Potrebbero piacerti anche

- Negotiable Instruments 2010Documento12 pagineNegotiable Instruments 2010qanaqNessuna valutazione finora

- CDCS Specimen Paper C - QPDocumento30 pagineCDCS Specimen Paper C - QPNavin ChoudharyNessuna valutazione finora

- Century Egg Dedicated to Carl VincentDocumento31 pagineCentury Egg Dedicated to Carl VincentMary Rose Ramos100% (1)

- Nego Suggested Answers 2008Documento11 pagineNego Suggested Answers 2008farsuyNessuna valutazione finora

- Mid-Terms Negotiable Instrument Questionnaire February 2 2016 Ver 1.2Documento12 pagineMid-Terms Negotiable Instrument Questionnaire February 2 2016 Ver 1.2Eppie SeverinoNessuna valutazione finora

- LIBF Level 4 Certificate For Documentary Credit Specialists (CDCS)Documento30 pagineLIBF Level 4 Certificate For Documentary Credit Specialists (CDCS)Abhay PandereNessuna valutazione finora

- ACCTG 25 Negotiable Instruments Law: Lyceum-Northwestern UniversityDocumento4 pagineACCTG 25 Negotiable Instruments Law: Lyceum-Northwestern UniversityAmie Jane MirandaNessuna valutazione finora

- Delivery of Instrument Key to LiabilityDocumento3 pagineDelivery of Instrument Key to LiabilityAquino, JPNessuna valutazione finora

- Quizzer 2 Pdic SBD Ub Week 14 Set BDocumento7 pagineQuizzer 2 Pdic SBD Ub Week 14 Set Bmariesteinsher0Nessuna valutazione finora

- 151218142343Documento60 pagine151218142343asdf100% (1)

- PT Bank Maybank Syariah Indonesia v Mindo-Trade Sdn Bhd Summary JudgmentDocumento16 paginePT Bank Maybank Syariah Indonesia v Mindo-Trade Sdn Bhd Summary JudgmentTsai Shiang YeapNessuna valutazione finora

- Law Neg o PDFDocumento14 pagineLaw Neg o PDFKendrew SujideNessuna valutazione finora

- Mock 06 001Documento36 pagineMock 06 001masud khan0% (1)

- Bespile SDN BHD (In Liquidation) V Asianshine SDN BHD & OrsDocumento18 pagineBespile SDN BHD (In Liquidation) V Asianshine SDN BHD & OrsSaidatulnajwaNessuna valutazione finora

- CDCS Specimen Paper A - 2017-18Documento35 pagineCDCS Specimen Paper A - 2017-18LêTrungHiếuNessuna valutazione finora

- Sample ExamDocumento2 pagineSample ExamattymauNessuna valutazione finora

- AR Astern Niversity: Atty. Aldren D. Abrigo, CPADocumento3 pagineAR Astern Niversity: Atty. Aldren D. Abrigo, CPARamainne RonquilloNessuna valutazione finora

- (C 01) DBP vs. Sima Wei, 219 SCRA 736, March 9, 1993Documento8 pagine(C 01) DBP vs. Sima Wei, 219 SCRA 736, March 9, 1993JJNessuna valutazione finora

- Nego Final Exam QuestionsDocumento2 pagineNego Final Exam QuestionsResci Angelli Rizada-Nolasco50% (2)

- 12-Development Bank of Rizal v. Sima Wei 219 SCRA 736 (1993)Documento3 pagine12-Development Bank of Rizal v. Sima Wei 219 SCRA 736 (1993)Ronald Alasa-as AtigNessuna valutazione finora

- Adobe Scan 31-Mar-2024Documento24 pagineAdobe Scan 31-Mar-2024Mishra DPNessuna valutazione finora

- Suggested Answers To Bar Exam Questions 2008 On Mercantile LawDocumento13 pagineSuggested Answers To Bar Exam Questions 2008 On Mercantile LawMary LouiseNessuna valutazione finora

- Suggested Answers To Bar Exam Questions 2008 On Mercantile LawDocumento9 pagineSuggested Answers To Bar Exam Questions 2008 On Mercantile LawsevenfivefiveNessuna valutazione finora

