Potrebbero piacerti anche

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- KW Branding Identity GuideDocumento44 pagineKW Branding Identity GuidedcsudweeksNessuna valutazione finora

- Procedure For Import of Gold Carried by Passenger Travelling by AirDocumento3 pagineProcedure For Import of Gold Carried by Passenger Travelling by AirYulia PuspitasariNessuna valutazione finora

- Short Term Financial Management 3rd Edition Maness Test BankDocumento5 pagineShort Term Financial Management 3rd Edition Maness Test Bankjuanlucerofdqegwntai100% (16)

- Philippine Laws On WomenDocumento56 paginePhilippine Laws On WomenElle BanigoosNessuna valutazione finora

- ReservationsDocumento30 pagineReservationsplasmadragNessuna valutazione finora

- NHA V BasaDocumento3 pagineNHA V BasaKayeNessuna valutazione finora

- Miske DocumentsDocumento14 pagineMiske DocumentsHNN100% (1)

- Lancesoft Offer LetterDocumento5 pagineLancesoft Offer LetterYogendraNessuna valutazione finora

- Blue Ocean StrategyDocumento247 pagineBlue Ocean StrategyFadiNessuna valutazione finora

- Professional Practice of Accounting With AnswerDocumento12 pagineProfessional Practice of Accounting With AnswerRNessuna valutazione finora

- The Forrester Wave PDFDocumento15 pagineThe Forrester Wave PDFManish KumarNessuna valutazione finora

- FI Account Opening Form 1Documento3 pagineFI Account Opening Form 1gopal_psbNessuna valutazione finora

- RTIDocumento138 pagineRTIgopal_psbNessuna valutazione finora

- Direct TaxesDocumento15 pagineDirect Taxesgopal_psbNessuna valutazione finora

- Ratio Analysis: R K MohantyDocumento30 pagineRatio Analysis: R K MohantySulav SheeNessuna valutazione finora

- 01 - Clearing ActivtiesDocumento14 pagine01 - Clearing ActivtiesBarjesh_Lamba_2009Nessuna valutazione finora

- 2 - Job Card For Splitting and Merging of ChequebooksDocumento7 pagine2 - Job Card For Splitting and Merging of Chequebooksgopal_psbNessuna valutazione finora

- Std11 TamilDocumento133 pagineStd11 Tamilgopal_psbNessuna valutazione finora

- 01 - Clearing ActivtiesDocumento14 pagine01 - Clearing ActivtiesBarjesh_Lamba_2009Nessuna valutazione finora

- Current Affairs June 2013Documento15 pagineCurrent Affairs June 2013Karthick NaikNessuna valutazione finora

- Jaiib - Paper IDocumento2 pagineJaiib - Paper IkirthikasingaramNessuna valutazione finora

- Current Affairs July 2013 - WWW - BankingawarenessDocumento0 pagineCurrent Affairs July 2013 - WWW - BankingawarenessJaya SudhakarNessuna valutazione finora

- CAIIB Super Notes Advanced Bank Management Module C Human Resource Management Human Implications of Organ Is at IonsDocumento48 pagineCAIIB Super Notes Advanced Bank Management Module C Human Resource Management Human Implications of Organ Is at Ionsvippy_love0% (1)

- WELCOME To Institute of Banking Personnel SelectionDocumento2 pagineWELCOME To Institute of Banking Personnel Selectiongopal_psbNessuna valutazione finora

- 9th IX Bipartite SettlementDocumento57 pagine9th IX Bipartite Settlementgopal_psbNessuna valutazione finora

- Basel 3 Summary TableDocumento1 paginaBasel 3 Summary TableIzian SherwaniNessuna valutazione finora

- Union Budget 2012-13: HighlightsDocumento15 pagineUnion Budget 2012-13: HighlightsNDTVNessuna valutazione finora

