Potrebbero piacerti anche

- Consumer Sentiment August 2009Documento5 pagineConsumer Sentiment August 2009peter_martin9335Nessuna valutazione finora

- Consumer Sentiment Report January 2010Documento5 pagineConsumer Sentiment Report January 2010peter_martin9335Nessuna valutazione finora

- Consumer Sentiment, SeptemberDocumento8 pagineConsumer Sentiment, Septemberpeter_martin9335Nessuna valutazione finora

- Consumer Sentiment Index OctoberDocumento5 pagineConsumer Sentiment Index Octoberpeter_martin9335Nessuna valutazione finora

- Westpac - Melbourne Institute Consumer Sentiment Index September 2013Documento8 pagineWestpac - Melbourne Institute Consumer Sentiment Index September 2013peter_martin9335Nessuna valutazione finora

- Westpac - Melbourne Institute Consumer Sentiment Index March 2013Documento8 pagineWestpac - Melbourne Institute Consumer Sentiment Index March 2013peter_martin9335Nessuna valutazione finora

- Consumer Price Index - Apr 13 FinalDocumento4 pagineConsumer Price Index - Apr 13 FinalPatricia bNessuna valutazione finora

- Inside The Surprise IndexDocumento5 pagineInside The Surprise IndexmaxNessuna valutazione finora

- The Economy Is in A Recession:: Analysis of US Economy From 2005-2010Documento6 pagineThe Economy Is in A Recession:: Analysis of US Economy From 2005-2010Jake SchnallNessuna valutazione finora

- InflationKSAEn Q4-2019Documento9 pagineInflationKSAEn Q4-2019indraseenayya chilakalaNessuna valutazione finora

- The GIC WeeklyDocumento12 pagineThe GIC WeeklyedgarmerchanNessuna valutazione finora

- Fed Refocus: Sector WatchDocumento5 pagineFed Refocus: Sector WatchSokhomNessuna valutazione finora

- InflationKSAEn Q3-2019 EnglishDocumento9 pagineInflationKSAEn Q3-2019 Englishindraseenayya chilakalaNessuna valutazione finora

- Consumer Price Index: Inflation Rate 1.9%Documento4 pagineConsumer Price Index: Inflation Rate 1.9%BernewsAdminNessuna valutazione finora

- The Trendpointers Report: Advance Signals For Economic Expectations and ConsumptionDocumento19 pagineThe Trendpointers Report: Advance Signals For Economic Expectations and ConsumptionmarcycapronNessuna valutazione finora

- Supply Chain Management Strategy Planning and Operation 7th Edition Chopra Solutions ManualDocumento14 pagineSupply Chain Management Strategy Planning and Operation 7th Edition Chopra Solutions Manualmoriskledgeusud100% (22)

- Aci Reuters BuyDocumento6 pagineAci Reuters BuysinnlosNessuna valutazione finora

- 1909 Ausbil Unitholder Report PDFDocumento32 pagine1909 Ausbil Unitholder Report PDFTonyNessuna valutazione finora

- Monthly Economic DataDocumento2 pagineMonthly Economic Dataapi-25887578Nessuna valutazione finora

- Industry: Table 7.1: Annual Growth Rate of Industrial Production in Major Sectors of Industry Base: 1993-94 100Documento22 pagineIndustry: Table 7.1: Annual Growth Rate of Industrial Production in Major Sectors of Industry Base: 1993-94 100naren2006100% (3)

- CH 04Documento28 pagineCH 04Ali EmadNessuna valutazione finora

- PR201007Documento1 paginaPR201007qtipxNessuna valutazione finora

- BX View On 2011 - Wein Oct 2010Documento60 pagineBX View On 2011 - Wein Oct 2010anujbahalNessuna valutazione finora

- ITC Quarterly Result Presentation Q3 FY2021Documento46 pagineITC Quarterly Result Presentation Q3 FY2021Vineet UttamNessuna valutazione finora

- ReportDocumento15 pagineReportsimon jordan1005Nessuna valutazione finora

- Consumer Price IndexDocumento7 pagineConsumer Price IndexKashémNessuna valutazione finora

