7: Account Current: Learning OutcomesamirNessuna valutazione finora

- Banglore BPODocumento2 pagineBanglore BPOwaris bhatNessuna valutazione finora

- Porter 5 Force FinalDocumento35 paginePorter 5 Force FinalAbinash BiswalNessuna valutazione finora

- Wells Fargo Everyday CheckingDocumento6 pagineWells Fargo Everyday CheckingDavid Dali Rojas Huamanchau100% (1)

- Indian Economic Development: DAV Fertilizer Public School, BabralaDocumento96 pagineIndian Economic Development: DAV Fertilizer Public School, Babralakavin sNessuna valutazione finora

- PHM PCH EnglishDocumento9 paginePHM PCH Englishlalit823187Nessuna valutazione finora

- The Manufacturing Sector in Malaysia PDFDocumento17 pagineThe Manufacturing Sector in Malaysia PDFNazirah Abdul RohmanNessuna valutazione finora

- Rent ReceiptDocumento1 paginaRent ReceiptHarish LakhaniNessuna valutazione finora

- Lesson 23 Illustrating Simple and Compound InterestDocumento12 pagineLesson 23 Illustrating Simple and Compound InterestANGELIE FERNANDEZNessuna valutazione finora

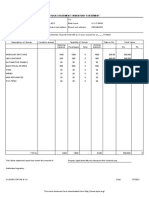

- Stock Statement Format For Bank LoanDocumento1 paginaStock Statement Format For Bank Loanpsycho Neha40% (5)

- AMT4SAP - Junio26 - Red - v3 PDFDocumento30 pagineAMT4SAP - Junio26 - Red - v3 PDFCarlos Eugenio Lovera VelasquezNessuna valutazione finora

- Origin and Theoretical Basis of The New Public Management (NPM)Documento35 pagineOrigin and Theoretical Basis of The New Public Management (NPM)Jessie Radaza TutorNessuna valutazione finora

- BA316 International Business Trade Module 2Documento19 pagineBA316 International Business Trade Module 2Pamela Rose CasenioNessuna valutazione finora