Potrebbero piacerti anche

- Cost-Based Pricing: A Guide for Government ContractorsDa EverandCost-Based Pricing: A Guide for Government ContractorsNessuna valutazione finora

- Contracts, Biddings and Tender:Rule of ThumbDa EverandContracts, Biddings and Tender:Rule of ThumbValutazione: 5 su 5 stelle5/5 (1)

- FIDIC & ICTAD Formula DifferencesDocumento5 pagineFIDIC & ICTAD Formula DifferencesTharaka Kodippily67% (3)

- Cesmm3 NotesDocumento2 pagineCesmm3 Notesdohaqs123Nessuna valutazione finora

- QSMMDocumento158 pagineQSMMizac007Nessuna valutazione finora

- Tips - Estimating Day Work Rates 2nd EditionDocumento52 pagineTips - Estimating Day Work Rates 2nd EditionNisay QSNessuna valutazione finora

- Performance Security NotesDocumento2 paginePerformance Security NotesAvinaash VeeramahNessuna valutazione finora

- Computation of Price Adjustment in A Construction ContractDocumento6 pagineComputation of Price Adjustment in A Construction ContractBarrouz67% (3)

- 20.1 - Contractors ClaimsDocumento1 pagina20.1 - Contractors ClaimsMuhammad ArslanNessuna valutazione finora

- PP Past Year Dec 2015-July 2017-Jan 2018Documento30 paginePP Past Year Dec 2015-July 2017-Jan 2018hani sofia sulaiman100% (1)

- ASAQS Preliminaries 5th Edition - November 2007.PDF-A-22-0-ASAQS Preliminaries 5th Edition - November 2007Documento11 pagineASAQS Preliminaries 5th Edition - November 2007.PDF-A-22-0-ASAQS Preliminaries 5th Edition - November 2007Francois Ehlers100% (1)

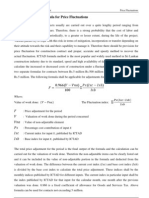

- Price Fluctuations of CostsDocumento10 paginePrice Fluctuations of CostsChinthaka AbeygunawardanaNessuna valutazione finora

- Provisional Sum & Prime CostDocumento13 pagineProvisional Sum & Prime Costiqbal2525Nessuna valutazione finora

- What Is The Meaning of Variation OrderDocumento2 pagineWhat Is The Meaning of Variation OrderFaty BercasioNessuna valutazione finora

- Discussion Paper-01 AnswersDocumento7 pagineDiscussion Paper-01 AnswersShakthi ThiyageswaranNessuna valutazione finora

- Managing Construction ClaimsDocumento31 pagineManaging Construction ClaimshumaidjafriNessuna valutazione finora

- @entrusty Letter of IntentDocumento5 pagine@entrusty Letter of Intentola789Nessuna valutazione finora

- Kees BerendsDocumento5 pagineKees BerendsJavier LopezNessuna valutazione finora

- Dqs389-Interim PaymentDocumento31 pagineDqs389-Interim Paymentillya amyraNessuna valutazione finora

- Provisional Sum and Prime Cost ItemsDocumento4 pagineProvisional Sum and Prime Cost Itemsizyan_zulaikha100% (2)

- Preparing Interim Payment Valuations For Construction Works - Wor PDFDocumento23 paginePreparing Interim Payment Valuations For Construction Works - Wor PDFOumer ShaffiNessuna valutazione finora

- Cost Value ReconciliationDocumento18 pagineCost Value ReconciliationNeminda Dhanushka Kumaradasa0% (1)

- A Practical Guide To The 1999 Red & Yellow Books, Clause8-Commencement, Delays & SuspensionDocumento4 pagineA Practical Guide To The 1999 Red & Yellow Books, Clause8-Commencement, Delays & Suspensiontab77zNessuna valutazione finora

- Form of Tender and Appendix To TenderDocumento4 pagineForm of Tender and Appendix To Tendernandini2309Nessuna valutazione finora

- STD Procedure and Formula For Price AdjustmentDocumento13 pagineSTD Procedure and Formula For Price AdjustmentAbhinav Goel100% (3)

- A Contractor's Guide To The FIDIC Conditions of ContractDocumento1 paginaA Contractor's Guide To The FIDIC Conditions of ContractAnthony GerrardNessuna valutazione finora

- Avoiding Pitfalls in Construction - A Review of FIDIC Forms of ContractDocumento5 pagineAvoiding Pitfalls in Construction - A Review of FIDIC Forms of ContractSohail MalikNessuna valutazione finora

- Top Tips 9 - Preliminaries To The Claim RBDocumento4 pagineTop Tips 9 - Preliminaries To The Claim RBmonsieurkevin30Nessuna valutazione finora

