Potrebbero piacerti anche

- Effect of Basel III On Indian BanksDocumento52 pagineEffect of Basel III On Indian BanksSargam Mehta50% (2)

- Case Study Barclays FinalDocumento13 pagineCase Study Barclays FinalShalini Senglo RajaNessuna valutazione finora

- SecuritisationDocumento52 pagineSecuritisationdk6666Nessuna valutazione finora

- Securities Lending Times Issue 218Documento46 pagineSecurities Lending Times Issue 218Securities Lending TimesNessuna valutazione finora

- Banking As A Whole: Investment Bank Commercial BankingDocumento50 pagineBanking As A Whole: Investment Bank Commercial Bankingsalva89830% (1)

- Securities Lending Times Issue 225Documento32 pagineSecurities Lending Times Issue 225Securities Lending TimesNessuna valutazione finora

- Capital and Its StructureDocumento116 pagineCapital and Its Structurev_konduri1177Nessuna valutazione finora

- Basel III For DummiesDocumento4 pagineBasel III For DummiesGill Wallace Hope100% (2)

- Balance of Trade and Balance of Payment NewDocumento27 pagineBalance of Trade and Balance of Payment NewApril OcampoNessuna valutazione finora

- Europe's Sovereign Dept CrisisDocumento5 pagineEurope's Sovereign Dept CrisisCiocoiu Vlad AndreiNessuna valutazione finora

- E-PAPER - NON-BANKING ISLAMIC FINANCIAL INSTITUTIONS - Research Center For Islamic Economics (IKAM)Documento50 pagineE-PAPER - NON-BANKING ISLAMIC FINANCIAL INSTITUTIONS - Research Center For Islamic Economics (IKAM)Muhammad QuraisyNessuna valutazione finora

- FinTech PDFDocumento19 pagineFinTech PDFatikahNessuna valutazione finora

- Commercial Banking Risk ManagementDocumento439 pagineCommercial Banking Risk Managementshank nNessuna valutazione finora

- CAPITAL ADEQUACY BEYOND BASEL Banking, Securities, and InsuranceDocumento354 pagineCAPITAL ADEQUACY BEYOND BASEL Banking, Securities, and Insurancetarekmn1100% (1)

- Retail Banking in IndiaDocumento38 pagineRetail Banking in IndiaYaadrahulkumar MoharanaNessuna valutazione finora

- Asset Liability ManagementDocumento24 pagineAsset Liability ManagementG117Nessuna valutazione finora

- CFR - Mead Fin-MiddleClass PaperDocumento92 pagineCFR - Mead Fin-MiddleClass PaperMrkva2000 account!Nessuna valutazione finora

- Regulatory Sandbox - 270218 FINAL - 2Documento18 pagineRegulatory Sandbox - 270218 FINAL - 2Mustafa Al OdailiNessuna valutazione finora

- DNS Bank (Saurabh)Documento25 pagineDNS Bank (Saurabh)Shoumi MahapatraNessuna valutazione finora

- Blackbook Project On International Banking - 16340Documento67 pagineBlackbook Project On International Banking - 16340Vinod ChaurasiyaNessuna valutazione finora

- Orrick Sponsors CB Insights' Los Angeles Tech Venture Capital Almanac (35 charactersDocumento102 pagineOrrick Sponsors CB Insights' Los Angeles Tech Venture Capital Almanac (35 charactersAGjjjjkjjNessuna valutazione finora

- Public SME Financing and FILP System in JapanDocumento36 paginePublic SME Financing and FILP System in JapanADBI EventsNessuna valutazione finora

- World BankDocumento20 pagineWorld Banksaad124Nessuna valutazione finora

- Customer Buying Behavior With A Focus On Market SegmentationDocumento60 pagineCustomer Buying Behavior With A Focus On Market Segmentationcharlsarora100% (1)

- Debt Pandemic Reinhart Rogoff Bulow TrebeschDocumento5 pagineDebt Pandemic Reinhart Rogoff Bulow TrebeschTinotenda DubeNessuna valutazione finora

