Potrebbero piacerti anche

- Guide-to-Venture-Capital IVA PDFDocumento90 pagineGuide-to-Venture-Capital IVA PDFNaveen AwasthiNessuna valutazione finora

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveDa EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNessuna valutazione finora

- A Study On Private Equity in IndiaDocumento21 pagineA Study On Private Equity in IndiaPrabakar NatrajNessuna valutazione finora

- Indian Unicorns With Chinese InvestorsDocumento1 paginaIndian Unicorns With Chinese InvestorsThe WireNessuna valutazione finora

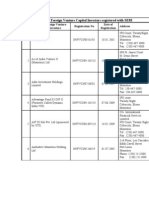

- A-List of Foreign Venture Capital Investors Registered With SEBIDocumento24 pagineA-List of Foreign Venture Capital Investors Registered With SEBIVipul ParekhNessuna valutazione finora

- Pitchbook Private Equity Breakdown 4Q 2009Documento6 paginePitchbook Private Equity Breakdown 4Q 2009Zerohedge100% (1)

- Venture CapitalDocumento30 pagineVenture Capitalmeenakshi383Nessuna valutazione finora

- An Explorative Event Study of Listed Private Equity VehiclesDocumento105 pagineAn Explorative Event Study of Listed Private Equity VehiclesSiddh MehtaNessuna valutazione finora

- Private Equity Secondaries China - PEI Magazine WhitepaperDocumento2 paginePrivate Equity Secondaries China - PEI Magazine WhitepaperpfuhrmanNessuna valutazione finora

- Top 300 PEIDocumento8 pagineTop 300 PEIJerome OngNessuna valutazione finora

- SV Angel - RC Current Investments As of 11/22/2011Documento24 pagineSV Angel - RC Current Investments As of 11/22/2011FortuneNessuna valutazione finora

- Venture Capital Q2 2016Documento1 paginaVenture Capital Q2 2016BayAreaNewsGroup100% (2)

- KKR Annual Review 2008Documento77 pagineKKR Annual Review 2008AsiaBuyoutsNessuna valutazione finora

- CB Insights Game Changers 2018Documento70 pagineCB Insights Game Changers 2018DiannaNessuna valutazione finora

- Q2 Fundraising 2009Documento4 pagineQ2 Fundraising 2009Dan Primack100% (1)

- Pere 50Documento15 paginePere 50Ravin JagooNessuna valutazione finora

- 2Q 15 Vcsurvey PDFDocumento11 pagine2Q 15 Vcsurvey PDFBayAreaNewsGroupNessuna valutazione finora

- Zodius Capital II Fund Launch 070414Documento2 pagineZodius Capital II Fund Launch 070414avendusNessuna valutazione finora

- Mudit Saxena - Genpact SeedDocumento2 pagineMudit Saxena - Genpact SeedParas SatijaNessuna valutazione finora

- FAB Analyst and Investor Day BiosDocumento17 pagineFAB Analyst and Investor Day BioskhuramrajpootNessuna valutazione finora

- Healthtech Venture CapitalDocumento28 pagineHealthtech Venture CapitalFelipe Hernan Herrera SalinasNessuna valutazione finora

- Infrastructure Investor - Brazil Intelligence ReportDocumento40 pagineInfrastructure Investor - Brazil Intelligence ReportjleungcmNessuna valutazione finora

- Venture ListsDocumento8 pagineVenture ListsRavi Singh BishtNessuna valutazione finora

- Private Equity Apax Partners 2007 Annual ReportDocumento78 paginePrivate Equity Apax Partners 2007 Annual ReportAsiaBuyouts100% (3)

- Ecommerce & Marketplace VC Panels & Pitches HandoutDocumento6 pagineEcommerce & Marketplace VC Panels & Pitches HandoutAndrew BottNessuna valutazione finora

- Dokumen - Tips - Middle East Venture Capital Private Equity DirectoryDocumento15 pagineDokumen - Tips - Middle East Venture Capital Private Equity DirectorySadeq ObaidNessuna valutazione finora

- 1Q 14 VCchart PDFDocumento25 pagine1Q 14 VCchart PDFBayAreaNewsGroupNessuna valutazione finora

- CB Insights Global Unicorn Club 2019Documento20 pagineCB Insights Global Unicorn Club 2019Yash Joglekar0% (1)

