Potrebbero piacerti anche

- Summary Of "Politics And Power In Menem's Government" By Marcos Novaro And Vicente Palermo: UNIVERSITY SUMMARIESDa EverandSummary Of "Politics And Power In Menem's Government" By Marcos Novaro And Vicente Palermo: UNIVERSITY SUMMARIESNessuna valutazione finora

- Reviving LeviathanDocumento36 pagineReviving LeviathanGeorgiana SerbanNessuna valutazione finora

- Free Markets under Siege: Cartels, Politics, and Social WelfareDa EverandFree Markets under Siege: Cartels, Politics, and Social WelfareValutazione: 4 su 5 stelle4/5 (1)

- Taxes, Consultation and Democracy in Export-Led EconomiesDocumento39 pagineTaxes, Consultation and Democracy in Export-Led EconomiesHenrry AllanNessuna valutazione finora

- Cryptosecession and The Limitis of Taxation Towards A Theory of Non Territorial Internal Exit CompressedDocumento36 pagineCryptosecession and The Limitis of Taxation Towards A Theory of Non Territorial Internal Exit CompressedAnonymous d1v0KnjNessuna valutazione finora

- Eshag J E. (2008) Fiscal FederalismDocumento8 pagineEshag J E. (2008) Fiscal FederalismAndré AranhaNessuna valutazione finora

- Pol PresentationDocumento6 paginePol PresentationLipika SinglaNessuna valutazione finora

- 20 007 History and Taxation The Dialectical Relationship Between Taxation Final WebDocumento44 pagine20 007 History and Taxation The Dialectical Relationship Between Taxation Final WebDaisy AnitaNessuna valutazione finora

- Summary w4 r3 Chaudhry, The Myhts of The Market - PDF 1680126135Documento4 pagineSummary w4 r3 Chaudhry, The Myhts of The Market - PDF 1680126135Ceren Gökçe KeskinNessuna valutazione finora

- Demo - Glob-Ignas KledenDocumento15 pagineDemo - Glob-Ignas Kledenlubeck starlight100% (1)

- 1.1 Pierre and Peters Different Ways To Think About GovernanceDocumento7 pagine1.1 Pierre and Peters Different Ways To Think About GovernanceKay GóngoraNessuna valutazione finora

- Eaton 1Documento25 pagineEaton 1AdrianaNessuna valutazione finora

- Models of Federal-Power Sharing Ronald L. WattsDocumento11 pagineModels of Federal-Power Sharing Ronald L. Wattsmsaamir115851Nessuna valutazione finora

- Small Is Beautiful and Efficient: The Case For Secession: Hans-Hermann HoppeDocumento7 pagineSmall Is Beautiful and Efficient: The Case For Secession: Hans-Hermann HoppeArchiloloNessuna valutazione finora

- Local Government - Provision of Public Goods - NigeriaDocumento20 pagineLocal Government - Provision of Public Goods - NigeriaAlice Soares GuimarãesNessuna valutazione finora

- Decentralization and The Post-War Political Economy Francis G. Castles Discussion Paper No. 399 March 1999Documento28 pagineDecentralization and The Post-War Political Economy Francis G. Castles Discussion Paper No. 399 March 1999Franditya UtomoNessuna valutazione finora

- Federalism and DecentralizationDocumento40 pagineFederalism and DecentralizationnailaweoungNessuna valutazione finora

- Fiscal Rules 1Documento21 pagineFiscal Rules 1La SalleNessuna valutazione finora

- 72TaxLRev235 Taxation and DemocracyDocumento71 pagine72TaxLRev235 Taxation and DemocracysakalemNessuna valutazione finora

- Boix PartisanGovernmDocumento37 pagineBoix PartisanGovernmIvo TunjićNessuna valutazione finora

- Why Don't Tax The RichDocumento46 pagineWhy Don't Tax The RichJamodNessuna valutazione finora

- Globalization and Its ImpactDocumento18 pagineGlobalization and Its ImpactSurya Prakash Singh100% (1)

- Zviad Barkaia Public Choice PaperDocumento8 pagineZviad Barkaia Public Choice PaperZviad BarkaiaNessuna valutazione finora

- Budget, Institutions and Fiscal Policy - Tanzi (2014)Documento41 pagineBudget, Institutions and Fiscal Policy - Tanzi (2014)Maria DiazNessuna valutazione finora

