Potrebbero piacerti anche

- Summary of Stefan Loesch's A Guide to Financial Regulation for Fintech EntrepreneursDa EverandSummary of Stefan Loesch's A Guide to Financial Regulation for Fintech EntrepreneursNessuna valutazione finora

- Week 12 Reading 03 Insights33 PDFDocumento43 pagineWeek 12 Reading 03 Insights33 PDFAsri SiraitNessuna valutazione finora

- Behind the Swap: The Broken Infrastructure of Risk Management and a Framework for a Better ApproachDa EverandBehind the Swap: The Broken Infrastructure of Risk Management and a Framework for a Better ApproachNessuna valutazione finora

- Former Lecturer, Institute of Financial Services Zug (IFZ)Documento12 pagineFormer Lecturer, Institute of Financial Services Zug (IFZ)Willi BrammertzNessuna valutazione finora

- A Critical Discussion On How Democratisation of Finance Has Transformed Consumers Into Financial CitizensDocumento14 pagineA Critical Discussion On How Democratisation of Finance Has Transformed Consumers Into Financial CitizensEdem EdysonNessuna valutazione finora

- Payments 101Documento37 paginePayments 101David Leeman100% (1)

- Whole Loan Book Entry White Paper: A Blueprint For The Future, 1993 Whitepaper - Phyllis K SlesingerDocumento3 pagineWhole Loan Book Entry White Paper: A Blueprint For The Future, 1993 Whitepaper - Phyllis K SlesingerTim BryantNessuna valutazione finora

- Some Legal Implications of The Use of Computers in The Banking BusinessDocumento8 pagineSome Legal Implications of The Use of Computers in The Banking BusinessJignesh GhaskataNessuna valutazione finora

- Research Paper On Electronic Fund TransferDocumento4 pagineResearch Paper On Electronic Fund Transferwzsatbcnd100% (1)

- Roger W Ferguson, JR: The Evolving Financial and Payment SystemDocumento4 pagineRoger W Ferguson, JR: The Evolving Financial and Payment SystemFlaviub23Nessuna valutazione finora

- MR Latter Looks at The Implications of E-Commerce For The Banking and Monetary System in Hong KongDocumento4 pagineMR Latter Looks at The Implications of E-Commerce For The Banking and Monetary System in Hong KongFlaviub23Nessuna valutazione finora

- Examining The Extensive Regulation of Financial TechnologiesDocumento39 pagineExamining The Extensive Regulation of Financial TechnologiesCrowdfundInsiderNessuna valutazione finora

- Virgo ProposalDocumento8 pagineVirgo ProposalWalterNessuna valutazione finora

- What If We Treated Regulators Like ClientsDocumento3 pagineWhat If We Treated Regulators Like ClientsDeloitte AnalyticsNessuna valutazione finora

- Mr. Patrikis Discusses The Monetary Policy and Regulatory Implications of Banking On The Internet Address by The Vice-President of The Federal Reserve Bank of NewDocumento9 pagineMr. Patrikis Discusses The Monetary Policy and Regulatory Implications of Banking On The Internet Address by The Vice-President of The Federal Reserve Bank of NewFlaviub23Nessuna valutazione finora

- New Regulatory Approach To Ecuador's Electronic Money From A Comparative International ScopeDocumento23 pagineNew Regulatory Approach To Ecuador's Electronic Money From A Comparative International ScopeHasfi YakobNessuna valutazione finora

- Reasons For Selecting The ProjectDocumento19 pagineReasons For Selecting The ProjectvivekksethNessuna valutazione finora

- DAO Legal Framework Jennings Kerr10.19.21 FinalDocumento30 pagineDAO Legal Framework Jennings Kerr10.19.21 FinalLastminute LaiNessuna valutazione finora

- The Challenges of E-BankingDocumento4 pagineThe Challenges of E-Bankingxuanb2009025Nessuna valutazione finora

- MR Mboweni Discusses E-Money and Its Impact On The Central Bank's OperationsDocumento5 pagineMR Mboweni Discusses E-Money and Its Impact On The Central Bank's OperationsFlaviub23Nessuna valutazione finora

- Why (And How) Should Lenders Start Building An Online Loan PortfolioDocumento3 pagineWhy (And How) Should Lenders Start Building An Online Loan PortfolioDivjyot88Nessuna valutazione finora

- Banking Through Networks of Retail AgentsDocumento24 pagineBanking Through Networks of Retail AgentsGautam IvaturyNessuna valutazione finora

- The Project: Financial Planning and Wealth Management Mid TermDocumento6 pagineThe Project: Financial Planning and Wealth Management Mid TermGagan KarwarNessuna valutazione finora

- First 3 PointersDocumento13 pagineFirst 3 PointersParav BansalNessuna valutazione finora