- 1Q 2018 Investor LetterDocumento18 pagine1Q 2018 Investor LetterczcarNessuna valutazione finora

- Underwriting Placements and The Art of Investor Relations Presentation by Sherilyn Foong Alliance Investment Bank Berhad MalaysiaDocumento25 pagineUnderwriting Placements and The Art of Investor Relations Presentation by Sherilyn Foong Alliance Investment Bank Berhad MalaysiaPramod GosaviNessuna valutazione finora

- Financial MGMT Assignment 2 - Private EquityDocumento32 pagineFinancial MGMT Assignment 2 - Private EquityStefanie Bayer100% (1)

- MeetFounders UK EU August 2021 HandoutDocumento13 pagineMeetFounders UK EU August 2021 HandoutAndrew BottNessuna valutazione finora

- Private Equity in Turkey - SantaDocumento36 paginePrivate Equity in Turkey - SantaOzan CigizogluNessuna valutazione finora

- List of VCFsDocumento3 pagineList of VCFspoddar_ruchitaNessuna valutazione finora

- 2010 0701 AIG Goldman Supporting DocsDocumento518 pagine2010 0701 AIG Goldman Supporting Docsenglishbob618Nessuna valutazione finora

- Venture Capital Funding, Fourth Quarter 2015Documento10 pagineVenture Capital Funding, Fourth Quarter 2015BayAreaNewsGroupNessuna valutazione finora

- 47 Most Active Venture Capital Firms in India For StartupsDocumento21 pagine47 Most Active Venture Capital Firms in India For StartupsfinvistaNessuna valutazione finora

- Submarine Workforce PDFDocumento160 pagineSubmarine Workforce PDFfaithnicNessuna valutazione finora

- Fintech VC Panels & Pitches HandoutDocumento7 pagineFintech VC Panels & Pitches HandoutAndrew BottNessuna valutazione finora

- PE/VC Firms With Women, Minority FoundersDocumento14 paginePE/VC Firms With Women, Minority FoundersdavidtollNessuna valutazione finora

- Venture CapitalDocumento42 pagineVenture CapitalKrinal ShahNessuna valutazione finora

- Pei 135 - Pei300Documento13 paginePei 135 - Pei300Anonymous Rwa38rT8GVNessuna valutazione finora

- BOLD Investor PresentationDocumento110 pagineBOLD Investor PresentationSerge Olivier Atchu YudomNessuna valutazione finora

- Sbic FundsDocumento3 pagineSbic FundsafkdsjfdlsjNessuna valutazione finora

- Tata Elxsi Limited Fundamental Company Report Including Financial, SWOT, Competitors and Industry AnalysisDocumento14 pagineTata Elxsi Limited Fundamental Company Report Including Financial, SWOT, Competitors and Industry AnalysisAastik MadanNessuna valutazione finora

- Europes Most Active Business Angels 2018.compressedDocumento100 pagineEuropes Most Active Business Angels 2018.compressedEnrique SobriniNessuna valutazione finora

- KKR Private Equity Investors, L.P. Annual Report 2008Documento131 pagineKKR Private Equity Investors, L.P. Annual Report 2008AsiaBuyoutsNessuna valutazione finora

- A91 Partners JDDocumento2 pagineA91 Partners JDJohn DoeNessuna valutazione finora

- Cyprus Value Investor Conference 2018 ProgrammeDocumento10 pagineCyprus Value Investor Conference 2018 ProgrammeSophocles SophocleousNessuna valutazione finora

- HEC - Dow Jones - PE Fitness Rankings - FAQ - FinalDocumento11 pagineHEC - Dow Jones - PE Fitness Rankings - FAQ - FinalDan PrimackNessuna valutazione finora

- The Economic Case For Private EquityDocumento34 pagineThe Economic Case For Private EquitymarkbankingsNessuna valutazione finora

- Startup India - State Report - KeralaDocumento24 pagineStartup India - State Report - Keralabalamuralivv8391Nessuna valutazione finora

- Sequoia Capital India FinalDocumento14 pagineSequoia Capital India FinalPallavi TirlotkarNessuna valutazione finora

- Private Equity Insiders GuideDocumento13 paginePrivate Equity Insiders GuidemsmetoNessuna valutazione finora