- Commentary:: Amending Clause 13.1 of FIDIC - Protracted NegotiationsDocumento2 pagineCommentary:: Amending Clause 13.1 of FIDIC - Protracted NegotiationsArshad MahmoodNessuna valutazione finora

- Walter Lilly V MacKay - SummaryDocumento30 pagineWalter Lilly V MacKay - SummaryPameswaraNessuna valutazione finora

- Contract ExamDocumento5 pagineContract ExamYeowkoon ChinNessuna valutazione finora

- Cost Plan SampleDocumento3 pagineCost Plan Sampleakg20041100% (1)

- C.6 Price Adjustment Clause (June 2014)Documento16 pagineC.6 Price Adjustment Clause (June 2014)Partha Sarathi DasNessuna valutazione finora

- Case Study - Contractor's Entitlement To Increased Costs On A Fixed Price ContractDocumento3 pagineCase Study - Contractor's Entitlement To Increased Costs On A Fixed Price ContractSridharNessuna valutazione finora

- QS CostControlDocumento7 pagineQS CostControlSyafiq Azme100% (2)

- RICS IConsult - RICS Draft Guidance Note - Developing A Building Procurement Strategy and Selecting An Appropriate Procurement Route APPENDIXDocumento4 pagineRICS IConsult - RICS Draft Guidance Note - Developing A Building Procurement Strategy and Selecting An Appropriate Procurement Route APPENDIXDivina Teja Rebanal-GlinoNessuna valutazione finora

- JCT Suite PDFDocumento18 pagineJCT Suite PDFTamer KhalifaNessuna valutazione finora

- Mathematical Application & Statistics For Quantity SurveyingDocumento7 pagineMathematical Application & Statistics For Quantity SurveyingOds GuysNessuna valutazione finora

- 13) FIDIC Quality Based Consultant Selection GuideDocumento20 pagine13) FIDIC Quality Based Consultant Selection GuideAltugNessuna valutazione finora

- Contract 17 - Roles and Responsibilities Within ProjectsDocumento17 pagineContract 17 - Roles and Responsibilities Within ProjectsRUMMNessuna valutazione finora

- SAP Presenation - Role of Quantity Surveying DeptDocumento26 pagineSAP Presenation - Role of Quantity Surveying DeptRoshan de SilvaNessuna valutazione finora

- QS VariationsDocumento7 pagineQS VariationsSathiya SeelanNessuna valutazione finora

- ProcurementGuidelines Sri Lanka 12juneDocumento79 pagineProcurementGuidelines Sri Lanka 12juneChinthaka SomaratnaNessuna valutazione finora

- Ethics Reading ListDocumento4 pagineEthics Reading Listrainbird7Nessuna valutazione finora

- Bill of Quantity Preparation and Total CDocumento11 pagineBill of Quantity Preparation and Total Celsabet gezahegn100% (1)

- EOT Prolongation CalculationsDocumento16 pagineEOT Prolongation CalculationsKeith Kiks100% (1)

- Matla Qs Company CVDocumento20 pagineMatla Qs Company CVMaha KalaiNessuna valutazione finora

- FIDIC Red BookDocumento112 pagineFIDIC Red BookKristine Cassandra Ogalesco100% (1)

- Practice Notes FOR Quantity Surveyors: TenderingDocumento12 paginePractice Notes FOR Quantity Surveyors: TenderingMok JSNessuna valutazione finora

- Cost Planning RIBA 05-09Documento17 pagineCost Planning RIBA 05-09LokuliyanaNNessuna valutazione finora

- p2010 HKIS - Practice Notes For QS - Final AccountsDocumento7 paginep2010 HKIS - Practice Notes For QS - Final AccountsPameswaraNessuna valutazione finora

- Guide to Good Practice in the Management of Time in Complex ProjectsDa EverandGuide to Good Practice in the Management of Time in Complex ProjectsNessuna valutazione finora

- FIDIC Plant and Design-Build Form of Contract IllustratedDa EverandFIDIC Plant and Design-Build Form of Contract IllustratedNessuna valutazione finora

- Construction Law in the United Arab Emirates and the GulfDa EverandConstruction Law in the United Arab Emirates and the GulfValutazione: 4 su 5 stelle4/5 (1)

- Project Delivery Method A Complete Guide - 2020 EditionDa EverandProject Delivery Method A Complete Guide - 2020 EditionNessuna valutazione finora

- A Contractor's Guide to the FIDIC Conditions of ContractDa EverandA Contractor's Guide to the FIDIC Conditions of ContractNessuna valutazione finora

- The NEC4 Engineering and Construction Contract: A CommentaryDa EverandThe NEC4 Engineering and Construction Contract: A CommentaryNessuna valutazione finora

- Advanced Planning and Scheduling APS Complete Self-Assessment GuideDa EverandAdvanced Planning and Scheduling APS Complete Self-Assessment GuideNessuna valutazione finora

