Potrebbero piacerti anche

- Asset: Formal DefinitionDocumento5 pagineAsset: Formal DefinitionAngelo AristizabalNessuna valutazione finora

- Pink GurlzDocumento423 paginePink Gurlzmygurlz1991Nessuna valutazione finora

- Accounting equation basicsDocumento61 pagineAccounting equation basicsSwapna Zacharia CheripurathuNessuna valutazione finora

- Assets - Meaning and ClassificationDocumento6 pagineAssets - Meaning and ClassificationJann Vic SalesNessuna valutazione finora

- In Business and AccountingDocumento6 pagineIn Business and AccountingHarish AroraNessuna valutazione finora

- Accounting: Main ArticleDocumento2 pagineAccounting: Main ArticleAnn StylesNessuna valutazione finora

- Asset & Its ClassificationDocumento5 pagineAsset & Its ClassificationSyed Shaker AhmedNessuna valutazione finora

- Unit 5 Audit of Fixed AssetsDocumento10 pagineUnit 5 Audit of Fixed Assetssolomon adamuNessuna valutazione finora

- Peter Goa - English Exercise Unit 4Documento14 paginePeter Goa - English Exercise Unit 4Ronaldo Stevent SitohangNessuna valutazione finora

- Assets, liabilities and the balance sheet explainedDocumento13 pagineAssets, liabilities and the balance sheet explainedMARIA-MIRUNA IVĂNESCUNessuna valutazione finora

- Balance Sheet ExplainedDocumento1 paginaBalance Sheet ExplainedТеа ДимитроваNessuna valutazione finora

- What Is Cash FlowDocumento31 pagineWhat Is Cash FlowSumaira BilalNessuna valutazione finora

- Current Assets and Non-Current Assets: Monday GroupDocumento11 pagineCurrent Assets and Non-Current Assets: Monday GroupGJ BadenasNessuna valutazione finora

- BACNTHIDocumento3 pagineBACNTHIFaith CalingoNessuna valutazione finora

- Actg1 - Chapter 3Documento37 pagineActg1 - Chapter 3Reynaleen Agta100% (1)

- Introduction To Balance Sheet: Assets Liabilities Owner's (Stockholders') EquityDocumento7 pagineIntroduction To Balance Sheet: Assets Liabilities Owner's (Stockholders') EquityChanti KumarNessuna valutazione finora

- How Businesses Measure Liquidity and SolvencyDocumento3 pagineHow Businesses Measure Liquidity and SolvencyKristelleMary LabradorNessuna valutazione finora

- Note-Fabm2 Day 1Documento4 pagineNote-Fabm2 Day 1MAYRA APURANessuna valutazione finora

- The Accounting EquationDocumento5 pagineThe Accounting EquationHuskyNessuna valutazione finora

- Lesson 1: Statement of Financial Position: I. AssetsDocumento1 paginaLesson 1: Statement of Financial Position: I. AssetsKristineNessuna valutazione finora

- Fixed Asset: Fixed Assets, Also Known As A Non-Current Asset or As Property, Plant, and Equipment (PP&E), Is ADocumento7 pagineFixed Asset: Fixed Assets, Also Known As A Non-Current Asset or As Property, Plant, and Equipment (PP&E), Is ARandal SchroederNessuna valutazione finora

- Bhargava FAMDocumento57 pagineBhargava FAMY. BhargavaNessuna valutazione finora

- CH 3 - Capital Employed and Invested CapitalDocumento9 pagineCH 3 - Capital Employed and Invested Capital李承翰Nessuna valutazione finora

- For Example, Wearing Apparel, Furniture, Car or Scooter, TV, Refrigerator, MusicalDocumento3 pagineFor Example, Wearing Apparel, Furniture, Car or Scooter, TV, Refrigerator, MusicalJoshua GibsonNessuna valutazione finora

- AssetsDocumento4 pagineAssetsCLLN FILESNessuna valutazione finora

- Bunwin Residence: Is The Company Profitable??Documento6 pagineBunwin Residence: Is The Company Profitable??Pum MineaNessuna valutazione finora

- Acconting NotesDocumento27 pagineAcconting NotesparinkhonaNessuna valutazione finora

- Important HighlightsDocumento2 pagineImportant HighlightsSyed Zeeshan ArshadNessuna valutazione finora