- InflationKSAEn Q3-2020 EnglishDocumento10 pagineInflationKSAEn Q3-2020 Englishindraseenayya chilakalaNessuna valutazione finora

- 2021 01 Executive Cotton UpdateDocumento15 pagine2021 01 Executive Cotton UpdatePadmanaban PasuvalingamNessuna valutazione finora

- Consumer Confidence Survey: HighlightsDocumento5 pagineConsumer Confidence Survey: HighlightsRidhima SaxenaNessuna valutazione finora

- Leading Index May 2010Documento7 pagineLeading Index May 2010Peter MartinNessuna valutazione finora

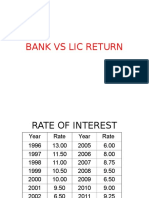

- Bank Vs LicDocumento15 pagineBank Vs LicPraveen AsokaranNessuna valutazione finora

- InflationKSA en Q1-2021 EnglishDocumento8 pagineInflationKSA en Q1-2021 Englishindraseenayya chilakalaNessuna valutazione finora

- Inflation en Q2-2021 EnglishKSADocumento8 pagineInflation en Q2-2021 EnglishKSAindraseenayya chilakalaNessuna valutazione finora

- Rate of Inflation and Rate of Unemployment in That CountryDocumento7 pagineRate of Inflation and Rate of Unemployment in That CountryumairahNessuna valutazione finora

- Consumer Price Index - Apr 12Documento4 pagineConsumer Price Index - Apr 12patburchall6278Nessuna valutazione finora

- Weekly Economic & Financial Commentary 18novDocumento12 pagineWeekly Economic & Financial Commentary 18novErick Abraham MarlissaNessuna valutazione finora

- History Favours The BraveDocumento4 pagineHistory Favours The BraveNaresh KumarNessuna valutazione finora

- Solutions: Part 5 Practice Exam 2Documento23 pagineSolutions: Part 5 Practice Exam 2Lee AlvarezNessuna valutazione finora

- Monthly Review August 2013Documento13 pagineMonthly Review August 2013faridwazirNessuna valutazione finora

- Summary of Economic Financial Data March 2021 1Documento14 pagineSummary of Economic Financial Data March 2021 1Fuaad DodooNessuna valutazione finora

- No1 Economy WaddellDocumento22 pagineNo1 Economy WaddellLowell FeldNessuna valutazione finora

- Ahluwalia - Economic Reforms in India Since 1991Documento34 pagineAhluwalia - Economic Reforms in India Since 1991sambit pradhanNessuna valutazione finora

- Economic Reforms in India Since 1991 Has Gradualism WorkedDocumento31 pagineEconomic Reforms in India Since 1991 Has Gradualism WorkedPallabi GuhaNessuna valutazione finora

- Joint Release U.S. Department of Housing and Urban DevelopmentDocumento4 pagineJoint Release U.S. Department of Housing and Urban Developmentapi-25887578Nessuna valutazione finora

- Monthly Review On Price Indices: January, 2013Documento12 pagineMonthly Review On Price Indices: January, 2013junaid112Nessuna valutazione finora

- Consumer Price Index - May 11Documento4 pagineConsumer Price Index - May 11Patricia bNessuna valutazione finora

- Tue0620212357 - Incentive Plan FSOs - FY2122Documento14 pagineTue0620212357 - Incentive Plan FSOs - FY2122Sheshdhar Nagendra TiwariNessuna valutazione finora

- Volatile February Torpedoes ConfidenceDocumento3 pagineVolatile February Torpedoes ConfidenceCeleste KatzNessuna valutazione finora

- DistCo Warehouse ForecastingDocumento3 pagineDistCo Warehouse ForecastinghatanoloveNessuna valutazione finora

- Summary of Economic & Financial Data - September 2020Documento14 pagineSummary of Economic & Financial Data - September 2020Fuaad DodooNessuna valutazione finora

- Forecasting MethodsDocumento14 pagineForecasting MethodsSiddiqullah IhsasNessuna valutazione finora