- GameDev Friendly Investors List From ACHIEVERS HUBDocumento7 pagineGameDev Friendly Investors List From ACHIEVERS HUBSarahNessuna valutazione finora

- M&a SigmaDocumento57 pagineM&a SigmaDanteNessuna valutazione finora

- Middle East Family Office Investment SummitDocumento10 pagineMiddle East Family Office Investment SummitAlex BurgessNessuna valutazione finora

- Investment and VC Funds Acting in SEE RegionDocumento72 pagineInvestment and VC Funds Acting in SEE Regionpaul_costasNessuna valutazione finora

- Venture CapitalDocumento71 pagineVenture CapitalSmruti VasavadaNessuna valutazione finora

- The Impact of Private Equity Acquisitions and Operations On Capital Spending, Sales, Productivity, and Employment by SoneconDocumento20 pagineThe Impact of Private Equity Acquisitions and Operations On Capital Spending, Sales, Productivity, and Employment by SoneconAsiaBuyoutsNessuna valutazione finora

- Equity Capital in Emerging Domestic Markets and Its Critical Role in Driving Growth - NAIC and BCG Jul-2009Documento83 pagineEquity Capital in Emerging Domestic Markets and Its Critical Role in Driving Growth - NAIC and BCG Jul-2009AsiaBuyoutsNessuna valutazione finora

- American Jobs and The Impact of Private Equity Transactions - Sonecon Jan-2008Documento12 pagineAmerican Jobs and The Impact of Private Equity Transactions - Sonecon Jan-2008AsiaBuyoutsNessuna valutazione finora

- Taxation of Carried Interest in Private Equity - Weisbach Apr-2008Documento50 pagineTaxation of Carried Interest in Private Equity - Weisbach Apr-2008AsiaBuyouts0% (1)

- Private Equity and Leveraged Buyouts Study - European Parliament Nov-2007Documento65 paginePrivate Equity and Leveraged Buyouts Study - European Parliament Nov-2007AsiaBuyoutsNessuna valutazione finora

- Role of Private Equity in US Capital Markets - Sonecon Oct-2008Documento21 pagineRole of Private Equity in US Capital Markets - Sonecon Oct-2008AsiaBuyoutsNessuna valutazione finora

- White Paper On Corporate Governance in Asia Dated 04-December-2003 by OECDDocumento113 pagineWhite Paper On Corporate Governance in Asia Dated 04-December-2003 by OECDAsiaBuyoutsNessuna valutazione finora

- Global Economic Impact of Private Equity Report 2010 - World Economic ForumDocumento76 pagineGlobal Economic Impact of Private Equity Report 2010 - World Economic ForumAsiaBuyoutsNessuna valutazione finora

- Role of The Private Equity Sector Promoting Economic Recovery by Sonecon - March 2009Documento13 pagineRole of The Private Equity Sector Promoting Economic Recovery by Sonecon - March 2009AsiaBuyoutsNessuna valutazione finora

- Why Are Buyouts Levered? The Financial Structure of Private Equity Funds Dated 04-January-07Documento60 pagineWhy Are Buyouts Levered? The Financial Structure of Private Equity Funds Dated 04-January-07AsiaBuyoutsNessuna valutazione finora

- How Do Private Equity Investors Create Value - 2006 - Ernst and YoungDocumento12 pagineHow Do Private Equity Investors Create Value - 2006 - Ernst and YoungAsiaBuyoutsNessuna valutazione finora

- Corporate Perceptions of Private Equity - Asia-Pacific Nov-2008 - KPMGDocumento28 pagineCorporate Perceptions of Private Equity - Asia-Pacific Nov-2008 - KPMGAsiaBuyoutsNessuna valutazione finora

- Competitive Impact of Global Private Equity: Creative Destruction and Innovation by Thunderbird School, April 2008Documento42 pagineCompetitive Impact of Global Private Equity: Creative Destruction and Innovation by Thunderbird School, April 2008AsiaBuyoutsNessuna valutazione finora

- Leveraged Buyouts and Private Equity June-2008 - Univ. of Chicago and Stockholm School of EconomicsDocumento40 pagineLeveraged Buyouts and Private Equity June-2008 - Univ. of Chicago and Stockholm School of EconomicsAsiaBuyouts100% (1)