- Chapter 3the Origins of Corruption in Transition CountriesDocumento14 pagineChapter 3the Origins of Corruption in Transition CountriesEdwardduskNessuna valutazione finora

- Taxation and Statebuilding The Tax Reform Under The Nationalist Government in ChinaDocumento14 pagineTaxation and Statebuilding The Tax Reform Under The Nationalist Government in ChinaShinobu MoriNessuna valutazione finora

- Corruption Beyond The Post Washington Consensus KhanDocumento22 pagineCorruption Beyond The Post Washington Consensus KhanAditya SanyalNessuna valutazione finora

- (READ) Lect 4 Why Market Capitalism Favors Democracy (Optional Reading)Documento3 pagine(READ) Lect 4 Why Market Capitalism Favors Democracy (Optional Reading)Cheryl LuiNessuna valutazione finora

- BOIX 2000 - Partisan - Governments - The - International - Economy - andDocumento37 pagineBOIX 2000 - Partisan - Governments - The - International - Economy - andbcasartelli1Nessuna valutazione finora

- Excerpt of Introduction To Political Economy, Lecture Notes by Daron Acemoglu (PoliticalDocumento34 pagineExcerpt of Introduction To Political Economy, Lecture Notes by Daron Acemoglu (PoliticalKaren PerezNessuna valutazione finora

- Military Rule & Economic Growth in Post-Independence Uganda: A Synthetic Counterfactual ApproachDocumento53 pagineMilitary Rule & Economic Growth in Post-Independence Uganda: A Synthetic Counterfactual ApproachHannington RkNessuna valutazione finora

- Money, Politics, AndDemocracy 2011Documento20 pagineMoney, Politics, AndDemocracy 2011Daiane Deponti Bolzan100% (1)

- 5-2 Goverment GlobalizationDocumento36 pagine5-2 Goverment GlobalizationEpi SidaNessuna valutazione finora

- (Doi 10.1017/CBO9780511973154.011) Tanzi, Vito - Government Versus Markets (The Changing Economic Role of The State) - Theories of Public-Sector BehaviorDocumento18 pagine(Doi 10.1017/CBO9780511973154.011) Tanzi, Vito - Government Versus Markets (The Changing Economic Role of The State) - Theories of Public-Sector BehaviorJokoWidodoNessuna valutazione finora

- French GovtDocumento6 pagineFrench GovtharleenpeterNessuna valutazione finora

- Focus and Background: The Focus of This EssayDocumento31 pagineFocus and Background: The Focus of This EssayDx RevueltasNessuna valutazione finora

- Public FinanceDocumento61 paginePublic FinancePlatonic100% (9)

- Notes On Senarclens On GovernanceDocumento4 pagineNotes On Senarclens On GovernanceDiana Ni DhuibhirNessuna valutazione finora

- Rethinking RegulationDocumento15 pagineRethinking RegulationRoosevelt InstituteNessuna valutazione finora

- Dahl - On Democracy - Chp. 13 14Documento7 pagineDahl - On Democracy - Chp. 13 14Visar ZekaNessuna valutazione finora

- The Political Economy of Taxation: Positive and Normative Analysis When Collective Choice MattersDocumento31 pagineThe Political Economy of Taxation: Positive and Normative Analysis When Collective Choice MattersJaymeeSolomonNessuna valutazione finora

- Final EVOLUTION OF PHILIPPINE TAXATIONDocumento17 pagineFinal EVOLUTION OF PHILIPPINE TAXATIONaaron danyliukNessuna valutazione finora

- Federalism: I. Meaning and HistoryDocumento33 pagineFederalism: I. Meaning and HistoryNOONEUNKNOWNNessuna valutazione finora

- IPE ExamDocumento3 pagineIPE ExamJM Hernandez VillanuevaNessuna valutazione finora

- Differential Effects of Fiscal Decentralization - Local Revenue Share Vs Local Fiscal AutonomyDocumento51 pagineDifferential Effects of Fiscal Decentralization - Local Revenue Share Vs Local Fiscal AutonomyAxellinaMuaraNessuna valutazione finora