- Siena Research Institute: Confidence Down in NY Consumer Recovery StallsDocumento4 pagineSiena Research Institute: Confidence Down in NY Consumer Recovery StallsElizabeth BenjaminNessuna valutazione finora

- Cpi Review March 2013 PDFDocumento12 pagineCpi Review March 2013 PDFjunaid112Nessuna valutazione finora

- Table 7.6: Outstanding Loans of Scheduled Commercial Banks by Interest RateDocumento12 pagineTable 7.6: Outstanding Loans of Scheduled Commercial Banks by Interest RateFarhat ImteyazNessuna valutazione finora

- Global Crisis and The Indian Economy-On A Few Unconventional AssertionsDocumento23 pagineGlobal Crisis and The Indian Economy-On A Few Unconventional AssertionsSumeet SharmaNessuna valutazione finora

- Joint Release U.S. Department of Housing and Urban DevelopmentDocumento4 pagineJoint Release U.S. Department of Housing and Urban Developmentp_balathandayuthamNessuna valutazione finora

- 20 LO4 Analysis and Interpretation of DataDocumento12 pagine20 LO4 Analysis and Interpretation of DatawmathematicsNessuna valutazione finora

- Weekly Economic & Financial Commentary 15aprDocumento13 pagineWeekly Economic & Financial Commentary 15aprErick Abraham MarlissaNessuna valutazione finora

- Consumer Price Index - Aug 20Documento4 pagineConsumer Price Index - Aug 20BernewsAdminNessuna valutazione finora

- GitAA 2015 EconomicsDocumento2 pagineGitAA 2015 Economicspeter_martin9335Nessuna valutazione finora

- GitAA 2015 EconomicsDocumento2 pagineGitAA 2015 Economicspeter_martin9335Nessuna valutazione finora

- 2014 Talent Et Al ACT Energy and Water BaselineDocumento66 pagine2014 Talent Et Al ACT Energy and Water Baselinepeter_martin9335Nessuna valutazione finora

- Letter From PanelDocumento1 paginaLetter From PanelUniversityofMelbourneNessuna valutazione finora

- GitAA 2015 EconomicsDocumento2 pagineGitAA 2015 Economicspeter_martin9335Nessuna valutazione finora

- Progressive SuperannuationDocumento2 pagineProgressive Superannuationpeter_martin9335Nessuna valutazione finora

- Complaint To CPA Australia PDFDocumento13 pagineComplaint To CPA Australia PDFpeter_martin9335Nessuna valutazione finora

- ACHR Paper On GP CopaymentsDocumento14 pagineACHR Paper On GP CopaymentsABC News OnlineNessuna valutazione finora

- GitAA 2015 EconomicsDocumento2 pagineGitAA 2015 Economicspeter_martin9335Nessuna valutazione finora

- Names of Exec Managers CEO and Chief ExecDocumento4 pagineNames of Exec Managers CEO and Chief Execpeter_martin9335Nessuna valutazione finora

- CC Report PDFDocumento16 pagineCC Report PDFPolitical AlertNessuna valutazione finora

- Commonwealth of Australia: The ConstitutionDocumento4 pagineCommonwealth of Australia: The Constitutionpeter_martin9335Nessuna valutazione finora

- Baby Bonus 2 PDFDocumento15 pagineBaby Bonus 2 PDFpeter_martin9335Nessuna valutazione finora

- Opposition BudgetDocumento8 pagineOpposition BudgetABC News OnlineNessuna valutazione finora

- Tony Abbott's First MinistryDocumento2 pagineTony Abbott's First MinistryLatika M BourkeNessuna valutazione finora

- COSTINGSDocumento5 pagineCOSTINGSPolitical Alert100% (1)

- Biggest Monthly Jobs Increase in 13 Years: The Hon Bill Shorten MPDocumento2 pagineBiggest Monthly Jobs Increase in 13 Years: The Hon Bill Shorten MPpeter_martin9335Nessuna valutazione finora

- BabyBonus PDFDocumento18 pagineBabyBonus PDFpeter_martin9335Nessuna valutazione finora