- Fintech Laws and Regulations 2021 - USADocumento28 pagineFintech Laws and Regulations 2021 - USAmiguelNessuna valutazione finora

- The Secrets of Offshore Banking - Part OneDocumento5 pagineThe Secrets of Offshore Banking - Part OneOffshore Company FormationNessuna valutazione finora

- SSRN Id4380768Documento17 pagineSSRN Id4380768SashaFierce Los A&ANessuna valutazione finora

- US GTM LentraDocumento6 pagineUS GTM LentraNabeel MohammadNessuna valutazione finora

- Loan Provision ServicesDocumento3 pagineLoan Provision ServicesAnonymous HSmVkCD4Nessuna valutazione finora

- Roger W Ferguson JR: Electronic Commerce, Banking and PaymentsDocumento5 pagineRoger W Ferguson JR: Electronic Commerce, Banking and PaymentsFlaviub23Nessuna valutazione finora

- Retail Payments: Overview, Empirical Results, and Unanswered QuestionsDocumento20 pagineRetail Payments: Overview, Empirical Results, and Unanswered QuestionsLuisMendiolaNessuna valutazione finora

- Fintechs, Techfins, and Associated Opportunities and ChallengesDocumento6 pagineFintechs, Techfins, and Associated Opportunities and ChallengesGodfrey MakurumureNessuna valutazione finora

- A Note On Cyber Crime and Economic Offence in Online BankingDocumento14 pagineA Note On Cyber Crime and Economic Offence in Online BankingBasu DuttaNessuna valutazione finora

- Entrep ReportDocumento6 pagineEntrep ReportSato AprilNessuna valutazione finora

- Overview of Mobile Payments WhitepaperDocumento14 pagineOverview of Mobile Payments WhitepapertderuvoNessuna valutazione finora

- Case Study ReportDocumento7 pagineCase Study ReportSeigner JiNessuna valutazione finora

- Banks ThesisDocumento7 pagineBanks Thesismichelleadamserie100% (2)

- Online or Offline? The Rise of Peer To Peer Lending in MicrofinanceDocumento11 pagineOnline or Offline? The Rise of Peer To Peer Lending in MicrofinanceNgọc Minh Đỗ NguyễnNessuna valutazione finora

- E Payments in MauritiusDocumento3 pagineE Payments in Mauritiuskurs23Nessuna valutazione finora

- Bcreg20230103a1 PDFDocumento3 pagineBcreg20230103a1 PDFMalcolm PietersenNessuna valutazione finora

- (English Finance Management Project Strategic) Financial Decision Making - Expert SystemsDocumento7 pagine(English Finance Management Project Strategic) Financial Decision Making - Expert SystemsVirencarpediemNessuna valutazione finora

- Final Project On E BankingDocumento71 pagineFinal Project On E BankingTarun Dhiman0% (2)

- Banking TrendsDocumento18 pagineBanking TrendsSiya SunilNessuna valutazione finora

- Information System For ManagersDocumento11 pagineInformation System For ManagersRupesh SinghNessuna valutazione finora

- Stablecoins Presentation TranscriptDocumento7 pagineStablecoins Presentation TranscriptANessuna valutazione finora

- Overview of Major Trends Affecting Banking Industry (4.0, Blockchain, AI, Fintech, Digital Transformation, ) Influences, ChallengesDocumento4 pagineOverview of Major Trends Affecting Banking Industry (4.0, Blockchain, AI, Fintech, Digital Transformation, ) Influences, ChallengesÁnh NguyệtNessuna valutazione finora

- GAO Report On FintechDocumento71 pagineGAO Report On FintechCrowdfundInsiderNessuna valutazione finora

- Thesis Payment SystemsDocumento4 pagineThesis Payment Systemsebonybatesshreveport100% (2)

- Fintech's Road To Regulatory Acceptance Is Just Starting - PaymentsSourceDocumento4 pagineFintech's Road To Regulatory Acceptance Is Just Starting - PaymentsSourceLondonguyNessuna valutazione finora

- Offline Banking Network in International Banking System 03Documento5 pagineOffline Banking Network in International Banking System 03erol1656Nessuna valutazione finora

- CCCDocumento3 pagineCCCvibhi.19356Nessuna valutazione finora

- Financial Inclusion in PakistanDocumento10 pagineFinancial Inclusion in Pakistanmehar noorNessuna valutazione finora

- PHI PaperDocumento8 paginePHI PaperrgyasuylmhwkhqckrzNessuna valutazione finora

- The Illicit Cash Act One PagerDocumento2 pagineThe Illicit Cash Act One PagerMarkWarner100% (1)

- Banking Sector-An Overview: Syed Asad Raza HBLDocumento39 pagineBanking Sector-An Overview: Syed Asad Raza HBL007tahir007Nessuna valutazione finora