- State Financialization Permanent Austerity Financialized Real Estate and The Politics of Public Assets in ItalyDocumento26 pagineState Financialization Permanent Austerity Financialized Real Estate and The Politics of Public Assets in ItalyIsabela RodriguesNessuna valutazione finora

- Taxation and Democracy - SchonDocumento65 pagineTaxation and Democracy - SchonRoberto RamosNessuna valutazione finora

- Different Ways To Think About GovernanceDocumento9 pagineDifferent Ways To Think About GovernanceKay GóngoraNessuna valutazione finora

- IPE ExamDocumento3 pagineIPE ExamJM Hernandez VillanuevaNessuna valutazione finora

- DescentralizationDocumento36 pagineDescentralizationNina PlopNessuna valutazione finora

- Deconcentration Versus Decentralization of Administration in FranceDocumento16 pagineDeconcentration Versus Decentralization of Administration in FrancenailaweoungNessuna valutazione finora

- Combining Psychology and Economics in TheDocumento19 pagineCombining Psychology and Economics in TheÉrika SordiNessuna valutazione finora

- Commanding Heights (Part 1: The Battle of Ideas) : A Reaction PaperDocumento3 pagineCommanding Heights (Part 1: The Battle of Ideas) : A Reaction PaperasdadhhNessuna valutazione finora

- THE OLD AND THE NEW POLITICS OF TAXATION - Cronin PDFDocumento34 pagineTHE OLD AND THE NEW POLITICS OF TAXATION - Cronin PDFRoberto RamosNessuna valutazione finora

- 10L Global EconomyDocumento16 pagine10L Global Economyhesenzadegulsum66Nessuna valutazione finora

- The Public Sector in An In-Between TimeDocumento20 pagineThe Public Sector in An In-Between TimeMaurino ÉvoraNessuna valutazione finora

- Chudnovsky OxfordDocumento25 pagineChudnovsky OxfordLeonardo FiscanteNessuna valutazione finora

- Polga-Hecimovich 2019 - OREDocumento31 paginePolga-Hecimovich 2019 - ORElaireneNessuna valutazione finora

- Against Law-SterityDocumento19 pagineAgainst Law-SterityrobertjknoxNessuna valutazione finora

- Governing Europe, Book by Jack Hayward, Anand Menon Oxford University Press, 2003Documento14 pagineGoverning Europe, Book by Jack Hayward, Anand Menon Oxford University Press, 2003Amina CristinaNessuna valutazione finora

- Industrial Training RepoDocumento24 pagineIndustrial Training RepoTeh Kim SinNessuna valutazione finora

- The Relationship Between Financial PDFDocumento255 pagineThe Relationship Between Financial PDFTeh Kim SinNessuna valutazione finora

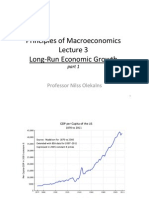

- Principles of Macroeconomics Lecture 3 Long - Run Economic GrowthDocumento4 paginePrinciples of Macroeconomics Lecture 3 Long - Run Economic GrowthTeh Kim SinNessuna valutazione finora

- Yap Lecture 2 PDF PDFDocumento18 pagineYap Lecture 2 PDF PDFTeh Kim SinNessuna valutazione finora

- Lecture Slides-Lecture 2 Part 3Documento5 pagineLecture Slides-Lecture 2 Part 3Asim RafiqNessuna valutazione finora

- Datastream Installation Guide PDFDocumento4 pagineDatastream Installation Guide PDFTeh Kim SinNessuna valutazione finora

- Principles of Macroeconomics Lecture 3 Long - Run Economic GrowthDocumento10 paginePrinciples of Macroeconomics Lecture 3 Long - Run Economic GrowthTeh Kim SinNessuna valutazione finora

- Principles of Macroeconomics Lecture 3 Long - Run Economic GrowthDocumento2 paginePrinciples of Macroeconomics Lecture 3 Long - Run Economic GrowthTeh Kim SinNessuna valutazione finora

- Lecture Slides-Lecture 2 Part 3Documento5 pagineLecture Slides-Lecture 2 Part 3Asim RafiqNessuna valutazione finora

- Lecture Slides Lecture 2 Part 1Documento4 pagineLecture Slides Lecture 2 Part 1Teh Kim SinNessuna valutazione finora