- Book BuildingDocumento7 pagineBook BuildingAnonymous 3yqNzCxtTzNessuna valutazione finora

- Prospects of Islamic Finance in KeralaDocumento5 pagineProspects of Islamic Finance in KeralaMuhammed K PalathNessuna valutazione finora

- Rural Marketing Assignment PDFDocumento6 pagineRural Marketing Assignment PDFSriram RajasekaranNessuna valutazione finora

- Article On Rural Entrepreneurship:challenges and OpportunitiesDocumento7 pagineArticle On Rural Entrepreneurship:challenges and OpportunitiesChandrika Das100% (1)

- Fighting Financial Crime Amidst Growing Complexity: T N R AML T ADocumento13 pagineFighting Financial Crime Amidst Growing Complexity: T N R AML T AIván DamiánNessuna valutazione finora

- Nning EthereumDocumento1 paginaNning EthereumfintechNessuna valutazione finora

- SP CMBS Legal and Structured Finance CriteriaDocumento248 pagineSP CMBS Legal and Structured Finance CriteriaVijay GogiaNessuna valutazione finora

- ConclusionDocumento2 pagineConclusionMasud Khan Shakil0% (1)

- Dissertation FinalDocumento49 pagineDissertation Finalaashi gargNessuna valutazione finora

- Pantera IGS Fund PresentationDocumento16 paginePantera IGS Fund PresentationIrakli NinuaNessuna valutazione finora

- Innovation in Banking SectorDocumento4 pagineInnovation in Banking SectorHetvi RajanNessuna valutazione finora

- Social Entrepreneurship Literature ReviewDocumento9 pagineSocial Entrepreneurship Literature ReviewScott J. Jackson0% (1)

- Implementation of Basel Capital Regulatory Requirements in India Disclosure RequirementsDocumento52 pagineImplementation of Basel Capital Regulatory Requirements in India Disclosure RequirementsAKSHAT AGARWALNessuna valutazione finora

- Hilton McCann - Offshore Finance-Cambridge University Press (2006)Documento564 pagineHilton McCann - Offshore Finance-Cambridge University Press (2006)Achraf Ez-zayaniNessuna valutazione finora

- Risk Management in BanksDocumento57 pagineRisk Management in BanksSunil RawatNessuna valutazione finora

- Definition of Microfinance and its Role in Fighting PovertyDocumento6 pagineDefinition of Microfinance and its Role in Fighting PovertyAyush BhavsarNessuna valutazione finora

- Workshop Session 1 PDFDocumento30 pagineWorkshop Session 1 PDFrakhalbanglaNessuna valutazione finora

- Development of Electronic Banking in BangladeshDocumento7 pagineDevelopment of Electronic Banking in BangladeshDr. Mohammad Shamsuddoha100% (2)

- Islamic Finance - Ethics, Concepts, Practice PDFDocumento130 pagineIslamic Finance - Ethics, Concepts, Practice PDFMuhammad TalhaNessuna valutazione finora

- Commercial Bank Financial Management in The Financial Services Industry PDFDocumento2 pagineCommercial Bank Financial Management in The Financial Services Industry PDFPrince0% (1)

- Long Sec Lending PaperDocumento123 pagineLong Sec Lending PaperAl T-sangNessuna valutazione finora

- Project Report On Infosys BECG SEEDocumento33 pagineProject Report On Infosys BECG SEEDEEPAK PRITHANINessuna valutazione finora

- Major Innovations Transforming BankingDocumento6 pagineMajor Innovations Transforming BankingKashishNessuna valutazione finora

- Money LaunderingDocumento7 pagineMoney LaunderingkumarankitgnluNessuna valutazione finora

- Lecture 9 International Credit Market enDocumento42 pagineLecture 9 International Credit Market enElla Marie WicoNessuna valutazione finora

- WealthTech and InsurTechDocumento31 pagineWealthTech and InsurTechAmritha JayanNessuna valutazione finora

- Managing Credit Risk in Corporate Bond Portfolios: A Practitioner's GuideDa EverandManaging Credit Risk in Corporate Bond Portfolios: A Practitioner's GuideNessuna valutazione finora