- Sans Nom 2Documento320 pagineSans Nom 2khalidNessuna valutazione finora

- Dario Great Wall of China Lesson PlanDocumento3 pagineDario Great Wall of China Lesson Planapi-297914033Nessuna valutazione finora

- Strps 15 3Documento2 pagineStrps 15 3Akanksha ChattopadhyayNessuna valutazione finora

- KSS 41 END enDocumento702 pagineKSS 41 END enJavier Del Pozo Garcia100% (1)

- How To Verify SSL Certificate From A Shell PromptDocumento4 pagineHow To Verify SSL Certificate From A Shell Promptchinku85Nessuna valutazione finora

- Sharda dss10 PPT 06Documento48 pagineSharda dss10 PPT 06Ragini PNessuna valutazione finora

- GE Power System and Corporate ExpressDocumento8 pagineGE Power System and Corporate ExpressdollieNessuna valutazione finora

- SuperPad2 Flytouch3 Tim Rom TipsDocumento4 pagineSuperPad2 Flytouch3 Tim Rom TipspatelpiyushbNessuna valutazione finora

- Week1 - Introduction To Business Process ManagementDocumento29 pagineWeek1 - Introduction To Business Process ManagementRamsky Baddongon PadigNessuna valutazione finora

- Statistics Mid-Term Exam - February 2023Documento18 pagineStatistics Mid-Term Exam - February 2023Delse PeterNessuna valutazione finora

- Victor Vroom PresentaciónDocumento7 pagineVictor Vroom Presentaciónapi-3831590100% (1)

- Family Day by Day - The Guide To A Successful Family LifeDocumento212 pagineFamily Day by Day - The Guide To A Successful Family Lifeprajya100% (3)

- PTSD, Assessment, Ies, TDocumento2 paginePTSD, Assessment, Ies, TKrishnaNessuna valutazione finora

- IBM Global Human Capital StudyDocumento72 pagineIBM Global Human Capital Studypraneeth.patlola100% (9)

- Application of Sensors in An Experimental Investigation of Mode DDocumento284 pagineApplication of Sensors in An Experimental Investigation of Mode DHamed MasterNessuna valutazione finora

- Bqs PDFDocumento14 pagineBqs PDFMiguel ColinaNessuna valutazione finora

- Updating Cd2 School Heads: TradeanDocumento2 pagineUpdating Cd2 School Heads: TradeanCarlos GarciaNessuna valutazione finora

- Doc 01 DE 20190115144751 PDFDocumento20 pagineDoc 01 DE 20190115144751 PDFAdi MNessuna valutazione finora

- Disconnected ManDocumento4 pagineDisconnected ManBecky100% (1)

- 5 HPHT API 6x - FowlerDocumento13 pagine5 HPHT API 6x - Fowlerchau nguyenNessuna valutazione finora

- Bartletts TestDocumento67 pagineBartletts TestRajendra KumarNessuna valutazione finora

- Lessons Electric Circuits 1 PDFDocumento530 pagineLessons Electric Circuits 1 PDFStefano SintoniNessuna valutazione finora

- My Dream Job Essay WritingDocumento3 pagineMy Dream Job Essay WritingAnne NgNessuna valutazione finora

- 10 Laws of Love: Principles That Will Transform Your Life!Documento72 pagine10 Laws of Love: Principles That Will Transform Your Life!rammohan2bNessuna valutazione finora

- Vibration MeasurementDocumento20 pagineVibration MeasurementDae A VeritasNessuna valutazione finora

- Ass AsDocumento2 pagineAss AsMukesh BishtNessuna valutazione finora

- Interpersonel Need of Management Student-Acilitor in The Choice of ElectivesDocumento180 pagineInterpersonel Need of Management Student-Acilitor in The Choice of ElectivesnerdjumboNessuna valutazione finora

- Literacy Lesson PlanDocumento5 pagineLiteracy Lesson Planapi-437974951Nessuna valutazione finora

- Challenges To FreedomDocumento11 pagineChallenges To Freedomgerlie orqueNessuna valutazione finora

- Quiz Unit 2 B3Documento9 pagineQuiz Unit 2 B3Nicolás Felipe Moreno PáezNessuna valutazione finora