- 1991-1996 BAR Mercantile QuestionsDocumento63 pagine1991-1996 BAR Mercantile QuestionsasdgafsdgadfgNessuna valutazione finora

- ACCTG 25 Negotiable Instruments Law: Lyceum-Northwestern UniversityDocumento4 pagineACCTG 25 Negotiable Instruments Law: Lyceum-Northwestern UniversityAmie Jane MirandaNessuna valutazione finora

- 59Documento4 pagine59KAYE JAVELLANANessuna valutazione finora

- Law 20013 Finals ReviewerDocumento9 pagineLaw 20013 Finals ReviewerHans ManaliliNessuna valutazione finora

- Escober, Alon & Associates For Petitioner. Martin D. Pantaleon For Private RespondentsDocumento17 pagineEscober, Alon & Associates For Petitioner. Martin D. Pantaleon For Private RespondentsCarla Eclarin BojosNessuna valutazione finora

- RIVERA, Lyka A. (Assign 4 - Law)Documento4 pagineRIVERA, Lyka A. (Assign 4 - Law)Lysss EpssssNessuna valutazione finora

- COMMREV Nego DigestsDocumento36 pagineCOMMREV Nego DigestsAnge Buenaventura Salazar100% (3)

- 129179-1992-Bank of The Philippine Islands v. Court Of20210424-12-F7qjuzDocumento26 pagine129179-1992-Bank of The Philippine Islands v. Court Of20210424-12-F7qjuzLydia Marie Inocencio-MirabelNessuna valutazione finora

- Development Bank of Rizal v. Sima WeiDocumento6 pagineDevelopment Bank of Rizal v. Sima WeiKaren Patricio LusticaNessuna valutazione finora

- NEGOTIABLE INSTRUMENTS LAWDocumento4 pagineNEGOTIABLE INSTRUMENTS LAWLing EscalanteNessuna valutazione finora

- (A) Pancho Asked The Payor Bank To Recredit His Account. Should The Bank Comply? Explain Fully. (3%)Documento5 pagine(A) Pancho Asked The Payor Bank To Recredit His Account. Should The Bank Comply? Explain Fully. (3%)zhoy26Nessuna valutazione finora

- HCA322D - 2008 BonusclaimDocumento141 pagineHCA322D - 2008 BonusclaimpschilNessuna valutazione finora

- Development Bank of Rizal v. Sima Wei and or Lee Kian HuatDocumento2 pagineDevelopment Bank of Rizal v. Sima Wei and or Lee Kian HuatbearzhugNessuna valutazione finora

- Equity Bank Tanzania LTD Vs Johnelly TZ Company Limited (Civil Appeal 37 of 2020) 2021 TZHC 6076 (22 July 2021)Documento13 pagineEquity Bank Tanzania LTD Vs Johnelly TZ Company Limited (Civil Appeal 37 of 2020) 2021 TZHC 6076 (22 July 2021)kelvinmalwa50Nessuna valutazione finora

- Resa Anti Bouncing Checks LawDocumento2 pagineResa Anti Bouncing Checks LawArielle D.Nessuna valutazione finora

- BPI v. CADocumento23 pagineBPI v. CApistekayawaNessuna valutazione finora

- Suggested Answers To Bar Exam Questions 2008 On Mercantile LawDocumento28 pagineSuggested Answers To Bar Exam Questions 2008 On Mercantile LawRJay JacabanNessuna valutazione finora

- UntitledDocumento3 pagineUntitledJunaid DadayanNessuna valutazione finora

- 2015 Bar Exam Suggested Answers in Mercantile LawDocumento14 pagine2015 Bar Exam Suggested Answers in Mercantile Lawargao100% (1)

- Understanding Contracts of Indemnity and Bank GuaranteesDocumento4 pagineUnderstanding Contracts of Indemnity and Bank GuaranteesPriyanshi VashishtaNessuna valutazione finora

- Nego 2022Documento16 pagineNego 2022crescente pagadduNessuna valutazione finora

