Potrebbero piacerti anche

- Kezia Noble - Text and Phone GameDocumento37 pagineKezia Noble - Text and Phone Gamesignup4ever100% (1)

- Teach Yourself Beginner's Italian PDFDocumento209 pagineTeach Yourself Beginner's Italian PDFRomero E Mayrla100% (14)

- Colloquial Russian The Complete Course For Beginners PDFDocumento317 pagineColloquial Russian The Complete Course For Beginners PDFkoroldariaNessuna valutazione finora

- RDocumento34 pagineRJhoel HuanacoNessuna valutazione finora

- Argus: Tanker FreightDocumento25 pagineArgus: Tanker FreightIvan OsipovNessuna valutazione finora

- Market Report June 130627Documento24 pagineMarket Report June 130627dondo1004Nessuna valutazione finora

- Urea Weekly Market Report 6 Sept17Documento18 pagineUrea Weekly Market Report 6 Sept17Victor VazquezNessuna valutazione finora

- Argus Sulphur (2018-08-02)Documento14 pagineArgus Sulphur (2018-08-02)saeidNessuna valutazione finora

- PM43Documento150 paginePM43William FergusonNessuna valutazione finora

- Verbal Judo 2010Documento3 pagineVerbal Judo 2010William FergusonNessuna valutazione finora

- Using German SinonymsDocumento347 pagineUsing German SinonymsMerjell91% (33)

- At A Glance Guide - International Hull ClausesDocumento26 pagineAt A Glance Guide - International Hull ClausesZoran DimitrijevicNessuna valutazione finora

- ENGLISH FOR SEAFARER MODULE by Rainisa Pratami, S.HumDocumento49 pagineENGLISH FOR SEAFARER MODULE by Rainisa Pratami, S.HumNitour indo100% (3)

- Optimax 200 Jet Drive ManualDocumento72 pagineOptimax 200 Jet Drive ManualcamiloNessuna valutazione finora

- Week 34Documento18 pagineWeek 34notaristisNessuna valutazione finora

- Shipping OutlookDocumento27 pagineShipping OutlookmervynteoNessuna valutazione finora

- Dry BulkDocumento28 pagineDry BulkyousfinacerNessuna valutazione finora

- Tankers Dry Bulk: Published by Fearnresearch 18. September 2013Documento3 pagineTankers Dry Bulk: Published by Fearnresearch 18. September 2013SimmarineNessuna valutazione finora

- Shipping Market Report 17082011Documento18 pagineShipping Market Report 17082011bleuwinzNessuna valutazione finora

- Willis Energy Market Review 2013 PDFDocumento92 pagineWillis Energy Market Review 2013 PDFsushilk28Nessuna valutazione finora

- Worldyards May 2007 NewsletterDocumento20 pagineWorldyards May 2007 Newsletternestor mospanNessuna valutazione finora

- Daily Market Report: Poten & PartnersDocumento1 paginaDaily Market Report: Poten & PartnersalgeriacandaNessuna valutazione finora

- Container Market PDFDocumento3 pagineContainer Market PDFDhruv AgarwalNessuna valutazione finora

- Intermodal Weekly 01-2012Documento8 pagineIntermodal Weekly 01-2012Wisnu KertaningnagoroNessuna valutazione finora

- Intermodal Weekly Market Report 3rd February 2015, Week 5Documento9 pagineIntermodal Weekly Market Report 3rd February 2015, Week 5Budi PrayitnoNessuna valutazione finora

- SeaIntel Sunday Spotlight Issue 100Documento31 pagineSeaIntel Sunday Spotlight Issue 100Alan Roos MurphyNessuna valutazione finora

- Polymerscan: Americas Polymer Spot Price AssessmentsDocumento29 paginePolymerscan: Americas Polymer Spot Price AssessmentsmcontrerjNessuna valutazione finora

- Po 20140910Documento30 paginePo 20140910mcontrerjNessuna valutazione finora

- SSY Chemical WeeklyDocumento3 pagineSSY Chemical WeeklyBeytullah KokoçNessuna valutazione finora

- AMR SummaryDocumento37 pagineAMR SummaryChatkamol KaewbuddeeNessuna valutazione finora

- SRJ Aug Sep 2009Documento76 pagineSRJ Aug Sep 2009majdirossrossNessuna valutazione finora