- Fundamentals of Accountancy, Business and Management (FDNACCTDocumento33 pagineFundamentals of Accountancy, Business and Management (FDNACCTChyle SamuelNessuna valutazione finora

- Accounting of Fixed AssetsDocumento6 pagineAccounting of Fixed Assetsnallarahul86Nessuna valutazione finora

- Types of AssetsDocumento2 pagineTypes of AssetsJustine Airra OndoyNessuna valutazione finora

- TOPIC 2 Elements of Accounting and Accounting EquationDocumento6 pagineTOPIC 2 Elements of Accounting and Accounting EquationAnastasia MelnicovaNessuna valutazione finora

- CH 2 and Ch. 3 Basic Theory and Final AccountsDocumento53 pagineCH 2 and Ch. 3 Basic Theory and Final AccountssagarnarayanmundadaNessuna valutazione finora

- Key Points For Week 3 TopicDocumento4 pagineKey Points For Week 3 TopicKyaw Thwe TunNessuna valutazione finora

- Elements of Financial Statements & The Recognition Criteria For Assets & LiabilitiesDocumento13 pagineElements of Financial Statements & The Recognition Criteria For Assets & LiabilitiesdeepshrmNessuna valutazione finora

- Adjusting EntriesDocumento26 pagineAdjusting EntriesSamuel GlovaNessuna valutazione finora

- What is an AssetDocumento2 pagineWhat is an AssetDarlene SarcinoNessuna valutazione finora

- English Active PasiveDocumento15 pagineEnglish Active PasiveAna DanaNessuna valutazione finora

- Distinguish Between Capital Expenditure and Revenue ExpenditureDocumento11 pagineDistinguish Between Capital Expenditure and Revenue ExpenditureGopika GopalakrishnanNessuna valutazione finora

- Accounting for Non-Current AssetsDocumento16 pagineAccounting for Non-Current AssetsSameer GoyalNessuna valutazione finora

- Fixed AssetsDocumento46 pagineFixed AssetsSprancenatu Lavinia0% (1)

- 1. Current Asset2. Current Asset 3. Noncurrent Asset4. Current Asset5. Noncurrent Asset6. Current AssetDocumento19 pagine1. Current Asset2. Current Asset 3. Noncurrent Asset4. Current Asset5. Noncurrent Asset6. Current AssetMylene SalvadorNessuna valutazione finora

- Balance Sheet SummaryDocumento9 pagineBalance Sheet SummaryRahul GuptaNessuna valutazione finora

- Corporate Finance Assignment - 1Documento14 pagineCorporate Finance Assignment - 1nsmkarthickNessuna valutazione finora

- Chapter 2: Accounting Equation and The Double-Entry SystemDocumento15 pagineChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae SasutilNessuna valutazione finora

- Chapter 2: Accounting Equation and The Double-Entry SystemDocumento15 pagineChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae Sasutil100% (1)

- Accounting terms and definitions under 40 charactersDocumento5 pagineAccounting terms and definitions under 40 charactersMa Glenda Brequillo SañgaNessuna valutazione finora

- Current and Noncurrent AssetsDocumento19 pagineCurrent and Noncurrent AssetsMylene SalvadorNessuna valutazione finora

- 04 FA Chapter FourDocumento23 pagine04 FA Chapter FourHistory and EventNessuna valutazione finora

- Fixed Asset Vs Current AssetDocumento3 pagineFixed Asset Vs Current AssetSheila Mae LiraNessuna valutazione finora

- The Accounting EquationDocumento4 pagineThe Accounting EquationjcwimzNessuna valutazione finora

- Assignment 3 (Group 1 Bascug, Basilio, Espineda)Documento2 pagineAssignment 3 (Group 1 Bascug, Basilio, Espineda)jbbascugNessuna valutazione finora

- Financial Management DictionaryDocumento9 pagineFinancial Management DictionaryRaf QuiazonNessuna valutazione finora

- Accounting For Managers. 1pdfDocumento168 pagineAccounting For Managers. 1pdfAkash TiwariNessuna valutazione finora

- Limitations of The Balance SheetDocumento14 pagineLimitations of The Balance SheetFantayNessuna valutazione finora

- A Balance SheetDocumento3 pagineA Balance SheetKarthik ThotaNessuna valutazione finora

- Understanding Financial Statements (Review and Analysis of Straub's Book)Da EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Valutazione: 5 su 5 stelle5/5 (5)

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Da Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Nessuna valutazione finora