- Top 100 Hedge Funds to WatchDocumento7 pagineTop 100 Hedge Funds to WatchBen YungNessuna valutazione finora

- Austrade - Investment Management Industry in AustraliaDocumento47 pagineAustrade - Investment Management Industry in Australiappt46Nessuna valutazione finora

- Ccaf 2021 06 Report 2nd Global Alternative Finance Benchmarking Study ReportDocumento197 pagineCcaf 2021 06 Report 2nd Global Alternative Finance Benchmarking Study ReportYasmin AruniNessuna valutazione finora

- The Microfinance IllusionDocumento38 pagineThe Microfinance Illusionbong21Nessuna valutazione finora

- Takaful Investment Portfolios: A Study of the Composition of Takaful Funds in the GCC and MalaysiaDa EverandTakaful Investment Portfolios: A Study of the Composition of Takaful Funds in the GCC and MalaysiaNessuna valutazione finora

- 03 Noyer Financial TurbulenceDocumento3 pagine03 Noyer Financial Turbulencenash666Nessuna valutazione finora

- Regulation of Financial Markets Take Home ExamDocumento22 pagineRegulation of Financial Markets Take Home ExamBrandon TeeNessuna valutazione finora

- What Do Banks Do - What Should They Do - and What Policies Are Needed To Ensure Best Results For The Real EconomyDocumento31 pagineWhat Do Banks Do - What Should They Do - and What Policies Are Needed To Ensure Best Results For The Real EconomyjoebloggsscribdNessuna valutazione finora

- Verdier - 2013 - Political Economy of International Financial RegulationDocumento71 pagineVerdier - 2013 - Political Economy of International Financial RegulationjoebloggsscribdNessuna valutazione finora

- The Financial and Economic Crisis of 2008-2009 and Developing CountriesDocumento340 pagineThe Financial and Economic Crisis of 2008-2009 and Developing CountriesROWLAND PASARIBU100% (2)

- The Role of Derivatives in The Financial Crisis - TranscriptDocumento376 pagineThe Role of Derivatives in The Financial Crisis - TranscriptEsquireNessuna valutazione finora

- Surviving The Cataclysm - Your Guide Through The Greatest Financial Crisis in Human History (1999) - Webster Griffin TarpleyDocumento700 pagineSurviving The Cataclysm - Your Guide Through The Greatest Financial Crisis in Human History (1999) - Webster Griffin TarpleyNicoleNessuna valutazione finora

- Trends in The Concentration of Bank Deposits - Northwest - ST Louis Federal ReserveDocumento4 pagineTrends in The Concentration of Bank Deposits - Northwest - ST Louis Federal ReservejoebloggsscribdNessuna valutazione finora

- OCC's Quarterly Report On Bank Trading and Derivatives Activities Fourth Quarter 2008Documento33 pagineOCC's Quarterly Report On Bank Trading and Derivatives Activities Fourth Quarter 2008ZerohedgeNessuna valutazione finora

- Roghoff and Reinhardt - NBER Paper This Time Is DifferentDocumento124 pagineRoghoff and Reinhardt - NBER Paper This Time Is DifferentKRambis79Nessuna valutazione finora

- Treasury Department Financial Regulatory Reform Blueprint 2008Documento212 pagineTreasury Department Financial Regulatory Reform Blueprint 2008joebloggsscribdNessuna valutazione finora

- Total chronologyoftheFinancialCrisisDocumento112 pagineTotal chronologyoftheFinancialCrisisErich Maria RemarqueNessuna valutazione finora

- The Financial Crisis Causes and Cures by Sony KapoorDocumento112 pagineThe Financial Crisis Causes and Cures by Sony KapoorjoebloggsscribdNessuna valutazione finora

- Financial Crisis Inquiry Report: Final Report of The National Commission On The Causes of The Financial and Economic Crisis in The United StatesDocumento662 pagineFinancial Crisis Inquiry Report: Final Report of The National Commission On The Causes of The Financial and Economic Crisis in The United StatesLisa Stinocher OHanlonNessuna valutazione finora