- G9 2019-3t-Western Pro (SM)Documento6 pagineG9 2019-3t-Western Pro (SM)David WebNessuna valutazione finora

- Branding Sri Lanka: - A Case StudyDocumento82 pagineBranding Sri Lanka: - A Case StudyDavid WebNessuna valutazione finora

- Selendiva/Spmc/2021/Civil Works/Tender Doc: Page PP - 1Documento7 pagineSelendiva/Spmc/2021/Civil Works/Tender Doc: Page PP - 1David WebNessuna valutazione finora

- University of Wolverhampton Harward Style Reference Full GuideDocumento31 pagineUniversity of Wolverhampton Harward Style Reference Full GuideDavid WebNessuna valutazione finora

- Maths G-6 P-II EDocumento179 pagineMaths G-6 P-II EDavid WebNessuna valutazione finora

- Guidelines For Interpreting A Turn It in Report (Jan 2020)Documento6 pagineGuidelines For Interpreting A Turn It in Report (Jan 2020)David WebNessuna valutazione finora

- G9 2019-3t-Western Pro (EM)Documento6 pagineG9 2019-3t-Western Pro (EM)David WebNessuna valutazione finora

- G9 2019-3t-Western Pro (SM)Documento6 pagineG9 2019-3t-Western Pro (SM)David WebNessuna valutazione finora

- G9 2019-3t-Western Pro (EM)Documento6 pagineG9 2019-3t-Western Pro (EM)David WebNessuna valutazione finora

- G9 2019-3t-Western Pro (SM)Documento6 pagineG9 2019-3t-Western Pro (SM)David WebNessuna valutazione finora

- G9 2019-3t-Western Pro (EM)Documento6 pagineG9 2019-3t-Western Pro (EM)David WebNessuna valutazione finora

- Which Countries Waste The Most FoodDocumento2 pagineWhich Countries Waste The Most FoodDavid WebNessuna valutazione finora

- G9 2019-3t-Western Pro (SM)Documento6 pagineG9 2019-3t-Western Pro (SM)David WebNessuna valutazione finora

- G9 2019-3t-Western Pro (EM)Documento6 pagineG9 2019-3t-Western Pro (EM)David WebNessuna valutazione finora

- Payment Gateway ProposalDocumento73 paginePayment Gateway ProposalDavid Web100% (2)

- GR 11 Mathematics EM Paper IIDocumento4 pagineGR 11 Mathematics EM Paper IIDavid WebNessuna valutazione finora

- G9 2019-3t-Western Pro (SM)Documento6 pagineG9 2019-3t-Western Pro (SM)David WebNessuna valutazione finora

- Save Food and Sustain LifeDocumento3 pagineSave Food and Sustain LifeDavid WebNessuna valutazione finora

- House BOQDocumento36 pagineHouse BOQDavid Web100% (1)

- GR 11 Mathematics EM Paper IDocumento8 pagineGR 11 Mathematics EM Paper IDavid WebNessuna valutazione finora

- Green Building Standards SLDocumento11 pagineGreen Building Standards SLDavid WebNessuna valutazione finora

- 2nd Email Successfully Activated Account 2Documento1 pagina2nd Email Successfully Activated Account 2David WebNessuna valutazione finora

- The A4 Paper Test Page 1 of 5 2010-10-25 (C) A4 Paper Test - R1.doc Version: R1Documento5 pagineThe A4 Paper Test Page 1 of 5 2010-10-25 (C) A4 Paper Test - R1.doc Version: R1David WebNessuna valutazione finora

- Richmond College First Term Test - 2020 32 E I, Ii: SSéukaâ Úohd, H M Uq JDR Mílaikh - 2020Documento13 pagineRichmond College First Term Test - 2020 32 E I, Ii: SSéukaâ Úohd, H M Uq JDR Mílaikh - 2020David WebNessuna valutazione finora

- NTCEnglishReport2017 PDFDocumento183 pagineNTCEnglishReport2017 PDFDavid WebNessuna valutazione finora

- Specifications For House ConstructionsDocumento2 pagineSpecifications For House ConstructionsDavid WebNessuna valutazione finora

- Food Wastage Directly Propotion To Climate ChangeDocumento3 pagineFood Wastage Directly Propotion To Climate ChangeDavid WebNessuna valutazione finora

- SOP For Payments To Contrctors Consultants by Finance WingDocumento29 pagineSOP For Payments To Contrctors Consultants by Finance WingDavid WebNessuna valutazione finora

- Project Plan Odessa Mobile Technology ProjectDocumento22 pagineProject Plan Odessa Mobile Technology Projectsan1432Nessuna valutazione finora

- Coverpage of The AssignmentDocumento1 paginaCoverpage of The AssignmentDavid WebNessuna valutazione finora

- General ManagementDocumento47 pagineGeneral ManagementRohit KerkarNessuna valutazione finora

