Potrebbero piacerti anche

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- ImfDocumento30 pagineImfvigneshkarthik23Nessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- 1Documento4 pagine1vigneshkarthik23Nessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Uk Con Customer Centricity DnaDocumento20 pagineUk Con Customer Centricity Dnavigneshkarthik23100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Greek CrisisDocumento10 pagineGreek Crisisvigneshkarthik2333% (3)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (894)

- Conflict ManagementDocumento7 pagineConflict Managementvigneshkarthik23Nessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- ME Unit 1Documento33 pagineME Unit 1vigneshkarthik23Nessuna valutazione finora

- Me Unit 2Documento117 pagineMe Unit 2vigneshkarthik23Nessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Erm FinanceDocumento4 pagineErm Financevigneshkarthik23Nessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Current Size Profit StatementDocumento2 pagineCurrent Size Profit Statementvigneshkarthik23Nessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

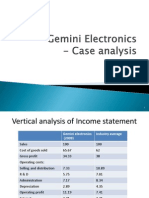

- Vertical analysis of Gemini ElectronicsDocumento5 pagineVertical analysis of Gemini Electronicsvigneshkarthik23100% (2)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- Lorenz CurveDocumento1 paginaLorenz Curvevigneshkarthik23Nessuna valutazione finora

- Business Ethics: Team 5Documento10 pagineBusiness Ethics: Team 5vigneshkarthik23Nessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Role of Regional Rural BanksDocumento17 pagineRole of Regional Rural Banksvigneshkarthik23Nessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Case Bill FrenchDocumento3 pagineCase Bill Frenchvigneshkarthik23Nessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- StakeholdersDocumento12 pagineStakeholdersvigneshkarthik23Nessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Verilog HDL - Samir PalnitkarDocumento403 pagineVerilog HDL - Samir PalnitkarSameer RaichurNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Audit ReportDocumento10 pagineAudit Reportsomnathsingh_hydNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- CMA II 2016 Study Materials CMA Part 2 MDocumento37 pagineCMA II 2016 Study Materials CMA Part 2 Mkopy brayntNessuna valutazione finora

- Financial Statement of A CompanyDocumento49 pagineFinancial Statement of A CompanyApollo Institute of Hospital Administration100% (3)

- ENGINEERING ECONOMY: KEY CONCEPTSDocumento13 pagineENGINEERING ECONOMY: KEY CONCEPTSbabadapbadapNessuna valutazione finora

- Sweet Dreams Inc. Case AnalysisDocumento13 pagineSweet Dreams Inc. Case Analysisdontcare3267% (3)

- Chapter 2 Multiple Choice Answers and SolutionsDocumento25 pagineChapter 2 Multiple Choice Answers and SolutionsMendoza KlariseNessuna valutazione finora

- Akash Clay LTDDocumento64 pagineAkash Clay LTDSathavara KetulNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Advanced Financial Accounting Canadian Canadian 7Th Edition Beechy Solutions Manual Full Chapter PDFDocumento36 pagineAdvanced Financial Accounting Canadian Canadian 7Th Edition Beechy Solutions Manual Full Chapter PDFpaul.colapietro194100% (13)

- 7160 - FAR Preweek ProblemDocumento14 pagine7160 - FAR Preweek ProblemMAS CPAR 93Nessuna valutazione finora

- Audit Risks & Ethical ThreatsDocumento10 pagineAudit Risks & Ethical ThreatsMuhammad TahaNessuna valutazione finora

- Pas 41 AgricultureDocumento5 paginePas 41 Agriculturetrevor.v.philips23Nessuna valutazione finora

- Accounting for Property, Plant and EquipmentDocumento4 pagineAccounting for Property, Plant and EquipmentSheenaNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Annual Statement of Rates: Stamp DutyDocumento205 pagineAnnual Statement of Rates: Stamp DutyJignesh PatelNessuna valutazione finora

- Square D 1990 Net EarningsDocumento9 pagineSquare D 1990 Net EarningsHeni Oktavianti0% (1)

- Accounting Transaction, Services CompanyDocumento3 pagineAccounting Transaction, Services CompanyCahyani PrastutiNessuna valutazione finora

- Chap7 PDFDocumento61 pagineChap7 PDFAshraf Alawneh100% (1)

- Kieso - IFRS - ch11 - IfRS (Depreciation, Impairments, and Depletion)Documento73 pagineKieso - IFRS - ch11 - IfRS (Depreciation, Impairments, and Depletion)Muzi RahayuNessuna valutazione finora

- Ifc Q & A 17 - GeasDocumento5 pagineIfc Q & A 17 - GeasBelat Cruz100% (3)

- Set Off & Carry Forward of LossesDocumento21 pagineSet Off & Carry Forward of LossesanchalNessuna valutazione finora

- Valuation AnalysisDocumento86 pagineValuation Analysisollllllllllo100% (1)

- Case Analysis On Sinclair CompanyDocumento7 pagineCase Analysis On Sinclair CompanyAce ConcepcionNessuna valutazione finora

- Global Engineering Economics 4EDDocumento554 pagineGlobal Engineering Economics 4EDSyed TamzidNessuna valutazione finora

- Chap1 - BA213Documento11 pagineChap1 - BA213kenozin272Nessuna valutazione finora

- Agribusiness Accounting Guide for Non-AccountantsDocumento39 pagineAgribusiness Accounting Guide for Non-AccountantsAlexander Kim Waing100% (1)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Feasibility StudyDocumento19 pagineFeasibility StudySwapnil Srivastava50% (2)

- Urban Water Partners Group ADocumento5 pagineUrban Water Partners Group AAman jhaNessuna valutazione finora

- Mobile Coffee Shop: Feasibility Study ReportDocumento13 pagineMobile Coffee Shop: Feasibility Study ReportBaharu AbebeNessuna valutazione finora

- Fabm2 DlaDocumento100 pagineFabm2 DlaCathlyn San LuisNessuna valutazione finora

- Cut Over StrategyDocumento29 pagineCut Over Strategygenfin100% (1)

- CH 05Documento23 pagineCH 05Damy RoseNessuna valutazione finora