- Bank ScamsDocumento13 pagineBank ScamsUday SharmaNessuna valutazione finora

- Ms Mwelwa: School of Business, Economics and Management Science Bba 170 Business LawDocumento10 pagineMs Mwelwa: School of Business, Economics and Management Science Bba 170 Business LawdanielNessuna valutazione finora

- 1.1 Introduction of E-BankingDocumento33 pagine1.1 Introduction of E-BankingahmedtaniNessuna valutazione finora

- Prospects and Problems of Information Technology in Banking Sector in NigeriaDocumento16 pagineProspects and Problems of Information Technology in Banking Sector in NigeriaAnonymous RoAnGpANessuna valutazione finora

- Implications For Central Banks of The Development of Electronic MoneyDocumento20 pagineImplications For Central Banks of The Development of Electronic MoneyAnonymous PnXCkKIagNessuna valutazione finora

- AMS Client Services Agreement VFDocumento5 pagineAMS Client Services Agreement VFGary AndersonNessuna valutazione finora

- Account Statement From 1 Apr 2023 To 31 Oct 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento3 pagineAccount Statement From 1 Apr 2023 To 31 Oct 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceBhavik NasitNessuna valutazione finora

- LawDocumento3 pagineLawKhenett Ramirez PuertoNessuna valutazione finora

- Sap SD User Manual PDFDocumento286 pagineSap SD User Manual PDFkrishnacfp232Nessuna valutazione finora

- Ref - No. 7854912-21572723-6: Syed AliDocumento6 pagineRef - No. 7854912-21572723-6: Syed AliPrince AliNessuna valutazione finora

- Airwallex Embedded Finance ReportDocumento26 pagineAirwallex Embedded Finance ReportBeltan TönükNessuna valutazione finora

- Gsis SummaryDocumento11 pagineGsis SummaryMary Jane Katipunan CalumbaNessuna valutazione finora

- Bank of America Bank StatementDocumento4 pagineBank of America Bank Statementiimoadi333Nessuna valutazione finora

- Occupational Standard: Accounts and Budget Support Level III Unit Title Administer Financial Accounts Unit Code Unit DescriptorDocumento3 pagineOccupational Standard: Accounts and Budget Support Level III Unit Title Administer Financial Accounts Unit Code Unit DescriptormulualemNessuna valutazione finora

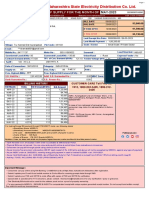

- Bill 670 502039075170 202305Documento5 pagineBill 670 502039075170 202305pravin ghatgeNessuna valutazione finora

- Avalon Investment v. Mukesh BrokerageDocumento7 pagineAvalon Investment v. Mukesh BrokerageAdyasha NandaNessuna valutazione finora

- Forest Hills Logistics Corporation - PafDocumento1 paginaForest Hills Logistics Corporation - PafSaiNessuna valutazione finora

- Qutatation For CourierDocumento17 pagineQutatation For CourierSaurabh SinghNessuna valutazione finora

- RT 05 2019Documento3 pagineRT 05 2019deepusvvpNessuna valutazione finora

- E-Commerce and Digital MarketingDocumento164 pagineE-Commerce and Digital Marketingpradip suryawanshiNessuna valutazione finora

- View SoaDocumento6 pagineView SoaJypy Torrejos100% (1)

- Proposal Penjualan Tanah Berbahasa InggrisDocumento17 pagineProposal Penjualan Tanah Berbahasa InggrisKang SalimNessuna valutazione finora

- Fee Management System - SRSDocumento13 pagineFee Management System - SRSKshitij Minocha75% (4)

- The New Government Accounting System ManualDocumento35 pagineThe New Government Accounting System ManualelminvaldezNessuna valutazione finora

- PDF Audit of Cash Roque 2018 1 Compress PDFDocumento87 paginePDF Audit of Cash Roque 2018 1 Compress PDFFernando III PerezNessuna valutazione finora

- MCQ - PC 21 - Civil Accounts Manual (CAM)Documento13 pagineMCQ - PC 21 - Civil Accounts Manual (CAM)DEVI SINGH MEENANessuna valutazione finora

- LC PC ConfigurationDocumento2 pagineLC PC ConfigurationmoorthykemNessuna valutazione finora

- Dispatcher To Carrier Template 3Documento7 pagineDispatcher To Carrier Template 3Daniel JacksonNessuna valutazione finora

- 1 Exercises - MM - enDocumento14 pagine1 Exercises - MM - enSyed Osama Ali ShahNessuna valutazione finora