- Research MethodologyDocumento5 pagineResearch Methodologysonal gargNessuna valutazione finora

- Diabetes Mellitus in Pediatric: Dr. Wasnaa Hadi AbdullahDocumento30 pagineDiabetes Mellitus in Pediatric: Dr. Wasnaa Hadi AbdullahLily AddamsNessuna valutazione finora

- Montessori Methodology To Teach EnglishDocumento7 pagineMontessori Methodology To Teach EnglishRaul Iriarte AnayaNessuna valutazione finora

- Financing The New VentureDocumento46 pagineFinancing The New VentureAnisha HarshNessuna valutazione finora

- Elliot Kamilla - Literary Film Adaptation Form-Content DilemmaDocumento14 pagineElliot Kamilla - Literary Film Adaptation Form-Content DilemmaDavid SalazarNessuna valutazione finora

- Tales From The Wood RPGDocumento51 pagineTales From The Wood RPGArthur Taylor100% (1)

- Systematic Survey On Smart Home Safety and Security Systems Using The Arduino PlatformDocumento24 pagineSystematic Survey On Smart Home Safety and Security Systems Using The Arduino PlatformGeri MaeNessuna valutazione finora

- A N S W e R-Accion PublicianaDocumento9 pagineA N S W e R-Accion PublicianaEdward Rey EbaoNessuna valutazione finora

- Coordinate Vector: The Standard Representation ExamplesDocumento4 pagineCoordinate Vector: The Standard Representation ExamplesAtikshaNessuna valutazione finora

- Anya Detonnancourt - Student Filmmaker ReflectionsDocumento2 pagineAnya Detonnancourt - Student Filmmaker Reflectionsapi-550252062Nessuna valutazione finora

- Navneet Publications India Limited HardDocumento34 pagineNavneet Publications India Limited Harddyumna100% (1)

- Entrepreneurial Culture - Chapter 13Documento11 pagineEntrepreneurial Culture - Chapter 13bnp guptaNessuna valutazione finora

- Digital Fabrication in Architecture PDFDocumento192 pagineDigital Fabrication in Architecture PDFAndrada Iulia NeagNessuna valutazione finora

- Growth PredictionDocumento101 pagineGrowth PredictionVartika TripathiNessuna valutazione finora

- MLB From 3G SideDocumento16 pagineMLB From 3G Sidemalikst3Nessuna valutazione finora

- MRL WP1 D ANS 013 06 D1 1 Railway Network Key Elements and Main Sub Systems SpecificationDocumento145 pagineMRL WP1 D ANS 013 06 D1 1 Railway Network Key Elements and Main Sub Systems SpecificationMarc MPNessuna valutazione finora

- Two Steps From Hell Full Track ListDocumento13 pagineTwo Steps From Hell Full Track ListneijeskiNessuna valutazione finora

- Family Coping IndexDocumento5 pagineFamily Coping IndexDarcey NicholeNessuna valutazione finora

- 19 March 2018 CcmaDocumento4 pagine19 March 2018 Ccmabronnaf80Nessuna valutazione finora

- Nift B.ftech Gat PaperDocumento7 pagineNift B.ftech Gat PapergoelNessuna valutazione finora

- Lesson Plan Form Day 2 / 3 (4) Webquest Data GatheringDocumento1 paginaLesson Plan Form Day 2 / 3 (4) Webquest Data GatheringMarkJLanzaNessuna valutazione finora

- Course Outline Math 221C Advanced AlgebraDocumento1 paginaCourse Outline Math 221C Advanced Algebraherbertjohn2450% (2)

- Chemical Engineering Science: N. Ratkovich, P.R. Berube, I. NopensDocumento15 pagineChemical Engineering Science: N. Ratkovich, P.R. Berube, I. Nopensvasumalhotra2001Nessuna valutazione finora

- Case Presentation 1Documento18 pagineCase Presentation 1api-390677852Nessuna valutazione finora

- The Creative Bureaucracy 2Documento45 pagineThe Creative Bureaucracy 2IndirannaNessuna valutazione finora

- Applications of Digital - Image-Correlation Techniques To Experimental MechanicsDocumento13 pagineApplications of Digital - Image-Correlation Techniques To Experimental MechanicsGustavo Felicio PerruciNessuna valutazione finora

- 17.5 Return On Investment and Compensation ModelsDocumento20 pagine17.5 Return On Investment and Compensation ModelsjamieNessuna valutazione finora

- 5.1 ReteachDocumento2 pagine5.1 ReteachCarlos Pastrana0% (1)

- Using Games in English Language Learning Mrs Josephine Rama: Jurong Primary SchoolDocumento16 pagineUsing Games in English Language Learning Mrs Josephine Rama: Jurong Primary SchoolChristine NguyễnNessuna valutazione finora