- Lecture Slides-Lecture 2 Part 3Documento5 pagineLecture Slides-Lecture 2 Part 3Asim RafiqNessuna valutazione finora

- Lecture Slides Lecture 2 Part 2Documento7 pagineLecture Slides Lecture 2 Part 2Teh Kim SinNessuna valutazione finora

- Grabbing Hand and Market Preserving FederalismDocumento1 paginaGrabbing Hand and Market Preserving FederalismTeh Kim SinNessuna valutazione finora

- Lecture Slides Lecture 1 Part 1Documento5 pagineLecture Slides Lecture 1 Part 1Teh Kim SinNessuna valutazione finora

- 15.1 A) The Monthly Growth Rate in IP Expressed in Percentage Points, Ip - Growth 100 Log (Ip/ip (-1) )Documento4 pagine15.1 A) The Monthly Growth Rate in IP Expressed in Percentage Points, Ip - Growth 100 Log (Ip/ip (-1) )Teh Kim SinNessuna valutazione finora

- Compunere Imagine A World Where Nobody Gets Sick or Old. Write A Story Based in This Fictitious WorldDocumento2 pagineCompunere Imagine A World Where Nobody Gets Sick or Old. Write A Story Based in This Fictitious WorldOverload4UNessuna valutazione finora

- Compunere Imagine A World Where Nobody Gets Sick or Old. Write A Story Based in This Fictitious WorldDocumento2 pagineCompunere Imagine A World Where Nobody Gets Sick or Old. Write A Story Based in This Fictitious WorldOverload4UNessuna valutazione finora

- New Presentation1Documento6 pagineNew Presentation1Teh Kim SinNessuna valutazione finora

- HTTP 1Documento1 paginaHTTP 1Teh Kim SinNessuna valutazione finora

- Public SectorDocumento13 paginePublic SectorPradnya SurwadeNessuna valutazione finora

- Cross Cultural Understanding 07 Cultural ConflictDocumento13 pagineCross Cultural Understanding 07 Cultural Conflictestu kaniraNessuna valutazione finora

- Moving Forward - UNHCR Malta MagazineDocumento72 pagineMoving Forward - UNHCR Malta MagazineUNHCR Malta100% (1)

- Womens Month MemoDocumento2 pagineWomens Month MemoLed Buen100% (2)

- Family Law 3Documento34 pagineFamily Law 3PIYUSH SHARMANessuna valutazione finora

- BLDocumento11 pagineBLOm Singh IndaNessuna valutazione finora

- Adams, Ilocos NorteDocumento3 pagineAdams, Ilocos NorteClaire GargaritaNessuna valutazione finora

- Pa 202 HandoutDocumento4 paginePa 202 Handoutmeldgyrie mae andalesNessuna valutazione finora

- Case Analysis Constitution Vijay Kumar Sharma V ST of Karnataka PDFDocumento14 pagineCase Analysis Constitution Vijay Kumar Sharma V ST of Karnataka PDFNaman DadhichNessuna valutazione finora

- 4-Parens Patriae - Alfred AdaskDocumento8 pagine4-Parens Patriae - Alfred AdaskOneNationNessuna valutazione finora

- Bsb1 2 SchofieldDocumento12 pagineBsb1 2 SchofieldMichal StiborNessuna valutazione finora

- Rape Victim Speaks OutDocumento3 pagineRape Victim Speaks OutlawrenceNessuna valutazione finora

- Globalization 1Documento6 pagineGlobalization 1JohnNessuna valutazione finora

- Sir John Jeremie - Experiences of Slave Society in St. Lucia !Documento121 pagineSir John Jeremie - Experiences of Slave Society in St. Lucia !cookiesluNessuna valutazione finora

- In Another Instance of Conscience Stirring CasesDocumento6 pagineIn Another Instance of Conscience Stirring CasesSNEHA SOLANKINessuna valutazione finora

- 1857 Revolt-Nature and CausesDocumento5 pagine1857 Revolt-Nature and CausesPadma LhamoNessuna valutazione finora

- Mr. Teodoro Sabuga-A, CSWD HeadDocumento4 pagineMr. Teodoro Sabuga-A, CSWD HeadJamil B. AsumNessuna valutazione finora

- Fee Structure 2023 24Documento1 paginaFee Structure 2023 24JavedNessuna valutazione finora