- CPA Financial Accounting and Reporting: Second EditionDa EverandCPA Financial Accounting and Reporting: Second EditionNessuna valutazione finora

- Admin Assistant Skills and Tips On Handling Admin Assistant DutiesDocumento3 pagineAdmin Assistant Skills and Tips On Handling Admin Assistant DutiesPhillip DominguezNessuna valutazione finora

- Speed Reading: From Wikipedia, The Free EncyclopediaDocumento5 pagineSpeed Reading: From Wikipedia, The Free EncyclopediaPhillip DominguezNessuna valutazione finora

- PEST AnalysisDocumento4 paginePEST AnalysisPhillip DominguezNessuna valutazione finora

- Organizational System in The Global EnvironmentDocumento17 pagineOrganizational System in The Global EnvironmentPhillip DominguezNessuna valutazione finora

- Organization DevelopmentDocumento12 pagineOrganization DevelopmentPhillip DominguezNessuna valutazione finora

- Standard Operating ProcedureDocumento1 paginaStandard Operating ProcedurerwrtyNessuna valutazione finora

- Employee Satisfactory and Assessment Form For Printing PressDocumento2 pagineEmployee Satisfactory and Assessment Form For Printing PressPhillip DominguezNessuna valutazione finora

- International BusinessDocumento8 pagineInternational BusinessPhillip DominguezNessuna valutazione finora

- Pygmalion EffectDocumento2 paginePygmalion EffectPhillip DominguezNessuna valutazione finora

- Conceptual Model For Organizational BehaviourDocumento19 pagineConceptual Model For Organizational BehaviourPhillip Dominguez100% (1)

- Industerial RelationsDocumento34 pagineIndusterial RelationsPhillip DominguezNessuna valutazione finora

- CH 04Documento44 pagineCH 04ashrafgo100% (1)

- Introduction To Organizational BehaviourDocumento18 pagineIntroduction To Organizational BehaviourPhillip DominguezNessuna valutazione finora

- Personal DevelopmentDocumento13 paginePersonal DevelopmentPhillip DominguezNessuna valutazione finora

- MicroeconomicsDocumento21 pagineMicroeconomicsPhillip DominguezNessuna valutazione finora

- Performance ManagementDocumento4 paginePerformance ManagementPhillip DominguezNessuna valutazione finora

- Reward Management and SystemDocumento55 pagineReward Management and SystemPhillip Dominguez100% (1)

- HR's Strategic Role in Business SuccessDocumento35 pagineHR's Strategic Role in Business SuccessPhillip DominguezNessuna valutazione finora

- A Short History of Performance Management V1Documento46 pagineA Short History of Performance Management V1Phillip Dominguez100% (2)

- More Literature Review On Job SatisfactionDocumento27 pagineMore Literature Review On Job SatisfactionPhillip DominguezNessuna valutazione finora

- More Literature Review On Job SatisfactionDocumento27 pagineMore Literature Review On Job SatisfactionPhillip DominguezNessuna valutazione finora

- Reward Management and SystemDocumento55 pagineReward Management and SystemPhillip Dominguez100% (1)

- Control ManagementDocumento11 pagineControl ManagementPhillip DominguezNessuna valutazione finora

- Job Satisfaction SIP Report UploadedDocumento51 pagineJob Satisfaction SIP Report UploadedPhillip DominguezNessuna valutazione finora

- MNCsDocumento2 pagineMNCsPhillip DominguezNessuna valutazione finora

- Financial AssetDocumento2 pagineFinancial AssetPhillip DominguezNessuna valutazione finora

- Human ResourcesDocumento2 pagineHuman ResourcesPhillip DominguezNessuna valutazione finora

- Test AssessmentDocumento12 pagineTest AssessmentPhillip DominguezNessuna valutazione finora

- What Is International Human Resource ManagementDocumento2 pagineWhat Is International Human Resource ManagementPhillip DominguezNessuna valutazione finora

- Leasehold CovenantsDocumento10 pagineLeasehold CovenantsLecture WizzNessuna valutazione finora

- Psychiatry, Psychology and LawDocumento28 paginePsychiatry, Psychology and LawDaimon MichikoNessuna valutazione finora

- DMC College Accounting Lessons, Tests, Grades 2016-2017Documento3 pagineDMC College Accounting Lessons, Tests, Grades 2016-2017HURLY BALANCARNessuna valutazione finora