- JJ CasesDocumento30 pagineJJ CasesRhose Azcelle MagaoayNessuna valutazione finora

- Nego MCQDocumento13 pagineNego MCQwainie_deroNessuna valutazione finora

- NEGOTIABLE INSTRUMENTS: FUNCTIONS, TYPES, AND PARTIESDocumento3 pagineNEGOTIABLE INSTRUMENTS: FUNCTIONS, TYPES, AND PARTIESWilson Freo Jr.Nessuna valutazione finora

- Mercantile Law ReviewerDocumento13 pagineMercantile Law ReviewerMarjorie Ramirez100% (1)

- Death Claim Settlement Policy SummaryDocumento11 pagineDeath Claim Settlement Policy SummaryPIYUSH YADAVNessuna valutazione finora

- STATE INVESTMENT HOUSE, INC. Vs CADocumento5 pagineSTATE INVESTMENT HOUSE, INC. Vs CAClaudia Rina LapazNessuna valutazione finora

- NegoDocumento8 pagineNegoJica GulaNessuna valutazione finora

- Dev Bank of Rizal VS Sima WeiDocumento4 pagineDev Bank of Rizal VS Sima WeiKristanne Louise YuNessuna valutazione finora

- Development Bank of Rizal Vs Sima Wei PDFDocumento3 pagineDevelopment Bank of Rizal Vs Sima Wei PDFkaren mae bollerNessuna valutazione finora

- Section 1. Interrogatories To Parties Service Thereof. - Upon Ex Parte Motion, Any Party Desiring To ElicitDocumento3 pagineSection 1. Interrogatories To Parties Service Thereof. - Upon Ex Parte Motion, Any Party Desiring To ElicitAmerigo VespucciNessuna valutazione finora

- 2015 Bar Exam Suggested Answers in Mercantile Law by The UP Law ComplexDocumento14 pagine2015 Bar Exam Suggested Answers in Mercantile Law by The UP Law ComplexLenar GamoraNessuna valutazione finora

- DBP Vs Sima WeiDocumento5 pagineDBP Vs Sima WeiKrister VallenteNessuna valutazione finora

- 2008 Bar Questions and AnswersDocumento15 pagine2008 Bar Questions and AnswersimoymitoNessuna valutazione finora

- How To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionDa EverandHow To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionNessuna valutazione finora

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)Da EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)Nessuna valutazione finora

- The 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsDa EverandThe 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsValutazione: 5 su 5 stelle5/5 (1)

- Geography P1 Memo Eng Nov 2008 FinalDocumento17 pagineGeography P1 Memo Eng Nov 2008 FinalPatrick Van WykNessuna valutazione finora

- Geography P2 Memo Eng Nov 2008 FinalDocumento9 pagineGeography P2 Memo Eng Nov 2008 FinalqanaqNessuna valutazione finora

- Geography P1 Nov 2008 EngDocumento25 pagineGeography P1 Nov 2008 EngqanaqNessuna valutazione finora

- Hospitality Studies Memo Nov 2008 Eng MemoDocumento14 pagineHospitality Studies Memo Nov 2008 Eng MemoqanaqNessuna valutazione finora

- History P1 Eng. Nov. 2008Documento10 pagineHistory P1 Eng. Nov. 2008qanaq100% (1)

- History P1 Nov 2010 Memo EngDocumento30 pagineHistory P1 Nov 2010 Memo EngqanaqNessuna valutazione finora

- History p2 Nov 2008 Memo EngDocumento30 pagineHistory p2 Nov 2008 Memo Engqanaq0% (1)

- History P2 Eng Nov 2008Documento10 pagineHistory P2 Eng Nov 2008qanaqNessuna valutazione finora

- Life Sciences P2 Nov 2008 Eng Memo FinalDocumento13 pagineLife Sciences P2 Nov 2008 Eng Memo FinalqanaqNessuna valutazione finora

- Life Sciences P2 Nov 2008 Eng Memo FinalDocumento13 pagineLife Sciences P2 Nov 2008 Eng Memo FinalqanaqNessuna valutazione finora