- NBER-1958-Financial Intermediaries Since 1900-Ch-2-Meaning of The FindingsDocumento38 pagineNBER-1958-Financial Intermediaries Since 1900-Ch-2-Meaning of The FindingsjoebloggsscribdNessuna valutazione finora

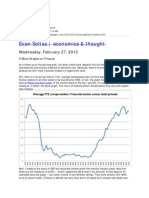

- Soltas Evan 5 Graphs On FinanceDocumento7 pagineSoltas Evan 5 Graphs On FinancejoebloggsscribdNessuna valutazione finora

- Tarpley Cataclysm Globaloney ListDocumento2 pagineTarpley Cataclysm Globaloney ListjoebloggsscribdNessuna valutazione finora

- Lessons From Global Financial CrisisDocumento112 pagineLessons From Global Financial CrisissilberksouzaNessuna valutazione finora

- Soltas Evan 5 Graphs On Finance AddendumDocumento3 pagineSoltas Evan 5 Graphs On Finance AddendumjoebloggsscribdNessuna valutazione finora

- Philosophy of EconomyDocumento359 paginePhilosophy of Economymmaidana2001100% (2)

- MIT-Inequality and Institutions in The 20th CenturyDocumento59 pagineMIT-Inequality and Institutions in The 20th CenturyjoebloggsscribdNessuna valutazione finora

- Money and Power Great PredatorsDocumento257 pagineMoney and Power Great Predatorsdarhan5551100% (1)

- NBER 1958 Financial Intermediaries Since 1900 CH 1 SummaryDocumento13 pagineNBER 1958 Financial Intermediaries Since 1900 CH 1 SummaryjoebloggsscribdNessuna valutazione finora

- SEC 1949 Annual ReportDocumento288 pagineSEC 1949 Annual ReportjoebloggsscribdNessuna valutazione finora

- NBER 1958 Financial Intermediaries Since 1900 Appendix StatisticsDocumento361 pagineNBER 1958 Financial Intermediaries Since 1900 Appendix StatisticsjoebloggsscribdNessuna valutazione finora

- The Mystery of Banking, by Murray RothbardDocumento322 pagineThe Mystery of Banking, by Murray RothbardLudwig von Mises Institute100% (47)

- NBER - 2012 - Voting Rights, Share Concentration, and Leverate at 19th Century Us BanksDocumento55 pagineNBER - 2012 - Voting Rights, Share Concentration, and Leverate at 19th Century Us BanksjoebloggsscribdNessuna valutazione finora

- Lawyer and Banker - 1937 - Lawyers and New Deal - Non-PartisansipDocumento65 pagineLawyer and Banker - 1937 - Lawyers and New Deal - Non-PartisansipjoebloggsscribdNessuna valutazione finora

- NBER - 2003 - Bank Concentration and CrisesDocumento43 pagineNBER - 2003 - Bank Concentration and CrisesjoebloggsscribdNessuna valutazione finora

- Jones, Geoffrey - Globalization and Beauty - A Historical and Firm PerspectiveDocumento32 pagineJones, Geoffrey - Globalization and Beauty - A Historical and Firm PerspectivejoebloggsscribdNessuna valutazione finora

- Jones, Geoffrey - Future of Economic, Business, and Social HistoryDocumento31 pagineJones, Geoffrey - Future of Economic, Business, and Social HistoryjoebloggsscribdNessuna valutazione finora

- Chapter 31 Corporate Finance Ross Test BankDocumento65 pagineChapter 31 Corporate Finance Ross Test Bankali0% (1)

- Annual Return: Form No. Mgt-7Documento23 pagineAnnual Return: Form No. Mgt-7Mali KaleNessuna valutazione finora

- Working Capital ManualDocumento203 pagineWorking Capital ManualDeepika Pandey0% (1)

- Lecture 4 2016 - RamzanDocumento33 pagineLecture 4 2016 - RamzanQed VioNessuna valutazione finora