- DynaLiners Weekly 49-2015Documento12 pagineDynaLiners Weekly 49-2015Somayajula SuryaramNessuna valutazione finora

- Daily Market ReportDocumento1 paginaDaily Market ReportSmitha MohanNessuna valutazione finora

- Builders Risks Insurance ExplainedDocumento2 pagineBuilders Risks Insurance ExplainedIndra SatriaNessuna valutazione finora

- Euro Gas DailyDocumento8 pagineEuro Gas DailyJose DenizNessuna valutazione finora

- LPGDocumento15 pagineLPGMilkiss SweetNessuna valutazione finora

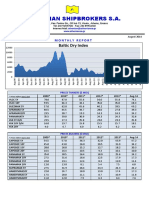

- Monthly report on shipping prices and Baltic Dry IndexDocumento17 pagineMonthly report on shipping prices and Baltic Dry IndexgeorgevarsasNessuna valutazione finora

- Chemf 2007 3Documento124 pagineChemf 2007 3Anupam AsthanaNessuna valutazione finora

- RS Platou Global Support Vessel Monthly February 2012Documento15 pagineRS Platou Global Support Vessel Monthly February 2012kelvin_chong_38Nessuna valutazione finora

- Platts 2020 Outlook Report PDFDocumento21 paginePlatts 2020 Outlook Report PDFKamal ShayedNessuna valutazione finora

- Opr 20181205Documento32 pagineOpr 20181205rojovies24Nessuna valutazione finora

- Complete Reference ListDocumento10 pagineComplete Reference ListdocdumpsterNessuna valutazione finora

- LW 20180731Documento10 pagineLW 20180731Victor FernandezNessuna valutazione finora

- Ihs Markit Is SectorsDocumento2 pagineIhs Markit Is SectorsKapilanNavaratnamNessuna valutazione finora

- Drimcgrawhill - Platts - Oilgram Price Report Nov 96Documento12 pagineDrimcgrawhill - Platts - Oilgram Price Report Nov 96Cristhian AymaNessuna valutazione finora

- 20082311526187Documento92 pagine20082311526187Pooja GaurNessuna valutazione finora

- Weekly Shipping Intelligence ReportDocumento20 pagineWeekly Shipping Intelligence ReportleejingsongNessuna valutazione finora

- Clean Tankerwire 030818Documento7 pagineClean Tankerwire 030818Philippos MichailidisNessuna valutazione finora

- Offshore DrillingDocumento28 pagineOffshore DrillingBull WinkleNessuna valutazione finora

- Compass Weekly Report November 20-2009Documento7 pagineCompass Weekly Report November 20-2009Abdul BasitNessuna valutazione finora

- Market ScanDocumento23 pagineMarket ScanGhasem2010Nessuna valutazione finora

- Chemf 2007 2Documento120 pagineChemf 2007 2Anupam AsthanaNessuna valutazione finora

- Affinity Research Crude Oil Tanker Outlook 2016-11-16Documento64 pagineAffinity Research Crude Oil Tanker Outlook 2016-11-16LondonguyNessuna valutazione finora

- Vam PricesDocumento28 pagineVam PricesMandar J DeshpandeNessuna valutazione finora

- Report 1Documento50 pagineReport 1qwerty1991srNessuna valutazione finora

- India's natural gas pricing policy and its potential impact on energy marketsDocumento12 pagineIndia's natural gas pricing policy and its potential impact on energy marketsJyoti DasguptaNessuna valutazione finora

- Chemical Forecaster Exec Summary TOCDocumento12 pagineChemical Forecaster Exec Summary TOCalgeriacandaNessuna valutazione finora

- Latin America WireDocumento3 pagineLatin America WirepacocardenasNessuna valutazione finora

- Argus: Coal Daily InternationalDocumento15 pagineArgus: Coal Daily InternationalUmang KadivarNessuna valutazione finora

- Monthly Oil Market Report - Feb 2023Documento24 pagineMonthly Oil Market Report - Feb 2023asaNessuna valutazione finora

- (E) Drybulk Daily Report 2018-12-11 (Vol. 180)Documento3 pagine(E) Drybulk Daily Report 2018-12-11 (Vol. 180)amornrat kampitthayakulNessuna valutazione finora

- Dry Bulk Research 9sep16Documento13 pagineDry Bulk Research 9sep16Takis RappasNessuna valutazione finora