- IR Lecture 21 Maternity Benefit ActDocumento13 pagineIR Lecture 21 Maternity Benefit ActradhikaNessuna valutazione finora

- 2020 05 26 IDN NV UN 001 EnglishDocumento2 pagine2020 05 26 IDN NV UN 001 EnglishRappler100% (2)

- Taxation ReviewerDocumento4 pagineTaxation ReviewerAesha Tamar PastranaNessuna valutazione finora

- English Application FormDocumento4 pagineEnglish Application FormFathu HasuNessuna valutazione finora

- Proposed Suspension OrderDocumento9 pagineProposed Suspension OrderGeronimo rigor Capariño100% (1)

- The Philippine Commonwealth PeriodDocumento18 pagineThe Philippine Commonwealth PeriodZanjo Seco0% (1)

- Province of Batangas v. RomuloDocumento4 pagineProvince of Batangas v. RomuloNoreenesse Santos100% (1)

- Brown County General OrdersDocumento124 pagineBrown County General OrdersreagandrNessuna valutazione finora

- Ingles 10 Doris - JudithDocumento10 pagineIngles 10 Doris - JudithLuz Mercedes Rugeles GelvezNessuna valutazione finora

- Period 2 Study Guide (APUSH)Documento2 paginePeriod 2 Study Guide (APUSH)trankNessuna valutazione finora

- Eo Badac Reorganization 2018Documento2 pagineEo Badac Reorganization 2018Rolando Lagat50% (2)

- Fiqh Al-Aqalliyat A Legal Theory For Muslim MinoritiesDocumento24 pagineFiqh Al-Aqalliyat A Legal Theory For Muslim MinoritiesMuhammad Fariz Mohamed Zain100% (1)

- Articles of Partnership - BLANKDocumento3 pagineArticles of Partnership - BLANKRafaelNessuna valutazione finora

- Thomas Jefferson: Author of AmericaDa EverandThomas Jefferson: Author of AmericaValutazione: 4 su 5 stelle4/5 (107)

- The Courage to Be Free: Florida's Blueprint for America's RevivalDa EverandThe Courage to Be Free: Florida's Blueprint for America's RevivalNessuna valutazione finora

- Nine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesDa EverandNine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesNessuna valutazione finora

- Stonewalled: My Fight for Truth Against the Forces of Obstruction, Intimidation, and Harassment in Obama's WashingtonDa EverandStonewalled: My Fight for Truth Against the Forces of Obstruction, Intimidation, and Harassment in Obama's WashingtonValutazione: 4.5 su 5 stelle4.5/5 (21)

- Modern Warriors: Real Stories from Real HeroesDa EverandModern Warriors: Real Stories from Real HeroesValutazione: 3.5 su 5 stelle3.5/5 (3)

- The Russia Hoax: The Illicit Scheme to Clear Hillary Clinton and Frame Donald TrumpDa EverandThe Russia Hoax: The Illicit Scheme to Clear Hillary Clinton and Frame Donald TrumpValutazione: 4.5 su 5 stelle4.5/5 (11)

- The Smear: How Shady Political Operatives and Fake News Control What You See, What You Think, and How You VoteDa EverandThe Smear: How Shady Political Operatives and Fake News Control What You See, What You Think, and How You VoteValutazione: 4.5 su 5 stelle4.5/5 (16)

- The Great Gasbag: An A–Z Study Guide to Surviving Trump WorldDa EverandThe Great Gasbag: An A–Z Study Guide to Surviving Trump WorldValutazione: 3.5 su 5 stelle3.5/5 (9)

- The Red and the Blue: The 1990s and the Birth of Political TribalismDa EverandThe Red and the Blue: The 1990s and the Birth of Political TribalismValutazione: 4 su 5 stelle4/5 (29)

- The Shadow War: Inside Russia's and China's Secret Operations to Defeat AmericaDa EverandThe Shadow War: Inside Russia's and China's Secret Operations to Defeat AmericaValutazione: 4.5 su 5 stelle4.5/5 (12)

- The FBI Way: Inside the Bureau's Code of ExcellenceDa EverandThe FBI Way: Inside the Bureau's Code of ExcellenceNessuna valutazione finora