- Part CDocumento2 paginePart CNorainun AzwaNessuna valutazione finora

- Mackenzie Herron Criminal ComplaintDocumento2 pagineMackenzie Herron Criminal ComplaintannaNessuna valutazione finora

- HILLARY's Roommate LoverDocumento3 pagineHILLARY's Roommate LoverBarrySoetoroNessuna valutazione finora

- Lifecard Manual WebDocumento24 pagineLifecard Manual WebRafa Gomes0% (1)

- Strategy and Grand Strategy: What Students and Practitioners Need To KnowDocumento97 pagineStrategy and Grand Strategy: What Students and Practitioners Need To KnowSSI-Strategic Studies Institute-US Army War College100% (1)

- Performance MeasuresDocumento14 paginePerformance MeasuresSOUMYAJIT BOSENessuna valutazione finora

- Court Decision in FTC v. MicrosoftDocumento53 pagineCourt Decision in FTC v. MicrosoftEthan GachNessuna valutazione finora

- Factors Influencing Gr.11 & Gr.12 Perspectives on ROTCDocumento12 pagineFactors Influencing Gr.11 & Gr.12 Perspectives on ROTCLa PeñarandaNessuna valutazione finora

- Installation of Mobile Towers in Residential Areas Case StudyDocumento3 pagineInstallation of Mobile Towers in Residential Areas Case StudyDinesh Patra100% (1)

- SOP User Guide - Check Customer IDDocumento30 pagineSOP User Guide - Check Customer IDDella GbedemahNessuna valutazione finora

- How to Trade Stock at Bursa Malaysia: A Step-by-Step Guide for BeginnersDocumento1 paginaHow to Trade Stock at Bursa Malaysia: A Step-by-Step Guide for BeginnersAiman ArshadNessuna valutazione finora

- ESPI vs ENAJE: Supreme Court rules on union security clause, legality of strikeDocumento13 pagineESPI vs ENAJE: Supreme Court rules on union security clause, legality of strikeCaryl BaylonNessuna valutazione finora

- Succession TranscriptDocumento58 pagineSuccession TranscriptLor BellezaNessuna valutazione finora

- Understanding the National Service Training ProgramDocumento7 pagineUnderstanding the National Service Training ProgramAether SkywardNessuna valutazione finora

- RCC71 Stair Flight & Landing - SingleDocumento4 pagineRCC71 Stair Flight & Landing - SingleKourosh KhalpariNessuna valutazione finora

- Australian Trusts PDFDocumento59 pagineAustralian Trusts PDFsamu2-4uNessuna valutazione finora

- TABANGDocumento81 pagineTABANGGuilbert CimeneNessuna valutazione finora

- The Honor-Dishonor ProcessDocumento126 pagineThe Honor-Dishonor ProcessJason Henry100% (7)

- Lesson 2.1: Online Safety, Security and NetiquetteDocumento6 pagineLesson 2.1: Online Safety, Security and NetiquetteChanie Baguio PitogoNessuna valutazione finora

- List+of+Acceptable+I 9+Documents.V2Documento1 paginaList+of+Acceptable+I 9+Documents.V2Maryorie RodriguezNessuna valutazione finora

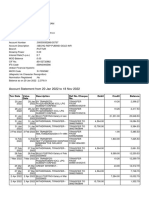

- Bank StatementDocumento4 pagineBank Statementvenkatarammana99Nessuna valutazione finora

- P2P flow with new ProductDocumento166 pagineP2P flow with new ProductRohit DaswaniNessuna valutazione finora

- (Day 58) (Final) The Delivery of Books and Newspapers (Public Libraries) Act, 1954Documento3 pagine(Day 58) (Final) The Delivery of Books and Newspapers (Public Libraries) Act, 1954Deb DasNessuna valutazione finora

- Indian Muslim Women by Razia PatelDocumento6 pagineIndian Muslim Women by Razia PatelAnkit YadavNessuna valutazione finora

- Evi2 Ing9 LDDocumento3 pagineEvi2 Ing9 LDCristian MolinaNessuna valutazione finora

- PCT04 - The Pure Contract Trust in A NutshellDocumento11 paginePCT04 - The Pure Contract Trust in A Nutshell2Plus90% (10)

- Ship Draught and Cargo Transport TermsDocumento5 pagineShip Draught and Cargo Transport TermsHải ChâuNessuna valutazione finora