- IT P2 Eng Memo Nov 2008Documento15 pagineIT P2 Eng Memo Nov 2008qanaqNessuna valutazione finora

- Life Sciences P2 Nov 2008 Eng Memo FinalDocumento13 pagineLife Sciences P2 Nov 2008 Eng Memo FinalqanaqNessuna valutazione finora

- Information Technology P1 Eng. Nov. 2008Documento32 pagineInformation Technology P1 Eng. Nov. 2008qanaqNessuna valutazione finora

- National Senior Certificate: Grade 12Documento21 pagineNational Senior Certificate: Grade 12qanaqNessuna valutazione finora

- Life Science P1 Nov 2008 Eng Memo FinalDocumento13 pagineLife Science P1 Nov 2008 Eng Memo Finalbellydanceafrica9540Nessuna valutazione finora

- Life Science P1 Nov 2008 EngDocumento18 pagineLife Science P1 Nov 2008 EngqanaqNessuna valutazione finora

- Mechanical Technology Nov 2008 EngDocumento25 pagineMechanical Technology Nov 2008 EngqanaqNessuna valutazione finora

- Music P1 Nov 2008 EngDocumento26 pagineMusic P1 Nov 2008 EngqanaqNessuna valutazione finora

- National Senior Certificate: Grade 12Documento13 pagineNational Senior Certificate: Grade 12qanaqNessuna valutazione finora

- 20140109151014542Documento7 pagine20140109151014542qanaqNessuna valutazione finora

- Physical Sciences P2 Memo Eng & Afr Nov 2008Documento18 paginePhysical Sciences P2 Memo Eng & Afr Nov 2008qanaq50% (2)

- Maths Literacy P2 Nov 2008 Memo EngDocumento22 pagineMaths Literacy P2 Nov 2008 Memo Engqanaq25% (4)

- Maths Literacy P1 Nov 2008 Memo AfrDocumento17 pagineMaths Literacy P1 Nov 2008 Memo AfrqanaqNessuna valutazione finora

- Life Sciences P2 Nov 2008 EngDocumento16 pagineLife Sciences P2 Nov 2008 EngqanaqNessuna valutazione finora

- Terms and Conditions: Prepaid RentalsDocumento1 paginaTerms and Conditions: Prepaid RentalsqanaqNessuna valutazione finora

- Mechanical Technology Nov 2008 Eng MemoDocumento19 pagineMechanical Technology Nov 2008 Eng MemoqanaqNessuna valutazione finora

- Music P2 Nov 2008 Eng MemoDocumento12 pagineMusic P2 Nov 2008 Eng MemoqanaqNessuna valutazione finora

- Music P1 Nov 2008 Eng MemoDocumento29 pagineMusic P1 Nov 2008 Eng MemoqanaqNessuna valutazione finora

- Maths Literacy P1 Nov 2008 Memo EngDocumento17 pagineMaths Literacy P1 Nov 2008 Memo Engqanaq100% (2)

- Mechanical Technology Nov 2008 Eng MemoDocumento19 pagineMechanical Technology Nov 2008 Eng MemoqanaqNessuna valutazione finora

- 3 Duets From J.S. Bach's English SuitesDocumento8 pagine3 Duets From J.S. Bach's English SuitesSilvia MacejovaNessuna valutazione finora

- People V ViernesDocumento14 paginePeople V Viernesjack fackageNessuna valutazione finora

- Kramer - Dynamic of Destruction Culture and Mass Killing in The First World War (2007) PDFDocumento447 pagineKramer - Dynamic of Destruction Culture and Mass Killing in The First World War (2007) PDFJeffNessuna valutazione finora

- FC Steaua BucurestiDocumento17 pagineFC Steaua BucurestiMartina MartyNessuna valutazione finora

- Policy Guidelines On The Proper Use of Computer and NetworkDocumento9 paginePolicy Guidelines On The Proper Use of Computer and NetworkJeanette Gonzales Aliman0% (1)

- War Crimes: AFP PNPDocumento19 pagineWar Crimes: AFP PNPsensei.adoradorNessuna valutazione finora