- Corporate Governance in Asia - Regional Overview and Hot Topics 24-June-2009 - Asian Corporate Governance AssociationDocumento20 pagineCorporate Governance in Asia - Regional Overview and Hot Topics 24-June-2009 - Asian Corporate Governance AssociationAsiaBuyoutsNessuna valutazione finora

- Implementing The White Paper On Corporate Governance in Asia - Stock-Take of Progress On Priorities and Recommendations For Reform - October 2006 - OECDDocumento93 pagineImplementing The White Paper On Corporate Governance in Asia - Stock-Take of Progress On Priorities and Recommendations For Reform - October 2006 - OECDAsiaBuyoutsNessuna valutazione finora

- Asia: Overview of Corporate Governance Frameworks in 2007 - OECDDocumento43 pagineAsia: Overview of Corporate Governance Frameworks in 2007 - OECDAsiaBuyoutsNessuna valutazione finora

- Private Equity Vs PLC Boards: A Comparison of Practices and Effectiveness August-2008 - London Business School and MWM ConsultingDocumento20 paginePrivate Equity Vs PLC Boards: A Comparison of Practices and Effectiveness August-2008 - London Business School and MWM ConsultingAsiaBuyoutsNessuna valutazione finora

- Testimony of Mark TrenowskiDocumento8 pagineTestimony of Mark TrenowskiDealBook100% (3)

- Testimony of Douglas Lowenstein of The Private Equity Council - 17-July-2009Documento8 pagineTestimony of Douglas Lowenstein of The Private Equity Council - 17-July-2009AsiaBuyoutsNessuna valutazione finora

- Corporate Governance in Asia - How VC Funds and Directors Can Help To Manage Governance Risks 6-August-2009 - Asian Corporate Governance AssociationDocumento17 pagineCorporate Governance in Asia - How VC Funds and Directors Can Help To Manage Governance Risks 6-August-2009 - Asian Corporate Governance AssociationAsiaBuyoutsNessuna valutazione finora

- Corporate Governance Failures in Asia - How Can Directors and Corporate Counsel Help To Manage Risk 6-May-2009 - ACGADocumento23 pagineCorporate Governance Failures in Asia - How Can Directors and Corporate Counsel Help To Manage Risk 6-May-2009 - ACGAAsiaBuyoutsNessuna valutazione finora

- Corporate Governance and Value Creation - Evidence From Private Equity 2-June-2008 - McKinsey and London Business SchoolDocumento68 pagineCorporate Governance and Value Creation - Evidence From Private Equity 2-June-2008 - McKinsey and London Business SchoolAsiaBuyoutsNessuna valutazione finora

- Corporate Governance in Asia - Recent Evidence From Indonesia, Korea, Thailand and Malaysia - October-2004 - Asian Development Bank InstituteDocumento211 pagineCorporate Governance in Asia - Recent Evidence From Indonesia, Korea, Thailand and Malaysia - October-2004 - Asian Development Bank InstituteAsiaBuyoutsNessuna valutazione finora

- AXA Private Equity 2008 Annual ReportDocumento30 pagineAXA Private Equity 2008 Annual ReportAsiaBuyoutsNessuna valutazione finora

- AIG Private Equity 2008 Annual ReportDocumento78 pagineAIG Private Equity 2008 Annual ReportAsiaBuyoutsNessuna valutazione finora

- AIG Private Equity 2007 Annual ReportDocumento70 pagineAIG Private Equity 2007 Annual ReportAsiaBuyoutsNessuna valutazione finora

- Private Equity Advent International 2007 Annual ReviewDocumento16 paginePrivate Equity Advent International 2007 Annual ReviewAsiaBuyouts100% (2)

- AIG Private Equity 2006 Annual ReportDocumento68 pagineAIG Private Equity 2006 Annual ReportAsiaBuyoutsNessuna valutazione finora

- Feasibility Study-Rimrock Kayak Rentals and MoreDocumento20 pagineFeasibility Study-Rimrock Kayak Rentals and Moreapi-335709436Nessuna valutazione finora

- Chapter 11 Supplemental Questions: E11-3 (Depreciation Computations-SYD, DDB-Partial Periods)Documento9 pagineChapter 11 Supplemental Questions: E11-3 (Depreciation Computations-SYD, DDB-Partial Periods)Dyan Novia67% (3)