- Order Form For CIPAC Pre-Published Methods: InstructionDocumento6 pagineOrder Form For CIPAC Pre-Published Methods: Instructionfarida belarbiNessuna valutazione finora

- Madras Fertilizer Limited (A Govt. of India Undertaking) Manali, Chennai 600 068 Notice Inviting Tender Procurement of Cat Ladder G.IDocumento20 pagineMadras Fertilizer Limited (A Govt. of India Undertaking) Manali, Chennai 600 068 Notice Inviting Tender Procurement of Cat Ladder G.IEliyas YesudossNessuna valutazione finora

- Acosj-P: Java Card - PBOC 3.0Documento22 pagineAcosj-P: Java Card - PBOC 3.0Alfi AlirezaNessuna valutazione finora

- Consolidated Bill: Mrs Nupur Roy 10/A Allenby Road KOLKATA 700020 19006167001 21/05/15 AC InstallationDocumento2 pagineConsolidated Bill: Mrs Nupur Roy 10/A Allenby Road KOLKATA 700020 19006167001 21/05/15 AC Installationkohinoor_roy5447Nessuna valutazione finora

- Call FlowDocumento4 pagineCall FlowJan Kathleen LapitanNessuna valutazione finora

- Instructions 1 PDFDocumento2 pagineInstructions 1 PDFMhyla CunananNessuna valutazione finora

- Ben & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooDa EverandBen & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooValutazione: 5 su 5 stelle5/5 (2)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingDa EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingValutazione: 4.5 su 5 stelle4.5/5 (97)

- AI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersDa EverandAI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersNessuna valutazione finora

- Business Law: a QuickStudy Digital Reference GuideDa EverandBusiness Law: a QuickStudy Digital Reference GuideNessuna valutazione finora

- Introduction to Negotiable Instruments: As per Indian LawsDa EverandIntroduction to Negotiable Instruments: As per Indian LawsValutazione: 5 su 5 stelle5/5 (1)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorDa EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorValutazione: 4.5 su 5 stelle4.5/5 (132)

- The SHRM Essential Guide to Employment Law, Second Edition: A Handbook for HR Professionals, Managers, Businesses, and OrganizationsDa EverandThe SHRM Essential Guide to Employment Law, Second Edition: A Handbook for HR Professionals, Managers, Businesses, and OrganizationsNessuna valutazione finora

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorDa EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorValutazione: 4.5 su 5 stelle4.5/5 (63)

- Secrecy World: Inside the Panama Papers Investigation of Illicit Money Networks and the Global EliteDa EverandSecrecy World: Inside the Panama Papers Investigation of Illicit Money Networks and the Global EliteValutazione: 4.5 su 5 stelle4.5/5 (6)

- LLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessDa EverandLLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessValutazione: 5 su 5 stelle5/5 (1)

- Public Finance: Legal Aspects: Collective monographDa EverandPublic Finance: Legal Aspects: Collective monographNessuna valutazione finora

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsDa EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsValutazione: 5 su 5 stelle5/5 (24)

- Indian Polity with Indian Constitution & Parliamentary AffairsDa EverandIndian Polity with Indian Constitution & Parliamentary AffairsNessuna valutazione finora

- Contract Law in America: A Social and Economic Case StudyDa EverandContract Law in America: A Social and Economic Case StudyNessuna valutazione finora

- The Streetwise Guide to Going Broke without Losing your ShirtDa EverandThe Streetwise Guide to Going Broke without Losing your ShirtNessuna valutazione finora

- International Business Law: Cases and MaterialsDa EverandInternational Business Law: Cases and MaterialsValutazione: 5 su 5 stelle5/5 (1)

- How to Win a Merchant Dispute or Fraudulent Chargeback CaseDa EverandHow to Win a Merchant Dispute or Fraudulent Chargeback CaseNessuna valutazione finora

- Corporate Law: A Handbook for Managers: Volume oneDa EverandCorporate Law: A Handbook for Managers: Volume oneNessuna valutazione finora

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementDa EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementValutazione: 4.5 su 5 stelle4.5/5 (20)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistDa EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistValutazione: 4 su 5 stelle4/5 (34)

- The Curse of Bigness: Antitrust in the New Gilded AgeDa EverandThe Curse of Bigness: Antitrust in the New Gilded AgeValutazione: 3.5 su 5 stelle3.5/5 (4)

- Side Hustles for Dummies: The Key to Unlocking Extra Income and Entrepreneurial Success through Side HustlesDa EverandSide Hustles for Dummies: The Key to Unlocking Extra Income and Entrepreneurial Success through Side HustlesNessuna valutazione finora

- The Startup Visa: U.S. Immigration Visa Guide for Startups and FoundersDa EverandThe Startup Visa: U.S. Immigration Visa Guide for Startups and FoundersNessuna valutazione finora