- HihiDocumento20 pagineHihiCath OquialdaNessuna valutazione finora

- Nike AdidasDocumento8 pagineNike AdidasJaime Andres PazNessuna valutazione finora

- Cost of Capitapractice Set1Documento2 pagineCost of Capitapractice Set1alphaaabNessuna valutazione finora

- Financial Management: Jia, Ning (贾宁) School of Economics and Management Tsinghua UniversityDocumento53 pagineFinancial Management: Jia, Ning (贾宁) School of Economics and Management Tsinghua University王振權Nessuna valutazione finora

- FM AssignmentDocumento12 pagineFM AssignmentNurul Ariffah100% (1)

- Credit Suisse Analyst Valuation Book PDFDocumento144 pagineCredit Suisse Analyst Valuation Book PDFP Win80% (5)

- Powerplay FINALDocumento6 paginePowerplay FINALBachelor's GamingNessuna valutazione finora

- Answer To Exercises-Capital BudgetingDocumento18 pagineAnswer To Exercises-Capital BudgetingAlleuor Quimno50% (2)

- Basel 2 NormsDocumento21 pagineBasel 2 NormsamolreddiwarNessuna valutazione finora

- "Dewan Cement": Income Statement 2008 2007 2006 2005 2004Documento30 pagine"Dewan Cement": Income Statement 2008 2007 2006 2005 2004Asfand Kamal0% (1)

- Capital Market in TanzaniaDocumento11 pagineCapital Market in TanzaniaJohnBenardNessuna valutazione finora

- Addendum 6: 1. Options/Big OI MovementDocumento32 pagineAddendum 6: 1. Options/Big OI MovementRashid KhanNessuna valutazione finora

- Bachelor (Hons) Accounting: Matriculation No: Identity Card No.: Telephone No.: E-Mail: Learning CentreDocumento26 pagineBachelor (Hons) Accounting: Matriculation No: Identity Card No.: Telephone No.: E-Mail: Learning CentreNadiah Atiqah Nor HishamudinNessuna valutazione finora

- Fundamentals of Investing 13th Edition Smart Test BankDocumento37 pagineFundamentals of Investing 13th Edition Smart Test Bankreputedrapergjyn100% (27)

- Impact of Working Capital Management On The Profitability of The Food and Personal Care Products Companies Listed in Karachi Stock Exchange (Finance)Documento41 pagineImpact of Working Capital Management On The Profitability of The Food and Personal Care Products Companies Listed in Karachi Stock Exchange (Finance)Muhammad Nawaz Khan Abbasi100% (1)

- Examining Key Financial Ratios Amongst Scheduled Airlines in North East EuropeDocumento10 pagineExamining Key Financial Ratios Amongst Scheduled Airlines in North East EuropeGeorge WinnerNessuna valutazione finora

- Group 6 Bankruptcy and Restructuring at Marvel Entertainment GroupDocumento9 pagineGroup 6 Bankruptcy and Restructuring at Marvel Entertainment Groupphamvi44552002Nessuna valutazione finora

- Bibaran PatraDocumento40 pagineBibaran PatraAmar PandeyNessuna valutazione finora

- Bear Stearns - Case Study Project ReportDocumento6 pagineBear Stearns - Case Study Project ReportMarketing Expert100% (1)

- Chicago's largest public companies in 2007Documento8 pagineChicago's largest public companies in 2007mayankpdNessuna valutazione finora

- The Appraisal ProfessionDocumento3 pagineThe Appraisal ProfessionJunel AlapaNessuna valutazione finora

- Marry wants to buy bond papers for art classDocumento30 pagineMarry wants to buy bond papers for art classjoven cortezNessuna valutazione finora

- Cheat Sheet - Bloomberg CommodityDocumento1 paginaCheat Sheet - Bloomberg CommoditybasitNessuna valutazione finora

- Poa ExcelDocumento4 paginePoa Excelahm_sarahNessuna valutazione finora

- CH 07Documento59 pagineCH 07Haroon NaseerNessuna valutazione finora

- Business Finance PPT 1Documento10 pagineBusiness Finance PPT 1angelica beatriceNessuna valutazione finora