Potrebbero piacerti anche

- Authorized Letter For Verification of Fund-RMBDocumento2 pagineAuthorized Letter For Verification of Fund-RMBAhmad Fauzi MehatNessuna valutazione finora

- Bond Pricing in The MarketDocumento53 pagineBond Pricing in The MarketAhmad Fauzi MehatNessuna valutazione finora

- Rentas ModuleDocumento1 paginaRentas ModuleAhmad Fauzi MehatNessuna valutazione finora

- A BeginnerDocumento9 pagineA BeginnerAhmad Fauzi MehatNessuna valutazione finora

- A Few Examples of How A Different Margin Could Affect Your Transaction FollowDocumento6 pagineA Few Examples of How A Different Margin Could Affect Your Transaction FollowAhmad Fauzi MehatNessuna valutazione finora

- BPPM FulltextDocumento673 pagineBPPM FulltextAhmad Fauzi MehatNessuna valutazione finora

- Exchange Control RulesDocumento14 pagineExchange Control RulesAhmad Fauzi Mehat100% (1)

- Roll On or Roll of Process FlowsDocumento11 pagineRoll On or Roll of Process FlowsAhmad Fauzi MehatNessuna valutazione finora

- Welcome To The Gold Guidelines: Page 1 of 9Documento9 pagineWelcome To The Gold Guidelines: Page 1 of 9Ahmad Fauzi MehatNessuna valutazione finora

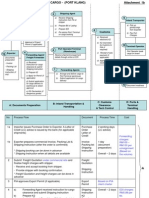

- Export + Import Process Flow - Break Bulk Cargo 27072010Documento11 pagineExport + Import Process Flow - Break Bulk Cargo 27072010Ahmad Fauzi Mehat100% (1)

- Suggested End of Chapter 5 SolutionsDocumento8 pagineSuggested End of Chapter 5 SolutionsAhmad Fauzi MehatNessuna valutazione finora

- Dry Bulk Cargo - (Import and Export)Documento12 pagineDry Bulk Cargo - (Import and Export)Ahmad Fauzi Mehat100% (1)

- World Bank Report FinalDocumento76 pagineWorld Bank Report FinalAhmad Fauzi MehatNessuna valutazione finora

- Valuation of Debt Instruments: Debt Securities Are Government Securities (Government Bonds, Government BillsDocumento13 pagineValuation of Debt Instruments: Debt Securities Are Government Securities (Government Bonds, Government BillsJoslin FernandesNessuna valutazione finora

- Swift Standards Category 7 Documentary Credits & GuaranteesDocumento209 pagineSwift Standards Category 7 Documentary Credits & GuaranteesMEGHANALOKSHANessuna valutazione finora

- Malaysia Haulage Charges (Base On Point-Butterworth, Penang)Documento2 pagineMalaysia Haulage Charges (Base On Point-Butterworth, Penang)Ahmad Fauzi MehatNessuna valutazione finora

- BG and SBLCDocumento1 paginaBG and SBLCKwadwo AsaseNessuna valutazione finora

- 30 Currencies Including The G7Documento6 pagine30 Currencies Including The G7Ahmad Fauzi MehatNessuna valutazione finora

- Swift Standards Category 7 Documentary Credits & GuaranteesDocumento209 pagineSwift Standards Category 7 Documentary Credits & GuaranteesMEGHANALOKSHANessuna valutazione finora

- Contract c8Documento9 pagineContract c8Ahmad Fauzi MehatNessuna valutazione finora

- Swift Standards Category 4 Collections Cash LettersDocumento128 pagineSwift Standards Category 4 Collections Cash LettersAhmad Fauzi MehatNessuna valutazione finora

- Bullion Coins BookletDocumento17 pagineBullion Coins BookletAhmad Fauzi MehatNessuna valutazione finora

- Swift Standards Category 6 Treasury Markets Precious Metals MT600 MT699Documento103 pagineSwift Standards Category 6 Treasury Markets Precious Metals MT600 MT699Ahmad Fauzi Mehat100% (1)

- Types of Credit Instruments & Its FeaturesDocumento22 pagineTypes of Credit Instruments & Its Featuresninpra94% (18)

- World Financial Infrastructure and MoneyDocumento129 pagineWorld Financial Infrastructure and MoneyAhmad Fauzi MehatNessuna valutazione finora

- Financial StatementDocumento6 pagineFinancial StatementAhmad Fauzi MehatNessuna valutazione finora

- Banking-Theory-Law and PracticeDocumento151 pagineBanking-Theory-Law and PracticeAhmad Fauzi MehatNessuna valutazione finora