- Chemf 2007 1Documento126 pagineChemf 2007 1Anupam AsthanaNessuna valutazione finora

- The Platou Report 2014Documento30 pagineThe Platou Report 2014Tze Yi Tay100% (1)

- Oil Gram Price Report 101911Documento21 pagineOil Gram Price Report 101911Khurram KhaliqNessuna valutazione finora

- Case Study: Ocean Carriers Inc.: Members Team: TitanicDocumento9 pagineCase Study: Ocean Carriers Inc.: Members Team: TitanicAnkitNessuna valutazione finora

- Fixation of JLPL & VSPL Tariff by PNGRB: An Overview of Gail'S Submissions To The BoardDocumento10 pagineFixation of JLPL & VSPL Tariff by PNGRB: An Overview of Gail'S Submissions To The BoardSanjai bhadouriaNessuna valutazione finora

- Ge Shipping Feb 14 PresentationDocumento34 pagineGe Shipping Feb 14 PresentationdiffsoftNessuna valutazione finora

- Osv Outlook ClarksonsDocumento36 pagineOsv Outlook ClarksonstranquocvinhtechNessuna valutazione finora

- Samuel, Geoffrey - Between Buddhism and Science, Between Mind and BodyDocumento20 pagineSamuel, Geoffrey - Between Buddhism and Science, Between Mind and BodylopsopNessuna valutazione finora

- Geo EconomicsDocumento11 pagineGeo EconomicsSamuel Aravind GunnabathulaNessuna valutazione finora

- How To PIDocumento122 pagineHow To PIlordhavok33Nessuna valutazione finora

- Quick Start Guide: Mobile ComputerDocumento2 pagineQuick Start Guide: Mobile ComputerWilliam FergusonNessuna valutazione finora

- SQL TutorialDocumento200 pagineSQL Tutorialroamer10100% (1)

- Infopack 2015 Sitel LisbonDocumento8 pagineInfopack 2015 Sitel LisbonWilliam FergusonNessuna valutazione finora

- The Geopolitical Determinants of Energy SecurityDocumento13 pagineThe Geopolitical Determinants of Energy SecurityWilliam FergusonNessuna valutazione finora

- 065145Documento138 pagine065145strast1Nessuna valutazione finora

- 19.let's Talk About Life An Integrated Approach To Russian ConversationDocumento286 pagine19.let's Talk About Life An Integrated Approach To Russian ConversationWilliam FergusonNessuna valutazione finora

- 3400E Printer User's ManualDocumento126 pagine3400E Printer User's ManualWilliam FergusonNessuna valutazione finora

- TLC Quicktip ExcelDocumento12 pagineTLC Quicktip ExcelRajas GuruNessuna valutazione finora

- Excel Training Guide PDFDocumento13 pagineExcel Training Guide PDFMoiz IsmailNessuna valutazione finora

- Outlook 2010 Advanced User Manual PDFDocumento51 pagineOutlook 2010 Advanced User Manual PDFfeipe_felixNessuna valutazione finora

- The Shape of Jobs To ComeDocumento149 pagineThe Shape of Jobs To Comeapi-21511478Nessuna valutazione finora

- Economic Cycles in Maritime Shipping and PortsDocumento18 pagineEconomic Cycles in Maritime Shipping and PortsWilliam FergusonNessuna valutazione finora

- 21st Century Diplomacy - A Practitioner's Guide (Team Nanban) TMRGDocumento393 pagine21st Century Diplomacy - A Practitioner's Guide (Team Nanban) TMRGJoao Nunes100% (1)

- Using Primavera Project Planner Ver 3 1 CoursewareDocumento250 pagineUsing Primavera Project Planner Ver 3 1 Coursewaresaran1947into100% (14)

- Rodrigues JoaoDocumento6 pagineRodrigues JoaoWilliam FergusonNessuna valutazione finora

- Exercises For Growing Taller - A Mini-GuideDocumento15 pagineExercises For Growing Taller - A Mini-GuideWilliam FergusonNessuna valutazione finora

- Ingles Extraordinaria 3DDocumento16 pagineIngles Extraordinaria 3DsandraNessuna valutazione finora

- Onshore and Offshore DrillingsDocumento44 pagineOnshore and Offshore DrillingsRavi ShankarNessuna valutazione finora