- The Quiet Man: The Indispensable Presidency of George H.W. BushDa EverandThe Quiet Man: The Indispensable Presidency of George H.W. BushValutazione: 4 su 5 stelle4/5 (1)

- Power Grab: The Liberal Scheme to Undermine Trump, the GOP, and Our RepublicDa EverandPower Grab: The Liberal Scheme to Undermine Trump, the GOP, and Our RepublicNessuna valutazione finora

- We've Got Issues: How You Can Stand Strong for America's Soul and SanityDa EverandWe've Got Issues: How You Can Stand Strong for America's Soul and SanityNessuna valutazione finora

- Game Change: Obama and the Clintons, McCain and Palin, and the Race of a LifetimeDa EverandGame Change: Obama and the Clintons, McCain and Palin, and the Race of a LifetimeValutazione: 4 su 5 stelle4/5 (572)

- Commander In Chief: FDR's Battle with Churchill, 1943Da EverandCommander In Chief: FDR's Battle with Churchill, 1943Valutazione: 4 su 5 stelle4/5 (16)

- Confidence Men: Wall Street, Washington, and the Education of a PresidentDa EverandConfidence Men: Wall Street, Washington, and the Education of a PresidentValutazione: 3.5 su 5 stelle3.5/5 (52)

- The Next Civil War: Dispatches from the American FutureDa EverandThe Next Civil War: Dispatches from the American FutureValutazione: 3.5 su 5 stelle3.5/5 (47)

- The Deep State: How an Army of Bureaucrats Protected Barack Obama and Is Working to Destroy the Trump AgendaDa EverandThe Deep State: How an Army of Bureaucrats Protected Barack Obama and Is Working to Destroy the Trump AgendaValutazione: 4.5 su 5 stelle4.5/5 (4)

- Crimes and Cover-ups in American Politics: 1776-1963Da EverandCrimes and Cover-ups in American Politics: 1776-1963Valutazione: 4.5 su 5 stelle4.5/5 (26)

- Socialism 101: From the Bolsheviks and Karl Marx to Universal Healthcare and the Democratic Socialists, Everything You Need to Know about SocialismDa EverandSocialism 101: From the Bolsheviks and Karl Marx to Universal Healthcare and the Democratic Socialists, Everything You Need to Know about SocialismValutazione: 4.5 su 5 stelle4.5/5 (42)

- Reading the Constitution: Why I Chose Pragmatism, not TextualismDa EverandReading the Constitution: Why I Chose Pragmatism, not TextualismNessuna valutazione finora

- Camelot's Court: Inside the Kennedy White HouseDa EverandCamelot's Court: Inside the Kennedy White HouseValutazione: 4 su 5 stelle4/5 (17)

- Hatemonger: Stephen Miller, Donald Trump, and the White Nationalist AgendaDa EverandHatemonger: Stephen Miller, Donald Trump, and the White Nationalist AgendaValutazione: 4 su 5 stelle4/5 (5)

- Witch Hunt: The Story of the Greatest Mass Delusion in American Political HistoryDa EverandWitch Hunt: The Story of the Greatest Mass Delusion in American Political HistoryValutazione: 4 su 5 stelle4/5 (6)

- The Magnificent Medills: The McCormick-Patterson Dynasty: America's Royal Family of Journalism During a Century of Turbulent SplendorDa EverandThe Magnificent Medills: The McCormick-Patterson Dynasty: America's Royal Family of Journalism During a Century of Turbulent SplendorNessuna valutazione finora

- An Ordinary Man: The Surprising Life and Historic Presidency of Gerald R. FordDa EverandAn Ordinary Man: The Surprising Life and Historic Presidency of Gerald R. FordValutazione: 4 su 5 stelle4/5 (5)

- The Last Republicans: Inside the Extraordinary Relationship Between George H.W. Bush and George W. BushDa EverandThe Last Republicans: Inside the Extraordinary Relationship Between George H.W. Bush and George W. BushValutazione: 4 su 5 stelle4/5 (6)

- 1960: LBJ vs. JFK vs. Nixon--The Epic Campaign That Forged Three PresidenciesDa Everand1960: LBJ vs. JFK vs. Nixon--The Epic Campaign That Forged Three PresidenciesValutazione: 4.5 su 5 stelle4.5/5 (50)