- Mt100 To 199 (Customer Payments)Documento286 pagineMt100 To 199 (Customer Payments)Perez CorazaNessuna valutazione finora

- Samad and Gardner and Cook - Islamic Banking and Finance PDFDocumento18 pagineSamad and Gardner and Cook - Islamic Banking and Finance PDFAhmad Fauzi MehatNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Ar 2008Documento153 pagineAr 2008Faradilah Binti Ajma'inNessuna valutazione finora

- BRM ProjectDocumento23 pagineBRM Projectrbhatter007Nessuna valutazione finora

- Negotiable InstrumentsDocumento20 pagineNegotiable InstrumentsFRANCIS JOSEPH100% (1)

- Risk Management Presentation January 14 2013Documento206 pagineRisk Management Presentation January 14 2013George LekatisNessuna valutazione finora

- GST CHAPTER I PreliminaryDocumento51 pagineGST CHAPTER I PreliminaryElson Antony PaulNessuna valutazione finora

- Chronology of EventsDocumento3 pagineChronology of EventsMonicaShayneVillafuerteNessuna valutazione finora

- PTI Financial Statement For Financial Year 2013-14Documento7 paginePTI Financial Statement For Financial Year 2013-14PTI Official100% (3)

- Emulsion Price List Wef 16-06-2016Documento4 pagineEmulsion Price List Wef 16-06-2016ఉప కార్యనిర్వాహక ఇంజినీరు ర.భ పలమనేరుNessuna valutazione finora

- Credit Rating Lecture 1Documento44 pagineCredit Rating Lecture 1Ahmed AliNessuna valutazione finora

- Mohammad Al-Hawari Tony Ward Leonce Newby: TitleDocumento1 paginaMohammad Al-Hawari Tony Ward Leonce Newby: TitleArbab Usman KhanNessuna valutazione finora

- PST0064 Practical HPHT Drilling and Well Engineering July2015Documento8 paginePST0064 Practical HPHT Drilling and Well Engineering July2015JacobsNessuna valutazione finora

- Estatement PDFDocumento5 pagineEstatement PDFTena Chamberlin100% (1)

- Bai Tap Thuc Hanh MYOB Nang Cao Co Chinh SuaDocumento5 pagineBai Tap Thuc Hanh MYOB Nang Cao Co Chinh SuaquocankNessuna valutazione finora

- JPMCDocumento14 pagineJPMCvenkatNessuna valutazione finora

- EMBMDocumento14 pagineEMBMnafizarafatNessuna valutazione finora

- General BankingDocumento32 pagineGeneral BankingTaanzim JhumuNessuna valutazione finora

- RM - Cash and Cash EquivalentsDocumento3 pagineRM - Cash and Cash Equivalentsncaacademics.nfjpia2324Nessuna valutazione finora

- Pennies A Day QuizDocumento1 paginaPennies A Day QuizZane ZangwillNessuna valutazione finora

- Dao Heng Bank Inc. Etc vs. Spouse Laigo DigestDocumento1 paginaDao Heng Bank Inc. Etc vs. Spouse Laigo DigestLuz Celine CabadingNessuna valutazione finora

- SLM-19667-BBA - Fiancial Markets and InstitutionsDocumento155 pagineSLM-19667-BBA - Fiancial Markets and InstitutionsMadhusudanNessuna valutazione finora

- FGE Module I NewDocumento93 pagineFGE Module I NewGedion100% (3)

- Credit Transactions Compilation #6Documento27 pagineCredit Transactions Compilation #6Vic RabayaNessuna valutazione finora

- Cooperation IvanDocumento3 pagineCooperation IvanEhramNessuna valutazione finora

- Cash ManagementDocumento54 pagineCash Managementash aminNessuna valutazione finora

- Management Information System: M-CommerceDocumento37 pagineManagement Information System: M-Commercesagarg94gmailcomNessuna valutazione finora

- Cs Acct 11 - Assessment Acct 11 - 3Documento3 pagineCs Acct 11 - Assessment Acct 11 - 3Danica del RosarioNessuna valutazione finora

- BPI v. SuarezDocumento2 pagineBPI v. SuarezMarrielDeTorresNessuna valutazione finora

- Internship Report On Credit Policy of Brac Bank LTDDocumento54 pagineInternship Report On Credit Policy of Brac Bank LTDwpushpa23Nessuna valutazione finora

- Evolution of Entrepreneurship in The PhilippinesDocumento17 pagineEvolution of Entrepreneurship in The PhilippinesAndrew Mercader83% (18)