- 03 BulkheadDocumento9 pagine03 BulkheadLucky BoatNessuna valutazione finora

- European Patent Application: Method of Installing Wellhead Platform Using An Offshore UnitDocumento37 pagineEuropean Patent Application: Method of Installing Wellhead Platform Using An Offshore Unitgusyahri001Nessuna valutazione finora

- One Example Is Taken For Calculation Purpose. in This A 70,000 Tons Deadweight OilDocumento4 pagineOne Example Is Taken For Calculation Purpose. in This A 70,000 Tons Deadweight OilFairuzNessuna valutazione finora

- Loadings Affecting On Boats and Small Craft: Markku Hentinen 2016Documento12 pagineLoadings Affecting On Boats and Small Craft: Markku Hentinen 2016notengofffNessuna valutazione finora

- Marine Product Guide 2020Documento33 pagineMarine Product Guide 2020Justin SasangkaNessuna valutazione finora

- Construction Risk For Offshore Units: Risk Assessment Data DirectoryDocumento20 pagineConstruction Risk For Offshore Units: Risk Assessment Data DirectoryAchraf Ben DhifallahNessuna valutazione finora

- American Intelligence Journal: Intelligence Support To The WarfighterDocumento10 pagineAmerican Intelligence Journal: Intelligence Support To The Warfightercarlos perezNessuna valutazione finora

- Navigating Safely with Voyage Planning and RouteingDocumento26 pagineNavigating Safely with Voyage Planning and RouteingXtiane100% (1)

- INTERTANKO CHARTERING QUESTIONNAIRE 88 - OILDocumento8 pagineINTERTANKO CHARTERING QUESTIONNAIRE 88 - OILAne LiberiaNessuna valutazione finora

- Application Form (Ratings)Documento7 pagineApplication Form (Ratings)Taufiq Al Fawazy100% (1)

- Adrift: The Cuban Raft People by Alfredo FernandezDocumento274 pagineAdrift: The Cuban Raft People by Alfredo FernandezArte Público Press0% (1)

- Book Mumbai to Mandwa Ferry TicketDocumento2 pagineBook Mumbai to Mandwa Ferry TicketDinesh MavarkarNessuna valutazione finora

- Data Overview - MARINE PILOTDocumento2 pagineData Overview - MARINE PILOTabdusy syukuurNessuna valutazione finora

- Confusing Questions C10Documento2 pagineConfusing Questions C10Khasy Jeans P. TamposNessuna valutazione finora

- MV Fugro Helmert 2017 LRDocumento2 pagineMV Fugro Helmert 2017 LRDenis RembrantNessuna valutazione finora

- Sailor of FortuneDocumento109 pagineSailor of FortuneLjiljanaNessuna valutazione finora

- Chinese Shipyard ListDocumento54 pagineChinese Shipyard Listbinoyraj2010Nessuna valutazione finora

- 2303-024 MV Meshka at Netherlands (FFE+lifeboats) PDFDocumento3 pagine2303-024 MV Meshka at Netherlands (FFE+lifeboats) PDFManeesh DhyaniNessuna valutazione finora

- Breakwater For Marina Pez Vela'': Quepos - Costa RicaDocumento2 pagineBreakwater For Marina Pez Vela'': Quepos - Costa Ricaeddve23Nessuna valutazione finora

- Frequently Asked Questions (FAQs) CII - Carbon Intensity Indicator - DNVDocumento4 pagineFrequently Asked Questions (FAQs) CII - Carbon Intensity Indicator - DNVanand raoNessuna valutazione finora

- ULJANIK Group Reference List 2Documento14 pagineULJANIK Group Reference List 2waelNessuna valutazione finora

- Another Blow On The Torn Down Wall-The Inclining Experiment: Selahattin Ozsayan Metin TaylanDocumento19 pagineAnother Blow On The Torn Down Wall-The Inclining Experiment: Selahattin Ozsayan Metin TaylanshahjadaNessuna valutazione finora

- Writing and CitylifeDocumento6 pagineWriting and Citylifedipankar89% (9)

- CV - Muhammad Fadel Muharram Latief PDFDocumento1 paginaCV - Muhammad Fadel Muharram Latief PDFMuhammmad Fadel Muharram LatiefNessuna valutazione finora

- Military Courtesy & DisciplineDocumento34 pagineMilitary Courtesy & DisciplineKhristian Jones PanesNessuna valutazione finora