- A Design Measurement and Management Model: The DMI Design Value ScorecardDocumento7 pagineA Design Measurement and Management Model: The DMI Design Value ScorecardDaz ArunabhNessuna valutazione finora

- Internship Report On "Human Resource Managemet Practices of NCC Bank Ltd.Documento57 pagineInternship Report On "Human Resource Managemet Practices of NCC Bank Ltd.Arefin RidwanNessuna valutazione finora

- Q 1Documento4 pagineQ 1sam heisenbergNessuna valutazione finora

- Chapter 7 Portfolio Theory: Prepared By: Wael Shams EL-DinDocumento21 pagineChapter 7 Portfolio Theory: Prepared By: Wael Shams EL-DinmaheraldamatiNessuna valutazione finora

- Cash and Cash Equivalents TheoriesDocumento5 pagineCash and Cash Equivalents Theoriesjane dillanNessuna valutazione finora

- Activity Questions 6.1 Suggested SolutionsDocumento6 pagineActivity Questions 6.1 Suggested SolutionsSuziNessuna valutazione finora

- Research Papers On Bank Loans in IndiaDocumento7 pagineResearch Papers On Bank Loans in Indiaofahxdcnd100% (1)

- Optimal Capital Structure Is The Mix of Debt and Equity ThatDocumento29 pagineOptimal Capital Structure Is The Mix of Debt and Equity ThatdevashneeNessuna valutazione finora

- Iesco Online Billl PDFDocumento2 pagineIesco Online Billl PDFAsad AliNessuna valutazione finora

- Why Oil and Gas Development Company Limited (OGDCL) Should Not Be PrivatizedDocumento11 pagineWhy Oil and Gas Development Company Limited (OGDCL) Should Not Be PrivatizedZohaib GondalNessuna valutazione finora

- Doing Business in UAEDocumento16 pagineDoing Business in UAEHani SaadeNessuna valutazione finora

- International Business: Gaurav DawarDocumento22 pagineInternational Business: Gaurav Dawarsarathnair26Nessuna valutazione finora

- Lithuanian Association of Basketball CoachesDocumento1 paginaLithuanian Association of Basketball CoachesLietuvos Krepšinio Trenerių AsociacijaNessuna valutazione finora

- Decline of Spain SummaryDocumento4 pagineDecline of Spain SummaryNathan RoytersNessuna valutazione finora

- Fabm2121 Week 11 19Documento40 pagineFabm2121 Week 11 19Mikhaela CoronelNessuna valutazione finora

- ComputationDocumento4 pagineComputationIshita shahNessuna valutazione finora

- The Impact of Firm Growth On Stock Returns of Nonfinancial Firms Listed On Egyptian Stock ExchangeDocumento17 pagineThe Impact of Firm Growth On Stock Returns of Nonfinancial Firms Listed On Egyptian Stock Exchangealma kalyaNessuna valutazione finora

- BaupostDocumento20 pagineBaupostapi-26094277Nessuna valutazione finora

- Mymaxicare Rates 2021Documento2 pagineMymaxicare Rates 2021Ariane ComboyNessuna valutazione finora

- Intimation of Demand NoteDocumento1 paginaIntimation of Demand NoteDeepakNessuna valutazione finora

- Philippine Deposit Insurance CorporationDocumento19 paginePhilippine Deposit Insurance CorporationGuevarra AngeloNessuna valutazione finora

- Flow Bill Explanation (Papiamentu)Documento2 pagineFlow Bill Explanation (Papiamentu)Shanon OsborneNessuna valutazione finora

- PMS Reckoner SeptDocumento7 paginePMS Reckoner SeptsendtokrishmunNessuna valutazione finora

- CH 07 Account Receivables and Inventory MGTDocumento61 pagineCH 07 Account Receivables and Inventory MGTElisabeth LoanaNessuna valutazione finora

- Topic 2 - Deferred TaxDocumento2 pagineTopic 2 - Deferred Tax靖怡Nessuna valutazione finora

- Deed of Absolute Sale of A Portion of LandDocumento2 pagineDeed of Absolute Sale of A Portion of LandmkabNessuna valutazione finora

- Chap 011 SolutionsDocumento8 pagineChap 011 Solutionsarie_spp100% (1)

- Financial StatementsDocumento21 pagineFinancial Statementsastute kidNessuna valutazione finora