- Jaii B Principles Banking Modules Ab QuestionsDocumento10 pagineJaii B Principles Banking Modules Ab Questionsgopal_psbNessuna valutazione finora

- Caiib Gbmmoda Mcqsnov0Documento5 pagineCaiib Gbmmoda Mcqsnov0gopal_psbNessuna valutazione finora

- Monetary and Credit Information Review: Issue 10Documento4 pagineMonetary and Credit Information Review: Issue 10gopal_psbNessuna valutazione finora

- Monetary and Credit Information Review: Issue 10Documento4 pagineMonetary and Credit Information Review: Issue 10gopal_psbNessuna valutazione finora

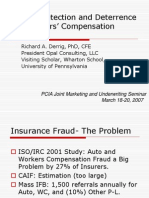

- Fraud Detection and Deterrence in Workers' CompensationDocumento46 pagineFraud Detection and Deterrence in Workers' CompensationTanya ChaudharyNessuna valutazione finora

- SAP Project System - A Ready Reference (Part 1) - SAP BlogsDocumento17 pagineSAP Project System - A Ready Reference (Part 1) - SAP BlogsSUNIL palNessuna valutazione finora

- Cypherpunk's ManifestoDocumento3 pagineCypherpunk's ManifestoevanLeNessuna valutazione finora

- On Rural America - Understanding Isn't The ProblemDocumento8 pagineOn Rural America - Understanding Isn't The ProblemReaperXIXNessuna valutazione finora

- Biography of The Chofetz ChaimDocumento2 pagineBiography of The Chofetz ChaimJavier Romero GonzalezNessuna valutazione finora

- Appendix 1. Helicopter Data: 1. INTRODUCTION. This Appendix Contains 2. VERIFICATION. The Published InformationDocumento20 pagineAppendix 1. Helicopter Data: 1. INTRODUCTION. This Appendix Contains 2. VERIFICATION. The Published Informationsamirsamira928Nessuna valutazione finora

- Online Auction: 377 Brookview Drive, Riverdale, Georgia 30274Documento2 pagineOnline Auction: 377 Brookview Drive, Riverdale, Georgia 30274AnandNessuna valutazione finora

- VergaraDocumento13 pagineVergaraAurora Pelagio VallejosNessuna valutazione finora

- Amalgamation of SocietiesDocumento4 pagineAmalgamation of SocietiesKen ChepkwonyNessuna valutazione finora

- Situational Prevention and The Reduction of White Collar Crime by Dr. Neil R. VanceDocumento22 pagineSituational Prevention and The Reduction of White Collar Crime by Dr. Neil R. VancePedroNessuna valutazione finora

- Tri-City Times: New Manager Ready To Embrace ChallengesDocumento20 pagineTri-City Times: New Manager Ready To Embrace ChallengesWoodsNessuna valutazione finora

- HIRING OF VEHICLEsDocumento2 pagineHIRING OF VEHICLEsthummadharaniNessuna valutazione finora

- K. A. Abbas v. Union of India - A Case StudyDocumento4 pagineK. A. Abbas v. Union of India - A Case StudyAditya pal100% (2)

- Statement by Bob Rae On The Death of Don SmithDocumento1 paginaStatement by Bob Rae On The Death of Don Smithbob_rae_a4Nessuna valutazione finora

- Econ Essay On Royal Mail Between PrivitisationDocumento2 pagineEcon Essay On Royal Mail Between PrivitisationAhila100% (1)

- Model Test 15 - 20Documento206 pagineModel Test 15 - 20theabhishekdahalNessuna valutazione finora

- Article On Female Foeticide-Need To Change The MindsetDocumento4 pagineArticle On Female Foeticide-Need To Change The MindsetigdrNessuna valutazione finora

- Promises During The Elections and InaugurationDocumento3 paginePromises During The Elections and InaugurationJessa QuitolaNessuna valutazione finora

- SaraikistanDocumento31 pagineSaraikistanKhadija MirNessuna valutazione finora