- Gabionsa v. CADocumento11 pagineGabionsa v. CADennis VelasquezNessuna valutazione finora

- Vda. de Bautista V Marcos DigestDocumento1 paginaVda. de Bautista V Marcos DigestBenedict EstrellaNessuna valutazione finora

- Emma Rothschild The Quest For World Order What Is 1995Documento47 pagineEmma Rothschild The Quest For World Order What Is 1995Marin100% (1)

- Articles Price CollusionDocumento7 pagineArticles Price CollusionNidhi ShahNessuna valutazione finora

- Consolidated Statements of Operations: Years Ended September 29, 2012 September 24, 2011 September 25, 2010Documento5 pagineConsolidated Statements of Operations: Years Ended September 29, 2012 September 24, 2011 September 25, 2010Basit Ali ChaudhryNessuna valutazione finora

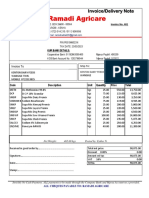

- Ramadi Agricare: Invoice/Delivery NoteDocumento2 pagineRamadi Agricare: Invoice/Delivery NoteRamadi cyberNessuna valutazione finora

- Copyright SamplingDocumento256 pagineCopyright SamplingsukanmikNessuna valutazione finora

- PSAK 51-RevDocumento5 paginePSAK 51-Revapi-3708783Nessuna valutazione finora

- Gashem Shookat Baksh v. Court of Appeals GR No. 97336. February 19, 1993Documento3 pagineGashem Shookat Baksh v. Court of Appeals GR No. 97336. February 19, 1993Debroah Faith PajarilloNessuna valutazione finora

- Kalinchowk Darshan Limited PDFDocumento52 pagineKalinchowk Darshan Limited PDFMandip DcNessuna valutazione finora

- Daphne Hermetic Oil Fv50s Eu1Documento3 pagineDaphne Hermetic Oil Fv50s Eu1torqueuNessuna valutazione finora

- Property Regimes Self-TestDocumento16 pagineProperty Regimes Self-TestMardeePinedaBorcena33% (18)

- Digitalization of Work in The Mirror of Labour Law Principles in HungaryDocumento11 pagineDigitalization of Work in The Mirror of Labour Law Principles in HungaryGlobal Research and Development ServicesNessuna valutazione finora

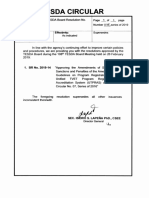

- TESDA Circular No. 038-2019Documento12 pagineTESDA Circular No. 038-2019Leonicia MarquinezNessuna valutazione finora

- Solution for Chapter 23 causality and transformationsDocumento8 pagineSolution for Chapter 23 causality and transformationsSveti JeronimNessuna valutazione finora

- Ias 40 - Presentation PDFDocumento21 pagineIas 40 - Presentation PDFAnonymous ns1HpZKAfNessuna valutazione finora

- Ched-Dbm Joint Memorandum Circular No. 2017-1Documento13 pagineChed-Dbm Joint Memorandum Circular No. 2017-1John Ceasar PascoNessuna valutazione finora

- FMBO 205 IInd Sem QBDocumento18 pagineFMBO 205 IInd Sem QBanishaNessuna valutazione finora

- Developing Good Work EthicDocumento3 pagineDeveloping Good Work Ethiclance100% (1)

- Calculate The Standard Free Energy For The Following Reaction by Using Given DataDocumento5 pagineCalculate The Standard Free Energy For The Following Reaction by Using Given DatamuraliMuNessuna valutazione finora

- What Is Forensic AccountingDocumento2 pagineWhat Is Forensic AccountingJonhmark AniñonNessuna valutazione finora

- FA1 NotesDocumento270 pagineFA1 Notesdaneq80% (10)

- Cantesco SolventDocumento5 pagineCantesco Solventmasv792512Nessuna valutazione finora

- Questions On Alphabet Series PDFDocumento4 pagineQuestions On Alphabet Series PDFGajendra JoshiNessuna valutazione finora